METIN TEKECI provides an analytical review of the Turkish corporate Sukuk landscape.

Despite 99.2% of its population being Muslim (according to Diyanet Report), Turkey was a latecomer to the global Islamic finance arena. The modern Turkish Islamic banking history goes back to the early 1980s and the legal infrastructure has been unified with that of conventional banking under the Banking Law No 5411 in 2005.

Turkey has received substantial support from the World Bank Group to develop its Islamic finance sector; the World Bank Group is also supporting the Republic’s initiatives to position Istanbul as a finance center. The government is taking active steps to develop its treasury Sukuk markets to diversify sources of capital to channel it toward economic development.

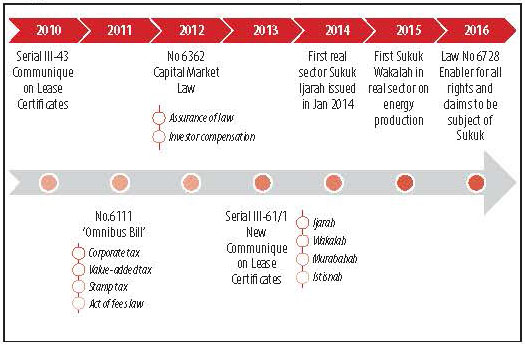

Turkey’s Sukuk legal framework was initiated under the capital market regulations, first of which is the Serial III-43 Communique on Lease Certificates in 2010.

This subordinate legislation remained inapplicable in the market until the enactment of Omnibus Bill No 6111 in 2011, which introduced tax neutrality on Sukuk Ijarah issuances. The first issuance registered under the Turkish Capital Markets Board (apart from the US$100 million issuance by Kuveyt Turk in August 2010 which was issued through an SPV in Cayman Islands) and sold out to foreign investors was the US$1.5 billion Sukuk facility by the Turkish Undersecretariat of Treasury (Hazine) in September 2012.

Diagram 1: Turkish Sukuk development timeline

At the end of 2012 and mid of 2013, the new capital Markets Law No 6362 and the new Communique in Lease Certificates (Serial 61.1) (the Communique, hereafter) were issued and provided the biggest leverage for market players to issue their own Sukuk.

Table 1: Sukuk issuance in the Turkish market

|

|

EUR |

MYR |

TRY |

USD |

Total |

|

MATURED |

|

|

|

|

|

|

Domestic |

|

|

74 |

|

74 |

|

Foreign |

|

|

1 |

4 |

5 |

|

OUTSTANDING |

|

|

|

|

|

|

Domestic |

|

|

20 |

|

20 |

|

Foreign |

1 |

6 |

2 |

7 |

16 |

|

TOTAL |

1 |

6 |

97 |

11 |

115 |

The momentum of Sukuk issuances especially those observed in the domestic market until 2016, proved that Sukuk have significant potential to become a complementary solution to conventional bonds and loans in Turkey, both for the originators and investors. We have observed 115 issuances from 2010 until November 2016, and 36 of these are still outstanding today, corresponding roughly to US$8.7 billion-worth of Sukuk circulating in the market.

We have observed that the outstanding Sukuk issuances of each issuer in Turkey are mainly denominated in US dollars with an average tenor of slightly above five years. TRY issuances are mostly used for short-term financing needs, generally in the size of TRY6 million (US$1.71 million).

Turkiye Finans (a subsidiary of Saudi giant National Commercial Bank) and Kuveyt Turk (the Turkish arm of Kuwait Finance House Group), and the Hazine are the leading originators of US dollar Sukuk issuances. Both Turkiye Finans and Kuveyt Turk are also the only Turkish issuers in the ringgit market to date.

Table 2: Outstanding Sukuk volume (in USD million)

|

Outstanding Sukuk |

EUR |

MYR |

TRY |

USD |

|

BEREKET VKS |

|

|

175 |

350 |

|

Hazine |

|

|

9.48 |

2.75 |

|

KABTEK VKS |

12 |

|

|

|

|

KT VKS |

|

800 |

550 |

1 |

|

TF VKS |

|

1.16 |

394 |

1 |

|

TFKB VKS |

|

|

314 |

|

|

ZIRAAT KATILIM VKS |

|

|

100 |

|

|

|

|

|

|

|

Sukuk are also of crucial importance in generating quasi-capital sources, considering the growth pressures on Islamic banking in Turkey. Tier 2 Sukuk issuances with 10-year tenors issued by Kuveyt Turk (US$350 million), Turkiye Finans (US$250 million) and Albaraka Turk (US$250 million), provided more capitalization opportunities for growth.

New Turkish participation banks such as Vakif Bank and Ziraat Bank are also expected to emerge as new players in the domestic and international Sukuk market, thanks to the political support of the government to increase Islamic banking share up to 15% from the current 4.7% (according to October 2016 figures by the Banking Regulation Supervisory Authority).

