After remaining stagnant for a number of years, the Islamic asset management sector is finally seeing some growth as investors dip a cautious toe back into the waters. Demand for Shariah compliant investment products is once again rising in the Middle East, and LAUREN MCAUGHTRY takes a look at the key trends and factors affecting the segment.

Islamic asset management is undoubtedly gathering pace. Ernst & Young estimates that around US$360-400 billion-worth of individual and institutional savings are available to the Islamic asset management industry, with around 70% concentrated in the Middle East. With global Islamic assets currently standing at an estimated US$1.3 trillion, PricewaterhouseCoopers estimates that the industry will grow at a compound annual growth rate of 15-20% until 2015, with the majority of the growth driven by asset management; and Sukuk investment in particular.

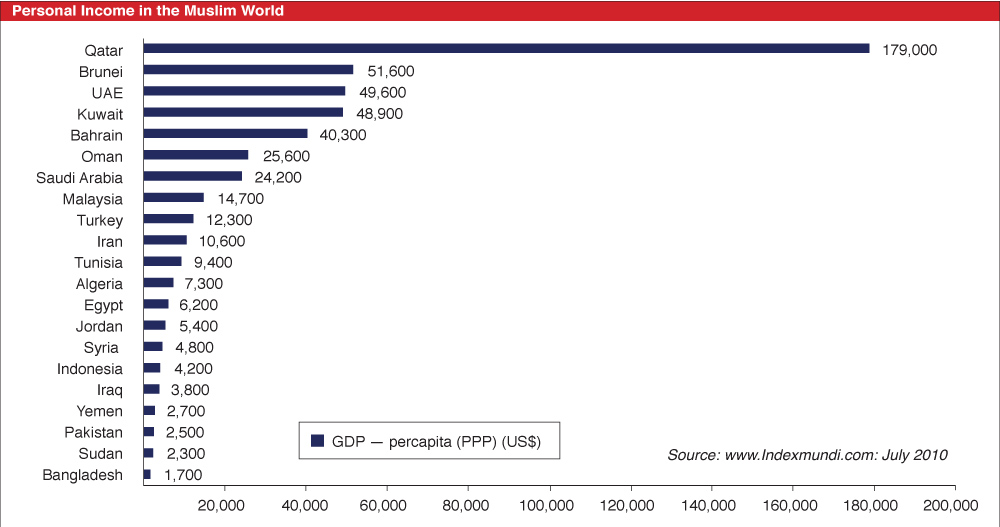

The market has enormous potential for growth, with Islamic finance currently accounting for less than 1.5% of total global assets and Middle East Muslims earning some of the highest per capita incomes in the world. There are around 450,000 millionaires in the Middle East, and according to the CapGemini RBC World Wealth Report 2012 the wealth of high net worth individuals in the region rose the most in 2011 compared with millionaires globally: by 0.7% to US$1.7 trillion.

With only around 28% of this currently invested Islamically, this makes Islamic asset management a vital segment of the nascent industry, as both Shariah compliant institutions and conventional fund centers alike seek to tap into this pool of wealth; and leading regional players including Bahrain, Qatar, Dubai and Abu Dhabi vie for dominance.

Key trends

So what has been happening in 2012 – what factors have impacted asset management in the region and how has the flow of wealth been affected?

The importance of sovereign wealth

Sovereign wealth funds are fundamental to the GCC asset management industry, accounting for 88% of existing investable assets and 74% of new assets, according to the 2012 Invesco Middle East Asset Management Study. In 2012, the impact of the Arab Spring made regional sovereign wealth funds keen to invest in local markets and boost public projects in order to maintain social stability. Particularly in Saudi Arabia and Qatar, government spending has increased significantly, despite volatile commodity prices that have affected income.

Flight to safety

The Arab Spring has also had an impact on the intra-regional flow of assets in the Middle East, with capital predominantly moving from the wider MENA region into the perceived safety of GCC states. According to a recent survey by Invesco Saudi Arabia, the UAE and Qatar have all seen significant inflows; while Oman, Kuwait and Bahrain have all lost assets. However, some industry players have noted that this is a temporary occurrence and this ‘hot money’ is simply sitting until it is safe to return rather than being invested or contributed in any meaningful way to the holding country’s economy.

Impact of financial crisis

Unsurprisingly, global financial conditions have had an impact on asset management in the region, with a number of institutions suffering significant losses particularly from European and US investments. However, it has also given asset managers in the region an opportunity to obtain new assets at low prices in new markets; such as the recent investments made by Qatar in UK real estate. Ongoing market volatility has maintained pressure on stakeholders however, and led to a preference for passive investment and benchmark tracking with a shift to a ‘core/satellite’ investment approach as investors retrench and seek to maintain their capital rather than take on risk.

