Having good liquidity management is a key prerequisite for sustaining financial stability and helping to alleviate any liquidity shortage.

As Islamic finance is moving to being part of the global interconnected financial system, financial markets across jurisdictions become more connected and economies become interlinked. Simply, joining up the dots is becoming more important. The lack of a global Islamic interbank market and liquidity management scheme has, according to some Islamic bankers, hampered the systemic development of the Islamic finance industry.

After the consequences of the global financial crisis, a renewed effort has been made to come up with a mechanism that is global, effective, and efficient as well as Shariah compliant. Regulators, industry organizations and market players have all stressed the urgent need for a global Islamic interbank market and a liquidity management scheme.

Challenges and issues

Liquidity management lies at the heart of confidence in Islamic financial institutions. Customers must be confident they can withdraw their deposit when they wish. If the ability of the bank to pay out on demand is questioned, all its business may be lost overnight.

The importance of liquidity transcends the individual institution, since a liquidity shortfall within any institution may invoke systemic repercussion causing harm to the whole financial stability of a country.

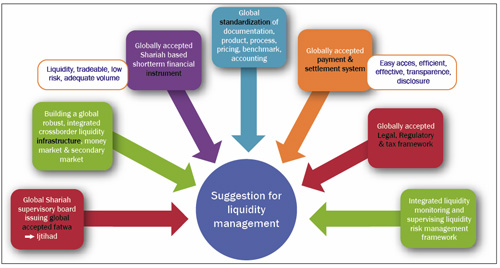

A globally accepted Shariah compliant liquidity management scheme

Vital for the development of the industry, creating such a scheme is challenging due to differing interpretations of Shariah rulings on financial matters across jurisdictions, which have led to differing methods of structuring or packaging financial instruments and the non-validity or non-recognition of some contracts or terms of practice in certain jurisdictions.

The process of harmonization and standardization of transactions across and within borders must be comprehensive. Shariah differences need to be resolved and a common design agreed among central banks. Consensus in fatwas may be overcome by the centralization of Shariah rulings in a central Islamic authority such as the Islamic Fiqh Academy of the Organisation of Islamic Cooperation. Furthermore, research entities such as IRTI and ISRA can collaborate. Ijtihad can also be the final option.

A

robust cross border liquidity market and infrastructure

Without adequate cross border liquidity market and infrastructure, Islamic banking institutions have poor management of cash, arising from the lack of a comprehensive Islamic interbank market with highly rated short-term tradable instruments.

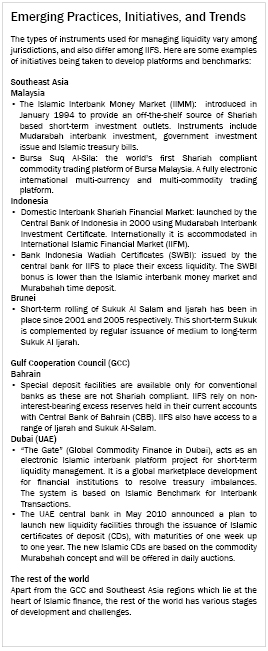

Without access to such a market, it is difficult for these institutions to manage their short-term liquidity needs; requiring them to maintain a larger amount of liquidity compared to their conventional counterparts. In Malaysia, such markets exist and have been the key to facilitating liquidity management.

Adequate availability of liquid short-term financial instruments

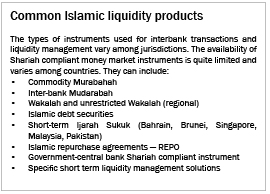

The availability of Shariah compliant money market instruments is limited and varies considerably among countries. Instruments such as Commodity Murabahah Interbank placement of funds under various profit sharing arrangements, and Islamic mutual funds, are the most commonly used instruments by institutions offering Islamic financial services (IIFS) in many jurisdictions.

The reliance on central banks for liquidity management is still low, as most short-term financing from central banks has not been adapted to comply with Shariah rules and principles.

Central banks should focus on encouraging the development and design of tradable Shariah compliant instruments which:

(a) Carry low risk and can set a benchmark for other instruments

(b) Can be issued in adequate volume and on a regular schedule to meet the needs of monetary policy, government financing and the portfolio needs of investors.

Robust global standards of documentation, product, process and accounting

Standardization of documentation, product, process and accounting is needed to promote consistent and efficient regulatory framework that will ensure unimpeded Islamic financial intermediation as well as liquidity management. The different standard used among jurisdictions is the main impediment. Global standardization is needed urgently so that an IIFS in one jurisdiction can transact easily with other jurisdictions.

Uniformity in legal, regulatory and tax framework

Legal frameworks for public debt and financing arrangements often do not explicitly allow for the design and issuance of Islamic financial instruments. Appropriate modifications to the law could facilitate Islamic money market development. A globally accepted legal, regulatory and tax framework would allow IIFS transactions to be easily conducted across jurisdictions.

Area of concerns in the legal, regulatory and tax framework are the trust laws, the banking and securities laws, the public debt laws, appropriate adjustments in the tax regime as well tax incentive or tax neutrality to facilitate the operation of Islamic money and capital markets.

An integrated payment and settlement system

The final challenge is to have an integrated and sophisticated payment and settlement system. Certain features within the existing payment and settlement system will require adaptations in order to ensure that payment transactions can be made within the rules of Shariah. In particular, adaptations are required in the types of collateral, the loss sharing arrangements, the interbank lending arrangements, and the availability of central bank lender of last resort facilities to support settlements by the IIFS.

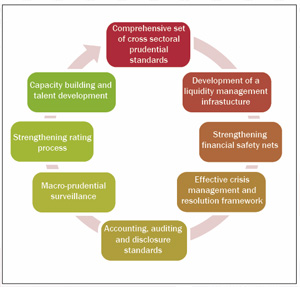

The current ongoing global financial and economic crisis has highlighted the weaknesses of the global financial regulatory and supervisory framework. Co-operation between regulators across jurisdictions is important in addressing potential systemic risks that have extended beyond the national and regional boundaries.

The IFSB, the Islamic Development Bank (IDB), and the Institute of Research and Training Institute (IRTI) have developed eight building blocks to strengthen the Islamic financial infrastructure. They target the stability and dynamism of the Islamic financial system through solid infrastructure components and strengthening key institutions.

Addressing these building blocks is vital in ensuring development of a robust and resilient Islamic financial system as all these eight areas are interconnected. Stability and contribution towards growth and development can be preserved if we adhere to these building blocks.

Daud Vicary presented this paper at the 2nd Islamic Financial Stability Forum in conjunction with 17th Meeting of Council of the IFSB on the 14th December 2010, Jeddah, Saudi Arabia.

Global Islamic finance leader

Deloitte

E-mail:

[email protected]

Daud Vicary Abdullah has been in the finance and consulting industry for more than 35 years, and has focused solely on Islamic finance since 2002.