In 2013, the legal framework was modified to permit the use of diversified Islamic financial instruments in Turkey, enabling Sukuk to be structured using:

- Ownership (Ijarah)

- Management contract (Wakalah)

- Trade (Murabahah)

- Partnership (Mudarabah)

- Work of art contract (Istisnah)

All these types of Sukuk, or any hybrid types acceptable by the Capital Markets Board (CMB), may be issued through public offering, private placement or sales to qualified investors only.

The most preferred issuance method is to qualified investors mostly due to the fact that the market is still premature. On the other hand, the CMB regulation does not require prospectus for private placement issuance.

Chart 1: Breakdown of Sukuk issuance methods

Chart 2: Number of Sukuk issuance by type

Ijarah is the most common Sukuk structure in the Turkish market. More than half of Turkish issuances are based on the Ijarah model or are based on an Ijarah-Murabahah combination. This has mainly stemmed from the opaque tax treatment on the Mudarabah and Istisnah models. The issuers, in response, are avoiding such tax risks.

A unique feature of Turkish Sukuk regulation against its global peers is that SPVs or asset leasing companies (ALCs) are permitted to issue multiple Sukuk concurrently on behalf of different originator companies, subject to the approval of the CMB. This permission mitigates cost of establishment and running an SPV, and concentrates knowledge base on the subject matter.

The financial reporting of asset base of different Sukuk issuances are segregated on the financial statements. Liquidation in case of a default is also defined to be managed and executed by the Investor Compensation Center, a public legal entity established under Capital Market Law.

The legal presence of ALCs in Turkish legislation has not been tested through a default case, however, the robust CMB supervision over each issuance provides comfort to investors. It is also worth to mention that ALCs are mainly used to fund their founder companies (except TFKB VKS).

TFKB VKS, differs in the market by functioning as a special Sukuk origination hub for customers of Turkiye Finans. Total issuance by TFKB VKS to date stands at TRY343 million (US$130 million, according to USD-TRY exchange rates during times of issuances) on behalf of four different originators operating in real economic sectors of Turkey, and Turkiye Finans remains the sole investor in these issuances. This model can set the groundwork for corporates looking to tap the Sukuk market.

Table 3: ALCs in Turkey

ALC Type Founder

HAZINE VKS Sovereign Turkish Treasury

AKTIF BANK SUKUK VKS Investment bank Aktif Investment Bank

ASYA VKS Islamic bank Bank Asya

BEREKET VKS Islamic bank Albaraka Turk

KABTEK VKS Corporate Kablotek AS

KT SUKUK VKS Islamic bank Kuveyt Turk

KT VKS Islamic bank Kuveyt Turk

TF VKS Islamic bank Turkiye Finans

TFKB VKS Islamic bank Turkiye Finans

ZIRAAT KATILIM VKS Islamic bank – public Ziraat Katilim

Non-bank financial institutions are playing an increasing role in the Turkish Sukuk market as an investor to these issuances however there is still plenty of room to reach to full potential. With the accelerating contribution of Turkish Takaful operators (eg, Katilim Emeklilik, Neova Insurance, Doga Insurance), Islamic investment firms (eg BMD Portfolio Management, Qinvest Portfolio Management), and conventional companies providing Islamic investment products to their customers ( eg Ziraat Portfolio, Ak Portfolio, Vakif Emeklilik, Garanti Emeklilik) the Sukuk market is expected to generate stronger demand in domestic market. On top of this list, the inclusion of large real sector companies which are already active buyers in bonds market is promising higher growth potential for this sector.

With the new Omnibus Bill – Law No 6728, published on the 9th August 2016, less popular Sukuk structures such as Mudarabah, Musharakah and Istisnah were granted tax neutrality, and this is expected to boost the utilization of Sukuk as a financing tool.

With the amendment of the Stamp Tax Law, VAT Law, and Law on Charges, all types of Sukuk transaction documents, proceeds, transfer of assets between issuer/ALC and originator will be exempted from tax and charge burdens, as required in the previous regulation. The exemptions will be also be valid for construction companies providing corporate tax exemption, and supporting project financing legal infrastructure.

Being an alternative financing source for Turkish corporations, the newly-relaxed tax framework facilitating Sukuk structures mentioned above would be useful for bridging the project financing gap in Turkey, particularly for infrastructure projects and public-private partnership projects such as airports, bridges, highways, and energy power plants.

The key challenges over the short to medium term, however, are the global and domestic macroeconomic challenges which have decelerated the growth of the Turkish economy. In order to increase the appeal of Islamic financial instruments, the government should consider introducing incentives for such products as in the case of Malaysia.

Metin Tekeci is the head of Turkiye Finans’ Bahrain branch. He can be contacted at [email protected].