Shariah compliant treasury management for a multilateral development bank like the Islamic Corporation for the Development of the Private Sector (ICD) poses specific challenges. The innovative solutions applied at the ICD provide valuable lessons which can be applied to any Islamic bank with normal treasury responsibilities. The article highlights the techniques and issues involved.

The ICD treasury division is entrusted with the responsibility of managing the liquidity risk and market risk of the ICD as a whole.

The division uses Wakalah and commodity Murabahah structures for its liquidity management. This involves interbank money market operations for resource mobilization and for placements.

The Wakalah (agency) agreement is suitable for established ‘big name’ Islamic banks, who have the necessary expertise to manage funds employing a Shariah compliant pool of assets. Under this mode the Wakeel (agent), having accepted the appointment as the Muwakkil (principal)’s agent, invests the Muwakkil’s funds in the Wakeel’s pool of assets, treasury pool of assets, or any other assets authorised by the Muwakkil in accordance with the rules and principles of Islamic Shariah, as determined by the Shariah supervisory board of the Wakeel.

The Wakeel is expected to generate an expected rate of profit and is entitled to a Wakeel fee (agency fee). It is also entitled to keep any additional profit as an incentive if it manages to generate more than the expected profit rate.

The commodity Murabahah structure, on the other hand, allows the ICD treasury department to manage its liquidity through the purchase and sale of non-precious metals (such as rhodium, palladium, copper etc.) and Shariah-approved agricultural commodities (such as palm, palm oil, cocoa beans, rubber etc.) This transaction is based on the ‘cost plus’ concept of purchasing commodities at spot on deferred payment terms with additional profit.

It is not the buyer’s intention to utilize the benefit from the purchased commodity, rather it is to enable the buyer to attain liquidity from sale of the same, usually on the same spot date but at a later time (i.e. after it purchases and takes constructive possession of the commodities and all associated risks/rewards involved therein before it decides to sell).

The ICD usually uses the commodity Murabahah mode for liquidity management in the countries where an Islamic banking law is not present or not mature enough, but where counterparts are allowed by regulators to take the constructive possession of commodities. Regulators of many countries do not allow counterparts, especially banks, to purchase commodities under their own names.

Placements under commodity Murabahah

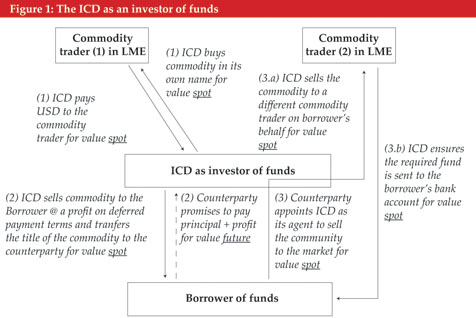

The following are the key steps employed when the ICD places funds with counterparts under the commodity Murabahah structure. They are defined below:

(1) The ICD will buy any metal commodity under the ICD’s name for the placement amount (i.e. principal amount) on spot.

(2) The ICD will offer to the counterparty as to whether it wants to buy the commodity on spot at the principal amount and pay the principal + profit to the ICD, after a deferred date, e.g. one year.(3) Once the counterparty agrees, the ICD will sell the commodity to the counterparty on spot and the title of the commodity will be legally and constructively transferred to the counterparty.(4) Then, according to the Master Commodity Murabahah agreement, the counterparty will appoint the ICD as its agent and will ask the ICD to sell the commodity in the market on spot to the counterparty.(5) The ICD will sell the commodity on the counterparty’s behalf on spot and the proceeds of the principal will be credited to the counterparty’s account on spot, thereby enabling the counterparty to meets its liquidity needs.

(6) After one year the counterparty will repay the principal + profit to the ICD (or in installments, whatever is agreed).

See Figure 1 for an illustration of the mechanics.

Resource mobilization under commodity Murabahah

The following key steps are applied when the ICD borrows funds from its counterparties under the commodity Murabahah structure:

(1) The lender appoints the ICD as its agent to buy the commodity, from the market, under the name of the lender for value spot, and the lender transfers the funds (the lending amount) to the ICD’s account.

(2) The ICD buys the commodity under the lender’s name for value spot and pays to the commodity trader.

(3) The lender offers to the ICD and the ICD has the option to purchase the commodity on spot delivery and deferred payment basis at a specific profit rate.

(4) Once the ICD agrees to pay the principal + profit at future, the title of the commodity is transferred to the ICD’s Name, according to the schedules of the Master Agreement.

(5) The ICD sells the commodity to another commodity trader, for value spot, and receives the US dollar lending amount.

(6) The ICD pays the principal + profit, according to the repayment terms agreed with the lender.

See Figure 2 for an illustration of the mechanics.

In addition to managing the liquidity risk of the ICD, the treasury division is also in the process of launching an Islamic foreign exchange forward contract and an Islamic profit rate swap in order to manage foreign exchange risk and profit rate fluctuation risk. The former is a Waad-based structure and the latter is based on a series of commodity Murabahah transactions

All this is being done using Islamic modes of finance.