Despite recent tax reforms, upcoming elections, tumbling oil prices and global market volatility, Islamic investors still just can’t get enough of UK real estate. Just what is it that makes the country so appealing — and will the attraction never end? LAUREN MCAUGHTRY looks at where the money is coming from — and who it is going to.

Strong motivation

“Whilst the year has only just started, investor interest in the UK seems as high as ever,” commented Philip Churchill, founder and managing partner of UK property fund 90 North. And perhaps counter-intuitively, as the oil prices have fallen investor enquiries have increased, suggesting that perennially property-hungry Islamic investors are keener than ever to get their money into bricks and mortar rather than leaving it in the bank at the mercy of global market currents.

The majority of interest is still in residential, with UK institutions such as 90 North, Gatehouse and London Central Portfolio all making major investments. “We are completing on our latest residential development at the moment, and aim to conduct further residential developments during 2015,” confirmed Churchill. However, interest is also growing in commercial deals, with new players such as formerly retail-focused Al Rayan Bank (previously known as Islamic Bank of Britain) moving into the market and branching out, according to Keith Leach, recently appointed chief commercial officer of the bank, which appointed him expressly to grow its corporate and real estate business. “Keith’s appointment provides IBB with the ability to tender for higher value transactions, particularly in the London real estate sector,” said Sultan Choudhury, CEO of Al Rayan Bank.

Tax mountains

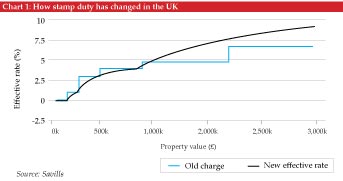

On the residential side, despite the overall upswing in interest, a number of recent tax reforms from the UK government recently threatened to derail this juggernaut, with a new stamp duty tax implemented on a progressive scale, and doubling from 5% to 10% for properties north of GBP925,000 (US$1.5 million) and to 12% for those worth GBP1.5 million (US$2.27 million) and above. The change is good news for the majority of domestic property buyers, with 98% of house purchases falling below the big jump. However, those buying expensive properties will be taxed more highly, which it was feared could put off high end property investors into the UK — including the flow of Islamic funds from Asia and the Middle East.

However, according to observers this has not so far been the case. “The UK market has absorbed historic residential purchase tax increases and moved onwards and upwards,” said Churchill. However, what the changes have done is made relative affordability more important. This has led to a trend towards increasing diversification into lower cost, higher return areas. “Prime purchasers want better value away from the traditional prime markets where values have been static at best for the last 12 months anyway. That said, for the ‘money no object’ purchaser, whilst this is a thinner market, the best postcodes will still be attractive.”

“The increase in Stamp Duty on residential property will have an impact on the market but it will not be uniform or long-term, agreed Naomi Heaton, CEO of London Central Portfolio. “For a start, almost any property under GBP1 million (US$1.52 million) will pay less stamp duty. Fifty five percent of all transactions are under GBP1 million and therefore this sector will remain buoyant. If anything, activity will increase as people try to trade underneath this price band.”

Although very high end of the market will see increases in stamp duty, this is the discretionary wealth management side of the business, and would probably be absorbed into the cost of investing into a blue chip asset within a safe haven environment. “Also, whilst there is much talk of such trophy properties, it is a very insignificant part of the market,” explained Heaton. “In the last year, there were only 65 properties sold over GBP10 million (US$15.16 million). It makes good ‘news’ stories but is of little relevance.”

However, another new tax (the non-resident capital gains tax) is also being introduced from 2015, taxing profits made from property purchases. “This has never been a main driver for investors coming into the UK however,” according to Heaton. “Therefore this has not been a deterrent and there has been very little change in behavior by investors as a result of this introduction.”

Spreading the love

London is still the favored location, unsurprisingly, with land registry statistics showing that prices in the two prime boroughs (the Royal Borough of Kensington & Chelsea and the City of Westminster) were up 13.1% and 16.6% respectively.

“We would expect continued price growth in Prime Central London but at a slower rate than in 2014, which saw growth above average levels of 10.4% per annum,” said Heaton. “Inevitably, the uncertainty around the General Election will delay some investor activity to the second half of the year but we would then expect to see the market pick up quickly.” The strategy at London Central Portfolio focuses on time in the market, rather than timing. “Whilst an investor might not see straight line linear growth, overall the limited stock (less than 6,000 transactions a year) versus the global population who wish to invest in central London means consistent upward pressure on prices.”

Greater London however, comprising the 31 boroughs outside the prime central area, which is largely a domestic market, saw prices rise even higher, by 17.4% across 2014. However, this was primarily a recovery from a run of weak performance following the credit crunch, and the market may have now reached its level of affordability. Last year the UK government also introduced the country’s first ever mortgage caps in order to limit the likelihood of a US-style housing bubble, with 85% of all new loans limited to a maximum of 4.5% of borrower income, which will inevitably affect domestic purchasing power. “While only 1 in 10 sales in Greater London are affected by the new higher rates of Stamp Duty, this will be a blow to domestic buyers who will have to save up for longer now to trade up to a more expensive property,” warned Heaton.

