One of the key developments in the insurance market has been the rise of bancassurance, a distribution channel which offers a means of efficiently accessing a wider customer base. As Islamic insurance grows and overall penetration increases, bancaTakaful is poised for further growth, especially in its key Southeast Asian markets of Indonesia and Malaysia. LAUREN MCAUGHTRY looks at the current trends.

Southeast Asia has huge potential for Takaful, with double-digit growth figures seen on an annual basis driven by a low insurance penetration, a growing awareness of Shariah compliant solutions and increased efficiency and accessibility of sales channels. Developing the efficiency of sales channels is indeed a primary issue for Takaful operators and bancaTakaful has been gradually increasing its share of the market as it offers opportunities to capture customer segments often missed by traditional agency forces. As the reach of Islamic banking services grows, so too does the spread of bancaTakaful, suggesting that this trend is only on the up.

Malaysia: A leading market

Malaysia is one of the largest Takaful markets in the world and Bank Negara Malaysia, the central bank, believes that the growth of bancaTakaful will continue to reinforce the market. “BancaTakaful, which uses bancassurance as a key growth channel for Shariah compliant insurance, is seeing positive growth for general Takaful and is now the leading distribution channel for Family Takaful products in Malaysia, accounting for 50.3% of contributions in September 2010,” according to the late deputy governor, Mohd Razif Abd Kadir. “With the development of bancaTakaful, consumers will have access to integrated financial services from banking institutions in a cost-effective manner.”

This success has allowed Malaysia to play a key role in promoting and developing bancaTakaful growth in neighboring countries, particularly in Indonesia, where several Malaysian Takaful operators have already entered the market. Leading provider Great Eastern Takaful entered Indonesia in 2011 in collaboration with OCBC Bank, which has over 400 branches in the country. In 2012 the group reported “encouraging growth in the bancassurance channel”. It currently derives a reported 10% of its revenue from bancaTakaful.

Indonesia: Growth and opportunity

Bancassurance was first introduced in Indonesia in the 1990s and has evolved into a successful channel driven by the increased spread of banking services, which has encouraged the purchase of insurance through banks due to its convenience and competitive pricing. According to the Indonesia Life Insurance Association or Asosiasi Asuransi Jiwa Indonesia (AAJI), bancassurance currently accounts for around 37.26% of the total premium income of life insurance in Indonesia; and almost every provider now offers a bancassurance service. Bank Indonesia, the central bank, has a Shariah unit (BNI Syariah) which operates in conjunction with BNI Life Syariah to offer bancaTakaful through 21 outlets. Bank Mandiri, one of the country’s biggest banks in terms of assets, loans and deposits, in 2003 collaborated with French provider AXA to combine their distribution channels and offer unit-linked Takaful products.

Indonesia’s insurance market is seeing fast-growing demand across all segments; and active competition is building offerings and bringing out new products and services. Increasing financial awareness along with a population shift from rural to urban areas is also making it easier for insurers to access customers – the World Bank has estimated that in Indonesia the urban population will grow from 42% to 60% from 2005-15 and is seeing annual growth of around 3.4%. The market is also being boosted by a strong government push for corporate, health and pension coverage; and by the attractive returns on unit-linked products due to the rapid growth of the Indonesian stock market, which saw 100% growth between 2006-11 on its main index. Indonesia has a low level of life insurance penetration at just 1% overall compared to 3% for Malaysia and over 7% for developed markets, making it a tempting opportunity for growth. In addition, premiums have been growing faster than the number of policies, thus increasing the average premium per policy – both for Shariah and conventional insurance, and for group and individual.

Although individual Shariah insurance has seen strong growth, it is still very small in terms of asset size and premium. BancaTakaful can play a significant role in driving this growth, and the channel has seen a good performance over the last five years. Between 2007-10, the bancassurance channel in Indonesia saw compound annual growth of 38%, from IDR44 trillion (US$4.5 billion) to IDR76 trillion (US$7.77 billion), compared to just 13% for other channels. In 2010 bancassurance accounted for around 35% of all life insurance sales in the country.

