As the global Sukuk market approaches the US$200 billion mark in terms of total issuance, this is an opportune time to take a step back to reflect on where the market stands with respect to the Islamic finance industry and answer some of the questions frequently asked about the market with respect to size, liquidity and diversity, and their impact on the outlook we can look forward to.

The good news about Islamic finance is that it is demand-driven and demand originates on the retail side. The man on the streets of Jeddah, Kuala Lumpur or Lagos understands what riba is and seeks ways to avoid it.

Islamic banks and financial institutions continue to be the primary beneficiaries of this trend, growing at compound annual growth rates of around 30% since 2000 and set for continued growth. Islamic banks command the majority of the US$1.3 trillion attributed to Islamic finance.

Islamic banks are offering increasingly attractive and relevant products to clients and are competing with conventional counterparts effectively so that in most jurisdictions with regulations for Islamic banks, Shariah compliant institutions are gaining market share and growing faster than their conventional peers.

This is not to say that Islamic banks and financial institutions have it easy. The global financial crisis highlighted the risks associated with concentrated and relatively large allocations to equities and real estate as well as limited liquidity and risk management tools to manage balance sheets. Transparency, governance and regulation are all important issues that are as relevant today as they were two and half years ago.

Progress, however, has been tangible on all of the above. Banks have improved their liquidity metrics and with the help of Shariah scholars and other service providers have innovated structures and contracts to diversify portfolios and better manage financial risks. Regulators in Malaysia, Saudi Arabia and Kuwait have propagated rules improving the Shariah compliant architecture for banks, asset management companies and Takaful companies. Central banks and finance ministries in the UAE, Indonesia, Gambia and Pakistan joined Malaysia, Bahrain and Brunei in issuing short-term Sukuk to manage liquidity. New multilateral institutions like the International Islamic Liquidity Management Corporation (IILM) complement the efforts of older institutions like the Islamic Development Bank and others to support the industry. Interest in Islamic finance continues unabated with China, Nigeria, Lebanon, Thailand, the Philippines, Singapore, France, the UK and others announcing various initiatives.

In the midst of all this change, Sukuk continue to occupy a central role. Policy makers, multilateral institutions, Shariah scholars, banks and asset management companies all see the tremendous benefit of large, liquid and deep Sukuk markets.

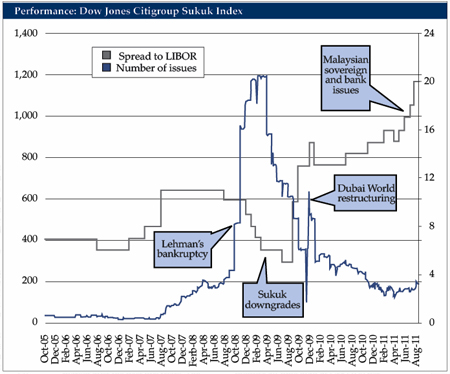

It is good news that three years after Lehman Brothers’ demise, almost to the day, Sukuk markets are significantly larger, more liquid, more diversified, and better researched with multiple precedents for restructurings and paths post-default.

Growth has returned to the Sukuk market and the technical dynamics have been improving and increasingly supportive of financial performance, especially relative to broader credit markets struggling with Eurozone debt contagion and decreasing investor confidence globally.

Year-to-date Sukuk performance has been strong. The market is up 5.3% with significantly less volatility in prices than other risk assets. Comparisons to equity, real estate or even global credit highlight the relative outperformance of Sukuk when the fundamentals of Islamic financial institutions and the economies they operate in are strong and improving.

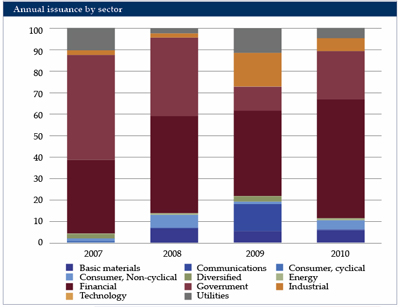

Issuance

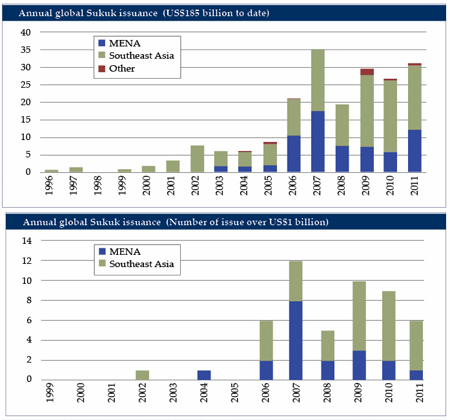

Sukuk issuance has recovered from the challenges of 2008, not just in quantity but quality as well. Since 2005, the number of larger, international and more liquid transactions has increased significantly and consistently. This has improved the quality of benchmarks, portfolios as well liquidity in the secondary markets.

