Commodity Murabahah has presented a challenge to market practitioners due to concerns ranging from the abuse of practices to the permissibility of the structure under Shariah, says HERMIONE HARRISON.

Commodity Murabahah is based on the concept of Tawarruq, that is, receiving cash for a debt of a higher amount. The structure attracted considerable attention when, in 2003, the OIC Islamic Fiqh Academy (International Islamic Fiqh Academy) likened commodity Murabahah to “organized” Tawarruq which it deemed a synthetic and fictitious transaction and therefore impermissible under Shariah.

While it is easy to mistake this ruling as a criticism of the contract of commodity Murabahah or Tawarruq, according to Bursa Malaysia’s Islamic markets global head Raja Teh Maimunah, the concerns raised by the OIC Islamic Fiqh Academy in arriving at its conclusion related to the practices regarding the application of commodity Murabahah or Tawarruq and not the contract itself. In particular, the academy expressed concern over the existence of fraudulent trading contracts or an absence of physical commodities underlying the commodity Murabahah structure.

The distinction between the contract and the practice of commodity Murabahah or Tawarruq is an important one. In Raja Teh’s opinion, “it should be the practices that ought to be tightened and not the rule on the permissibility of the contract itself”.

Despite the ruling by the OIC Islamic Fiqh Academy, the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) proceeded to issue a standard guideline on the requirements of Tawarruq (Shariah standard no 31). “I see this as an acknowledgement by the body that the concept of Tawarruq in itself is acceptable though the standards of its application need to be regulated,” Raja Teh explained.

The commercial viability of commodity Murabahah

In place of commodity Murabahah, the OIC Fiqh Academy recommended the use of Qard Hassan, a loan between two parties with no contractual increment to the creditor; in other words, a benevolent loan. In Raja Teh’s view, this “is simply not a commercially viable option”.

Many proponents of commodity Murabahah share this view. In particular, Azizul Azmi Adnan, partner of the Islamic banking practice group of Wong & Partners (a member firm of Baker & McKenzie International), considers that “while the use of instruments such as commodity Murabahah may not be in strict compliance with the rulings of the OIC Fiqh Academy, or similar academies, it is necessary to consider the application of Islamic finance in the real world” he said, recognizing that Islamic finance is developing against a backdrop of an established conventional finance framework and needs to be commercially viable.

In Adnan’s view, to follow the rulings of such academies would involve a wholesale change to the existing framework of Islamic finance which realistically cannot happen overnight.

“It will take time for an understanding and appreciation of Islamic principles to develop,” he said. “Malaysia appreciates that it is a progressive process. Continuous improvements are being introduced in order to develop Islamic finance.” The development from the widespread use of the Bai al Inah contract in favor of Tawarruq-based instruments such as commodity Murabahah is an example of the constant improvement of the Islamic finance systems in Malaysia. According to Adnan, “incremental steps are important in increasing awareness and improving the system”.

Citing the maxim found in Islamic jurisprudence, “severe harm is avoided by a lighter harm” or “choosing between the lesser of two evils”, some proponents of commodity Murabahah maintain that the choice is between having to resort to liquidity management instruments, which are imbued with clear-cut riba elements, or to pursue the alternative practice of controversial Tawarruq-based instruments for the time being.

Is commodity Murabahah too organized?

By likening today’s commodity Murabahah to “organized” Tawarruq, the OIC Fiqh Academy criticized commodity Murabahah for being too pre-arranged. While many practitioners have responded to this criticism by trying to disguise the pre-arranged nature of modern commodity Murabahah transactions, Raja Teh considers the pre-arrangement of a commodity Murabahah transaction as “a necessary development from how things were done in the old days”. “It is the evolution of the trading mechanism as things become more sophisticated,” she said.

“The practice of leaving things to chance is simply not conducive in today’s complex financial system. The absence of organization will expose banks and their clients to ‘unhedged’ risks and would certainly not be entertained in today’s financial markets, especially in the aftermath of the global credit crisis.”