The mass affluent market is a core component of insurance market growth in Indonesia, with up to 500 million potential customers and an estimated market size of up to IDR28 trillion (US$2.84 billion), or 34% of the total market. FWU Group splits the market into two segments: advice seekers and self-directed purchasers. Of these, advice seekers account for around IDR15 trillion (US$1.52 billion) and tend to prefer to buy from banks and advisory agents. Self-directed purchasers will use online channels to research, but will also prefer to buy direct from banks and agents, suggesting that bancaTakaful remains a vital part of developing the sector.

Product innovation

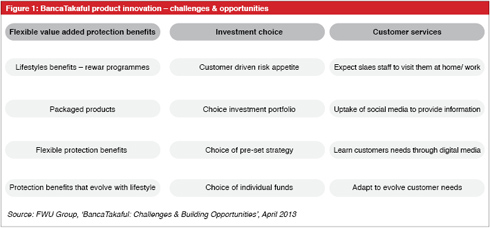

A key trend in bancaTakaful is product innovation. The general perception of Takaful is changing, and instead of being viewed just a means of protection it is becoming linked with the whole theme of wealth management and overall financial planning. This has led to demand for a far wider range of customized and sophisticated products, from investment-linked and wealth management services to annuities, medical coverage, specific ladies plans, child protection, personalized coverage and even microTakaful for the lower-income segments. As products become more sophisticated customers are also demanding better service and stronger relationships with their providers; and banks are in an ideal position to offer this, leveraging on their existing reputation and overall financial expertise and using their extended reach to access customers through marketing strategies.

Sohail Jaffer, a partner at FWU Global Takaful Solutions, comments that: “The customers of today seek products that match evolving needs that arise from their lifestyle. This creates several challenges and opportunities.” As customers evolve through different life stages, their needs change. In terms of protection, the type and the amount of cover required changes. In terms of long-term savings, age also alters customer needs. Younger customers have less investable income but can take more investment risk. As they grow, marry and settle down, their risk appetite declines but their investable income grows. Sohail explains that: “Customers should be offered the flexibility to select their own amount of investment risk, and choose the features of their own benefits.”

According to Bank Negara Malaysia, new business contributions from investment-linked products increased to US$125.3 million in 2010 from US$113 million in 2009, making it one of the most popular asset classes. Investment-linked products currently accounted for around 15.6% of total new Takaful business contributions. As customers often have a history with their bank and turn to banks for investment advice, this makes the bancaTakaful channel even more important.

The digital age

While the bancaTakaful channel is growing, however, there are still challenges to be met. Ernst & Young’s Global Consumer Banking Survey 2011 noted that: “There is considerable room for improvement in the levels of channel efficiency, personalization and integration that banks offer their customers.” This has led to an increased focus on developing customer-centric processes, and the growth of digital systems has revolutionized this trend.

“In a world where customers are in full control of your brand, it is important to go digital,” explains Sohail. “Information is the key to delivering solutions that customers need and want. Digital applications provide vital insight into the lifestyle needs of customers.”

The challenge is to evolve as quickly as possible, as customers become more informed and better able to access information and make choices based on their personal requirements. “Harness the power of social media such as Twitter and Facebook to understand and keep up to date with what customers are thinking,” suggests Sohail. “Use this information to develop improved solutions.”

Digital applications enhance customer service in two main ways. First at the point of sale, digital service helps to facilitate the sales process and provide customer convenience. Secondly, digital applications allow this data to be collected and analysed – capturing information not just from clients but from social media sources and networks; thus giving insight into customer segments and demands, monitoring sales, and therefore improving customer service and assisting with more appropriate and targeted product design.

At the point of sale, digital applications allow the agent to make the most of any sales opportunity, and to transact whenever and wherever is convenient to the customer, giving greater ease of access. It allows for immediate plan issuance and the conclusion of sales on the spot, thus saving the customer time and boosting the overall conversation ratio of visits to sales. This ease of distribution allows for a direct sales force, which is not only appealing to customers but offers a number of key benefits to the provider including enhanced productivity and efficiency of the sales agents, and the administration and underwriting of policies online.

Sohail concludes that: “Digital applications are changing the world we live in; allowing us to learn about evolving customer requirements and give them the solutions they need. All customers are not the same – digital solutions allow the provider to give clients a choice based on their age and lifestyle.”

Sohail Jaffer

Deputy CEO, FWU Global Takaful Solutions

Al Fattan Currency House,Tower 2,

Dubai International Financial Centre

PO Box 482026, Dubai, UAE

Tel: +9714 4175 422

Email:

[email protected]