In the rest of the country, growth has remained weak since the credit crunch, with prices around 50% lower. As a whole, prices remain no higher than they were 10 years ago, and only saw around 3% growth last year. Although this means there is significant room for growth, mortgage caps combined with the threat of rising interest rates could mean only a limited increase in prices.

However, Islamic ventures are moving outwards from the city, and increasing numbers of new projects are looking at regional areas. 90 North has investments across the north of England and Scotland, while Al Rayan Bank is headquartered in Birmingham. In November last year, Gatehouse Bank launched a new private rented sector (PRS) joint venture with Sigma Capital, commencing construction of an initial 927 new rental homes across Liverpool and Manchester, with a total development cost of approximately GBP100 million (US$151.56 million), to create one of the first and largest PRS platforms in the UK. The project was funded by GBP67 million (US$101.6 million) of bank financing from Barclays Bank to supplement equity of GBP47 million (US$71.2 million) from Gatehouse. The initial phase of construction is part of a wider proposal with Sigma to create a portfolio of new build privately rented residential properties across multiple sites in the UK.

“I welcome the announcement of the first PRS homes to start on site in Liverpool, Salford and Greater Manchester,” said Greg Clark MP, the UK minister of state for universities, science and cities. “This is a sure sign of investment flowing into cities in the north of England, building much needed housing through this growing form of tenure and delivering new construction which contributes to the local economy, creates jobs and delivers more homes for hardworking people.”

Government drive

This growth has seen strong support from the UK government, which has identified incoming Islamic investment in UK infrastructure as one of its key goals following its inaugural sovereign Sukuk in 2014. “Islamic finance is starting to play a crucial role in infrastructure development in the UK,” according to Harry Quilter-Pinner and Lin Yan from the UK Foreign and Commonwealth Office. The US$2.4 billion Ijarah financing to redevelop the Chelsea Barracks for Qatari developer Diar, from BNP Paribas, Calyon, HSBC Holdings, Masraf al-Rayan and Qatar National Bank, represents one of the biggest Shariah compliant real estate projects in the UK, while other major developments including the Shard and the Malaysian-led Battersea Power Station project have of course also been primarily financed by Shariah compliant investment products.

“Gulf sovereign wealth funds could provide a continued source of investment in the UK, including property investment in healthcare, education and social housing sectors. We should continue to ensure that the UK is well positioned to encourage this investment,” suggested Yan and Quilter-Pinner. “A core goal is to analyze how we can better accommodate and reduce barriers to Islamic finance investment to support Her Majesty’s Government’s overarching aim to enable greater levels of investment in UK infrastructure.”

Investor impact

This will include reducing barriers and encouraging investor participation from a wide range of sources. “Investor interest is from across the GCC,” according to Churchill, while Heaton notes that: “The main investors are still coming from Southeast Asia — Malaysia, Hong Kong and Singapore, as well as the Middle East.” However interestingly, it is the Islamic nations who are pushing the market forward. While big investors, the Chinese are still investing primarily in new developments in greater London and have not yet turned their attention to the more exclusive parts of central London. “The top end of prime central London is extremely small in numbers and diverse in terms of nationality of buyers,” she emphasized.

Competitive outlook

Nevertheless with such rich pickings to be had, it is inevitable that the sector is becoming increasingly crowded and players are becoming more aggressive in catching the best deals. “The UK market has always been competitive, as the best opportunities will always be sought after — unless you are able to secure them off market, as we frequently do,” noted Churchill. And with more real estate funds entering to add to this competition, the prospect looks promising. The Sterling United Kingdom Real Estate Fund (SURF) from Gatehouse Bank and Sidra Capital last year announced the first closing and the first acquisition of a UK property. “As one of the most mature, transparent, well regulated and liquid markets in the world, the UK is considered superior to other markets. By diversifying our risk across multiple asset classes, SURF’s mixed portfolio will provide an effective hedge against inflation,” said managing director and CEO of Sidra Capital, Hani Baothman.

Gatehouse has delivered over US$500 million in real estate acquisitions in the last two years, seeing significant new investor uptake in transactions by GCC high net worth and institutional investors, according to Richard Thomas, the chief representative of Gatehouse Bank in Malaysia, where the bank recently opened a new office. “The UK real estate sector provides a compelling investment opportunity, which has arisen following heavy falls in commercial property values due to the impact of the financial crisis. As yields return to the long-term historical average and rental growth establishes itself, SURF’s real estate investments should generate solid returns for its investors,” added Thomas.

So what can we expect for 2015 — will the winning streak continue? “It is expected that Prime Central London will continue to turn in a robust performance going forward, acting as an attractive counterbalance to an increasingly volatile equity market in the face of increasing global turmoil,” predicts Heaton. “While fall away in transactional activity is always seen before any general election, historically it has always strongly bounced back. This is to be expected and we therefore see a contra-cyclical market opportunity at the moment for investors, but this is likely to be short-lived.”