Since 2008 the pace of new Islamic investment product launches has slowed down, even though the Islamic finance industry continues to witness robust growth globally. According to Ernst & Young, the Islamic finance industry is expected to reach US$1.1 trillion in assets by the end of this year, up from US$826 billion in 2010. With under US$60 billion in assets under management, this industry remains relatively small compared to its conventional counterpart. However TARIQ Al-Rifai, the director of Islamic market indices at S&P Dow Jones Indices, explains how this is set to change.

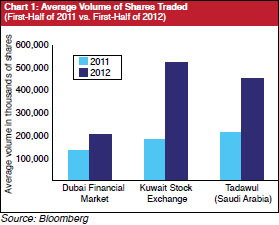

Trading volumes across GCC markets have increased dramatically since 2011. The Kuwait Stock Exchange, for example, has seen trading volume increase by over 185% in the first half of 2012, compared with the first half of 2011. Tadawul, the Saudi Arabian stock exchange and the largest exchange in the Middle East, has seen volumes increase by 115% over the same period. The Malaysian market, which has been one of the best performing markets recently, has seen trading volumes increase by 15% over the same period.

The rise in local trading activity has brought renewed confidence to the overall market and is leading investors to look outside the region for investment opportunities. Historically, the leading beneficiaries of GCC investment have been witnessed in developed markets and this will probably continue to be the case. Islamic investors in the GCC have typically favored real estate investments in their home countries while looking at international markets for equity exposure. While this preference is not expected to change any time soon, the launch of new Islamic indices over the past year is changing the product offering for Islamic investors and re-energizing interest in Islamic investments.

Equities and ETFs

Equity funds currently make up a majority of the US$60 billion in assets in Islamic funds. There are two main reasons for this. First, equity funds developed early on in the Islamic finance industry, because the equity markets worldwide were well-established. The only thing required was a universally accepted Shariah compliant screening process which would allow Islamic investors to access a universe of approved stocks. Second, the increased wealth in Islamic countries, such as the GCC and Malaysia in particular, drove demand for investment solutions, both inside and outside their home markets. As a result, equity funds took off as an asset class in the late 1990s.

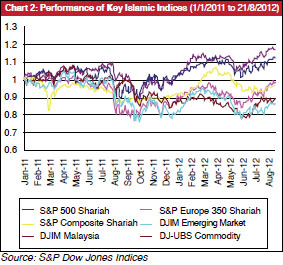

Over the past few years, stock markets in the GCC have suffered from low liquidity as well as low trading volumes. There has been less appetite for equity-based products, which is why so few Islamic equity funds have been launched since 2008. Investor confidence has also yet to recover from the recent financial crisis. The two charts show clearly that this is changing: not only are volumes increasing, but markets in the region are up as well.

One of the best performing markets since 2011 has been Malaysia. It has outpaced other emerging markets, some of which have performed poorly over the same period. Malaysia has also been one of the better IPO markets this year. GCC markets have done fairly well, beating commodities and other emerging markets, but still behind Malaysia and the US. Investors in the GCC are looking at foreign markets for investment, as they always have been. One of the more interesting segments for Islamic investors in the GCC has been in the high-dividend yield segment, which began with the launch of the Dow Jones Islamic Market Global Select Dividend Index last year.

One segment, which has yet to take off, is exchange traded funds (ETF). There are close to a dozen Islamic ETFs traded on several exchanges around the world, including Malaysia and Saudi Arabia, but they have yet to capture investors’ attention. Once investors become familiar with ETFs and the benefits they offer, they will take off in a similar way to how they took off in the US or in Europe and, more recently, in emerging markets.

Customized index products have been a major driving force for new investment products from the GCC. Many of the investors within the GCC, particularly Saudi Arabia, cannot find appropriate benchmarks for their new investment products, many of which are one-of-a-kind, thus designing customized benchmarks for them is the best way to meet their needs. The ways in which benchmarks can be created is virtually endless, and this is helping to bring new energy into the Islamic investment market. These new ideas are spilling over into other asset classes such as fixed-income (Sukuk), REITs and commodities.

Fixed-income (Sukuk)

Unlike the equity market, the fixed-income market was not readily accessible for Islamic investors to tap. No Shariah compliant screening process would make conventional bonds acceptable as an Islamic investment. The asset class itself is not compliant as it is interest-based. Therefore, for the Islamic fixed-income market to develop, new assets needed to be generated and both buyers and sellers have to be found.

The Sukuk market started from zero 12 years ago, and it represents today one of the fastest growing segments of the Islamic finance market, attracting issuers and investors from around the world. According to Bloomberg, the Sukuk market topped US$85 billion for the first time in 2011 and is expected to grow to over US$100 billion this year. The main challenge in the Sukuk market has been to meet investors’ demand. As each new issue has been oversubscribed, investors’ main complaint is the lack of liquidity in the market. The lack of liquidity is a result of investors’ buy and hold strategy since replacing Sukuk in their portfolios can be difficult.

When the Dow Jones Sukuk Index was launched in 2006, there were only 11 Sukuk issues in the index. This created a challenge for fund managers who wanted to replicate the index performance, as market pricing was not very efficient. Today, the index has over 30 issues, several Sukuk funds and portfolios benchmarked to it. There is increasing demand for additional Sukuk benchmarks, which can only develop as the industry grows and some of the liquidity issues are solved.

REITS, commodities and other asset classes

Islamic investors have always had a natural preference for real estate investments. From the launch of Islamic banks in the 1970s, real estate investments rapidly developed to satisfy the needs of the investors. Islamic banks have been some of the most active real estate investors, both in local as well as in international markets. Islamic real estate funds were developed in the 1980s but were not traded and not very liquid. The upside was that these funds paid attractive dividends. On the other hand, real estate investment trusts (REITs) were liquid and traded on major exchanges around the world, like a company’s stock or an ETF.

There were several attempts to launch Islamic funds which would invest in publicly-traded REITs around the world, but the challenge has been to find a pool of Shariah compliant REITs large enough. As this problem is almost resolved, this asset class is expected to garner a lot of attention in the coming years.

Commodities are also a very attractive asset class to Islamic investors. However, most commodities trade on a futures or options pricing and not spot pricing. So, until a universally accepted solution is found to trade commodities in a Shariah compliant manner, this asset class will remain a challenge for Islamic investors to access. One solution is equity indexes, based on commodity producers. For instance, the Dow Jones Global Equity Commodity Index gives Islamic investors the opportunity to participate in the commodity sector by gaining exposure to publicly-traded commodity producers.

While real estate and equities will remain the top asset classes favored by Islamic investors, other asset classes offer promising potential, including Takaful-linked investments, forex solutions and private equity. The re-energized investor base is making all of this possible. As with other Islamic investment products, they will take time to catch on with investors, but once they do, they will become a permanent part of the Islamic investment universe.

Tariq Al-Rifai

Director, Islamic market indices

S&P Dow Jones Indices

Public Relations

Tel: +44 20 7176 8461