Family offices account for a significant proportion of the asset management industry in the Middle East, representing around 40% of non-bankable assets in the region according to consultancy Booz & Co. In 2012 there was a significant trend towards capital flow into corporates and away from personal assets. Factors driving this flow include higher corporate returns and opportunities, along with short-term business funding requirements; which have led family offices to participate in corporate investment rather than focus on personal goals such as succession planning and diversification which in the current market environment could dilute shareholdings or require expensive and unnecessary bank financing.

Asset allocation

Real estate and Sukuk are traditionally the most popular forms of Islamic investment, and 2012 has shown little sign of bucking this trend. However, fund management after a stagnant few years is also on the rise, while alternative investments and particularly real estate investment trusts (REITs) have also seen an increase in investor interest.

2012 has been a record year for Sukuk and while Malaysia continues to dominate the market for issuance, the Middle East has clawed its way back into the competition with a couple of major benchmark issuances: such as the US$4 billion General Authority for Civil Aviation (GACA) Sukuk from Saudi Arabia in January. In the first half of 2012 Saudi Arabia accounted for 13% of global Sukuk, and HSBC has predicted that the Middle East region will continue to see high Sukuk volumes on the back of strong investor interest and relatively lower volatility.

Equity falters

In contrast, equity investment has unsurprisingly been less popular, due to the slowdown in equity worldwide over the past few years. However, the corporate space has put in a strong showing in 2012 and fundamentals are picking up with earnings rebounding, making it an asset class to watch for 2013.

Islamic funds

Think of Islamic asset management and the funds industry is probably the first to spring to mind. However, although the Islamic fund space has received much publicity in recent years, it has not yet achieved its full potential. There are currently only 765 Islamic mutual funds available globally, compared to over 60,000 conventional funds. Growth in the sector has also slowed. According to Ernst & Young in 2007 there were 173 Islamic funds launched, compared to 78 in 2008 and just 29 in 2009. However, this is in tandem with the conventional sector, which has also seen a slowdown during the financial crisis.

Equity funds are currently the most popular in the Islamic mutual fund space, accounting for 35% of total funds, followed by money market funds at 14%, fixed income at 14%, commodities at 12% and alternative and feeder funds at 6%.

However, with over 450,000 millionaires in the Middle East alone accounting for around US$1.7 trillion of available assets, there is no doubt that the current Islamic fund sector is failing to meet demand. The global Islamic funds industry currently only has around US$60 billion of assets under management, compared with US$22 trillion in the conventional space; signifying an area of huge potential.

The Islamic funds space has seen a number of positive trends over the past year which suggest a positive note for the future: including an increase in the number of funds, a diversification of asset classes and investment strategies, and most importantly the development of a more comprehensive and holistic wealth management service.

The rise of local wealth management

One of the most significant trends in Islamic asset management has been the evolution towards a more comprehensive wealth management approach. According to some sources the wealth management industry in the MENA region represents upwards of a US$800 billion opportunity; lying primarily in two key wealth hotspots of Turkey and Saudi Arabia, along with a second tier of Egypt and the UAE which also represent a vital pool of wealth – estimated at around US$60-110 billion in investable assets held by the richest 10% in each country.

However, especially in the Middle East, affluent investors often hold their money abroad and invest primarily in ‘hard’ assets such as real estate, commodities and foreign corporate shareholdings. There is a strong tendency to invest abroad, with an estimated 70% of wealth sent overseas (compared to 3% invested overseas by US and Japan and 25% from Europe). In addition, in the past affluent Middle East investors have been targeted primarily by experienced global asset managers and wealth advisors such as Merrill Lynch, exacerbating this outflow, while local advisors and regional banks have failed to offer a holistic management service that meets all their needs and have thus lost out on this business.

Increasingly however, Middle Eastern policymakers and bankers have been working to develop a local wealth management industry which keeps investments at home rather than allowing them to flow abroad. In October 2012 Safa Investment Services launched what it claims to be the world’s first independent global Islamic wealth and asset management brand, focusing on a range of ‘best of class’ Shariah compliant assets. According to John Sandwick, the manager of Safa Investment Services: “Professionally managed assets worldwide are now around US$80 trillion, of which Muslims own at least US$3 trillion. What is striking is that almost none of that is invested with any respect for Shariah.”

Challenges

However, the Islamic asset management industry still has a long way to go before it can truly capitalize on its potential. Key challenges remain which inhibit its growth: most importantly the continued problems of standardization and harmonization in terms of regulation, tax and legal treatment.

What next?

However, despite ongoing challenges the future remains bright for 2013. Continued volatilty in the conventional bond and equity markets combined with global economic uncertainty especially around the Eurozone crisis has led to a greater interest in Islamic finance, resulting in increased investment flows from investors seeking to diversify away from their traditional holdings. In the current economic environment wealth preservation and conservative strategies are paramount, with many investors seeking to reduce their exposure to conventional risk. At the same time, Islamic investors are finding new and increasingly sophisticated structures and asset classes available to them, and are dipping their toes into exciting new waters. Next year, we can hope for even greater things.