Last year, a number of milestones were achieved in the securitization market in the Gulf Cooperation Council region (GCC), including the successful completion of the first true sale residential “mortgage” backed securitization (by the Shariah compliant mortgage lender Tamweel PJSC).

As a result of these developments involving new assets in new jurisdictions, several legal and Shariah issues have been successfully resolved, paving the way for continued expansion of this market in the region. The following article summarizes some of the key issues raised in structuring Shariah compliant securitizations in the GCC.

The evolving legal landscape in the GCC is at the heart of a number of legal issues, which arise when structuring asset-backed products in the region. Although GCC countries in general do not have legislation that expressly regulates and/or permits securitizations, most of these jurisdictions recently enacted laws enabling the establishment of Shariah compliant true sale securitization structures that satisfy rating agency criteria (e.g. insolvency and property laws in the UAE, and Sukuk legislation in Kuwait).

Legal regimes in the GCC

In addition, a patchwork of different legal regimes may apply to a particular transaction, which adds complex layers to the legal analysis. For example, Dubai-based assets are subject to UAE federal law, Dubai emirate law and, in some instances, the laws of a particular free zone. In most instances, new regulations and the interplay between various layers of regulation have yet to be tested and, as such, require more detailed legal analysis of the likely impact of certain scenarios on the structure and, in order to accommodate rating agency criteria, may require additional structural features to compensate for certain uncertainties.

|

|

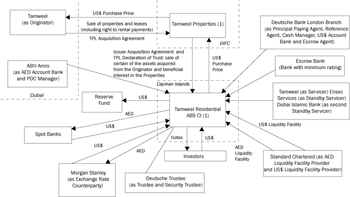

In order to accommodate these aspects of GCC legislation, a two-tiered special purpose vehicle (SPV) securitization structure can be used, whereby the originator transfers title in the relevant assets to a GCC-based SPV, which then transfers its rights and obligations as owner of the assets to an SPV established in a jurisdiction that recognizes trusts.

The new proposals for exempt companies in the Dubai International Financial Centre will assist in this regard. The trust is declared over the rights and obligations transferred to the second SPV, which then issues notes or Sukuk to investors.

Additional complexities are introduced into structuring securitizations in the GCC as a proportion of these transactions will have to be structured so as to comply with Shariah (e.g. if required by an originator or where investors are located in the GCC). Because Shariah compliant structures invariably require financing of assets, securitizations provide an ideal platform for compliant transactions.

Relevant Shariah requirements which impact securitization structures include prohibitions on interest-paying instruments or receivables (e.g. notes, GIC accounts and Istisna), restrictions on the inclusion of insurance-, guarantee- and hedging-like arrangements; limitations on tranching of debt; and restrictions on the nature of transferable assets (e.g. haram assets and debts cannot be transferred). In addition, the parties will have to determine who takes responsibility for monitoring the Shariah compliance for the life of a transaction.

In addition to legal and Shariah specific issues which arise in GCC-based securitizations, there are a number of additional factors relevant for securitizations in any emerging market, including potential transparency issues for non-local investors, relatively limited data on historical asset performance and consequently onerous due diligence investigations, currency convertibility issues and increased costs associated with regimes for the registration of title to and creating security over certain asset classes which have not been designed to accommodate structured financings.

In July 2007, the first true sale transaction in the UAE and the GCC region as a whole was completed with the US$210 million issuance of notes backed by Shariah compliant home financing products originated by Tamweel, the Dubai-based Islamic-compliant home finance provider. (See chart on previous page)

The issuer applied a portion of the proceeds of the issuance of the notes toward the consideration for such transfer by TPL (which used the proceeds to purchase the leases from Tamweel). The rental payments due under the leases served as the principal source of payments due under the notes. Tamweel continued to service the leases pursuant to a servicing agreement.

Growing, growing market

As a Shariah compliant institution, Tamweel requited a range of innovations and adjustments in order to securitize the leases (rather than conventional mortgage loans) originated in accordance with local law and practice, including thousands of existing and future post-dated lease payment checks and rent-control regulations.

TPL took on continuing obligations as lessor under the leases, which required detailed and tailored servicing procedures to accommodate this. In addition, the transaction tested for the first time a recently introduced property law in Dubai, creating a variety of legal and logistical hurdles. As the leases were UAE dirham-denominated and the notes were US dollar-denominated, currency swap arrangements appropriate for a Shariah compliant institution were also introduced.

Structuring conventional and Shariah compliant securitizations in the GCC poses particular difficulties and multi-tranched notes achieved an Aa2 from Moody’s and AA from Fitch, which is the highest ratings for any outstanding securities issued in the UAE.

Highly rated transactions like the Tamweel securitization mark significant milestones in the development of the securitization market in the GCC and are likely to pave the way for similar transactions.

[email protected]

. Allen & Overy regularly advises clients with an interest and active participation in Islamic finance transactions, across the spectrum of the banking, capital markets and leasing industries.