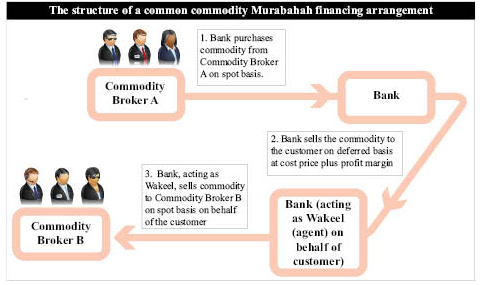

Structural features of commodity Murabahah

Compared to a simple one-step conventional financing between a lender and borrower, one could be forgiven for being somewhat confused by the structure of the comparable commodity Murabahah financing, as illustrated above.

“There is invariably an additional complexity when using Islamic finance as the basis of financing,” Adnan said, in recognition of the additional steps involved in structuring and carrying out an Islamic transaction.

Does this complexity carry a risk that the structure will not be upheld by the courts? According to him, “since Malaysia has a system of law which operates separately from Shariah, as long as the documentation does not contradict that system of law, there is freedom of contract, so it is unlikely that a structure, if well documented, will not be upheld by the courts”. The multiple roles that a financial institution may occupy in a commodity Murabahah transaction is also worthy of note. As shown in Diagram 1, a bank may act both as itself as well as wakeel (agent) on behalf of the customer.

While permitted under common law, there have been concerns regarding the risks of having one party acting in several capacities. Adnan, however, does not see this as a risk that cannot be addressed in documentation.

“As long as it is clear what the duties of the bank are while acting in differing capacities and as long as the documentation anticipates and addresses what rights and obligations might arise, it becomes a question of the parties getting comfortable that the transactions do not pose any serious risks,” he explained.

“The challenge is getting the promoters and investors more comfortable with the multiple roles that one party can perform,” he added.

These “complexities” do not appear to have translated into a higher risk rating for a commodity Murabahah based financing in Malaysia as opposed to its conventional counterpart. This could be suggestive of the level of comfort that the Malaysian market has developed with Islamic products and their underlying structures, however more complex than their conventional equivalent.

Adnan pointed out, however, that for US dollar issuances, investors may demand a higher premium for Sukuk as opposed to conventional bonds (as they did for the recent US dollar-denominated combined issue of conventional bonds and Sukuk by Petronas). Nevertheless, “this is likely to be a reflection of the need for investors to take time to understand and get comfortable with the structuring of an issue of Sukuk rather than of any inherent additional risk in the structure itself,” he explained.

What does the future hold for commodity Murabahah?

It is estimated that commodity Murabahah has an annual turnover of over US$1 trillion and in Raja Teh’s opinion, “demand remains strong”. While the ruling by the OIC Fiqh Academy may have resulted in significant discourse on the subject of commodity Murabahah and its practices, in Raja Teh’s experience, it “has not caused any major change in the way banks transact with their customers and each other simply because there is no other viable alternative at this juncture”.

“Commodity Murabahah is the one Islamic money market tool that can help provide liquidity in the Islamic banking system. There is no other instrument that is as widely used as commodity Murabahah, especially in the short term money markets. Sukuk are generally of medium to long tenure whilst other contracts, for example Wakalah, may not appeal to some risk managers in the management of short term liquidity,” she explained.

It appears that the response from some practitioners to the ruling of the OIC Fiqh Academy has been to continue to develop commodity Murabahah products but with a view to maintaining the integrity of the underlying contracts and processes. “In response to the ruling, what we have done is to design the world’s first regulated end-to-end commodity trading platform specifically to facilitate Tawarruq transactions,” explained Raja Teh, referring to the recent achievement of Bursa Malaysia.

“The structure of the trades to be undertaken via the platform addresses major concerns raised (such as) the validity of the contracts and the presence of physical commodities which are deliverable.

Those wishing to trade through the platform must first be admitted as members and are governed by a set of trading rules. Shariah audits are carried out intermittently by the exchange and members themselves may compel a Shariah audit to be undertaken upon issuance of a notice to the exchange.

“Commodity suppliers are first screened and trading flows are scrutinized before seeking approval from the national Shariah Advisory Council for the admission of a particular commodity. The whole structure of the platform is designed to ensure integrity in the trade flows.”

While the platform started out to provide for ringgit denominated trades, Raja Teh explained, it has since expanded to undertake non-ringgit denominated trades. “In addition, we have also moved to provide for a hybrid market, thus providing customers access to voice broking in addition to electronic trades (initially only electronic trades). We are also admitting other commodities in addition to our home star product, that is, crude palm oil,” she added.