Liquidity

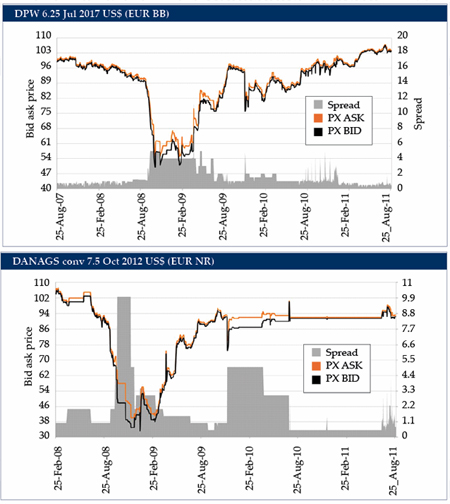

Frequently cited as a key restraint for participation in Sukuk markets, liquidity is often assumed to be static and low, or even dangerously unavailable. This is simply incorrect. Like any feature of a market, especially a developing one, liquidity goes through cycles and is necessarily a function of several factors, including investor confidence, liquidity on the balance sheet of market participants, and expected returns among others.

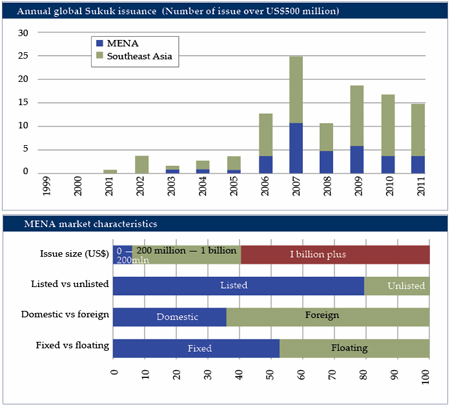

Therefore, different Sukuk have different liquidity profiles that vary over time. The credit quality of the issuer, the size of the issue and security specfiic risks all affect liquidity, as they would a conventional bond for each of the issuers below.

The important fact is that liquidity has improved, with most issues trading at bid-offer spreads comparable to conventional counterparts, facilitating more active secondary market trading and improving the quality of market signals to issuers and investors alike.

Underlying this improvement in liquidity are several factors. The successful restructuring of Dubai World and other troubled issuers added a significant measure of confidence in the market and improved demand.

Improved balance sheets of Islamic financial institutions, whether lower loan to deposit ratios, higher capital adequacy ratios or successful recent issuance, provide necessary support and stability to market prices.

Liquidity across the GCC, confirmed by declining interbank borrowing rates and an increase in credit extended to the private sector, also continues to support prices, even in the face of serious contagion from global credit markets.

Economic growth in Malaysia, high reserves and capital flows into the country, as well as concerted and serious efforts to establish Kuala Lumpur as a global hub for Islamic finance, further support demand for Sukuk as well as the credit quality of many issuers.

Diversification

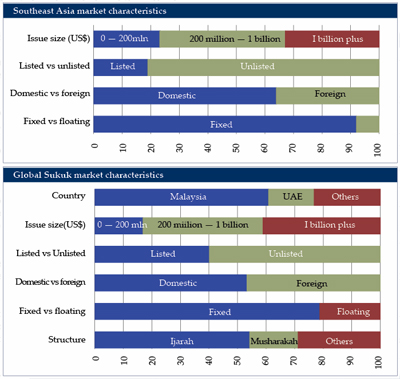

The Islamic financial product offering continues to develop rapidly and we have witnessed a material improvement in structural and legal standardization. Regulatory bodies have been quite successful at reforming and strengthening market regulation, standardization and authenticity (AAOIFI, IFSB and IIRA) making investments across borders possible as well as attractive.

Even though the disparity between MENA and Asian investment characteristics is still significant, this should diminish as both regions continue to grow and improve their respective financial architecture.

Countries and companies that care to issue Sukuk have precedent and templates that facilitate the process and reduce the costs of tapping a new investor base.

The increase in issuance, issuers, innovation and diversity is helping the market move deliberately to more authentic Shariah compliant products such that future Sukuk investment returns will resemble neither pure fixed income nor pure equity return profiles; an incredibly important objective of Islamic finance as well as a very attractive investment proposition to investors.

Outlook

The outlook for global Sukuk is very positive and exciting. Momentum is favorable and recent developments very constructive, encouraging and rewarding.

While we wait to welcome new issuers and innovations, it is important to focus on important governance issues that are not reflected in the growth numbers above.

New issuance should set better standards of transparency, not just from the companies raising funds, but from the special purpose vehicles created to issue the Sukuk.

Trust assets underlying Sukuk should be clearly identified and segregated from balance sheets, auditors and lawyers should maintain accounts and documentation post-issuance and regulators can be more aggressive in making sure contractual obligations underlying Sukuk are respected and enforced.

All market participants should contribute to the development of a culture of credit that encourages due diligence, and governments need to promote bankruptcy regimes that encourage investment and risk taking.

Mohieddine Kronfol is chief investment officer (fixed income/Sukuk) for Franklin Templeton Investments (ME) and a member of Franklin Templeton’s Fixed Income Group and Local Asset Management Team. He can be reached at

[email protected]

.