The Shariah dollar may be gaining traction but with one in five of the world’s population set to be over 60 by 2050, the silver dollar is more powerful still. Join the two together and what you have is a movement that could sweep the Islamic asset management industry and revolutionize Islamic institutional investment.

An aging population

The longevity issue is becoming a worldwide problem. And although more developed countries have the oldest population profiles at the present time, the most rapidly aging populations are in less developed countries and emerging markets. According to the World Health Organization (WHO), between 2010 and 2050, the number of older people in less developed countries is projected to increase more than 250%, compared with a 71% increase in developed countries.

Sheikh Faizal Ahmed Manjoo, a specialist in Islamic and conventional commercial and pensions law and the CEO of UK-based Minarah MultiConsulting, has warns that: “Not only are Muslim communities beginning to follow the same longevity risk pattern found in OECD countries, but the demographic change is happening faster than in the West, giving societies little time to adapt.”

A growing problem

According to population projections from Pew Research Center the global Muslim population is expected to increase by about 35% in the next 20 years to 2.2 billion by 2030, growing at a rate of around 1.5% per year – twice the rate of the non-Muslim population – to make up 26.4% of a projected 8.3 billion in 2030. Concurrently, Pew predicts in a report on The Future of the Global Muslim Population (2011) that between 1999 and 2030 the number of Muslims under 30 in Muslim-majority countries will have dropped from 68.4% to 49.6%.

“The forecast is alarming. If Muslim countries don’t start planning to avoid the aging population problems that OECD countries now face, the effects could be disastrous,” believes Manjoo. “The Muslim world does not have a pensions culture or industry, let alone a discussion about longevity risk.”

A vital component

With longevity a worldwide trend, the issue of a decline in the elderly dependency ratio (the ratio between the elderly and the working age population) is becoming acute. To tackle this problem, the United Nations (UN) in its 2010 report on Rethinking Poverty recommended a three-pillar proposal:

-

State pensions;

-

Occupational pensions with the employer contributing towards the pension plan; and

-

Private income sources.

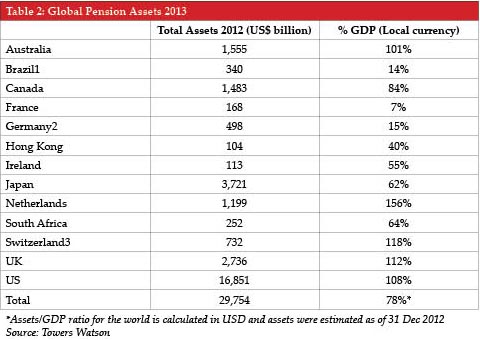

In the conventional industry, global pension assets amounted to around US$29.7 trillion in 2012, according to the Towers Watson Global Pension Assets Study 2013. This was an 8.9% increase over 2011, and accounted to 78% of total GDP. The largest pensions markets (the US, Japan and the UK) accounted for 56.6%, 12.5% and 9.2% of total pensions assets, respectively; and saw 2012 growth of 10%, 0.5% and 9.9%.

And as the global population ages, these figures are consistently increasing. Between 2002-12, global pensions assets grew at an average compound rate of 8.3%, with the fastest growth in Hong Kong followed by Brazil and South Africa.

Retirement potential

This highlights not only the vital importance of a sturdy pensions sector to cater to the increasing numbers nearing retirement age, but the invaluable role the institutional pensions industry plays in supporting the global asset management sector.

For example, according to the Towers Watson survey, assets under management of the top 300 conventional pension funds represent 46.7% of total global pensions assets, with the top 20 accounting for 18.5% or around US$5.4 trillion. In the US, the top 10 pension funds represent 9.1% of the market’s total assets under management, while in the UK they represent 16.4%. In Japan, where the Government Pension Investment Fund holds over a third of pension assets, this figure reaches 55.9%. The opportunities for the Islamic asset management industry backed by a state-led Shariah compliant pension fund and supported by the private sector are clear.

Trailing behind

But as yet, the Shariah compliant industry has signally failed to step up to the challenge. According to data from the Malaysia International Islamic Financial Centre, global assets under management for Islamic funds are estimated to have reached US$73.7 billion as at the 9th December 2013, a growth of 10.2% over the previous year. While this represents a four-fold increase over the past five years, with 78 new funds introduced in 2013 alone, the total figure represents a miniscule fraction compared to the conventional industry.

The Thomson Reuters Global Islamic Asset Management Report 2014 highlighted that: “The entrance of pension funds could double the size of the industry,” while EY has confirmed that pent-up demand for Islamic pension programs could add US$160-190 billion to the Islamic asset management sector – almost tripling its current size.

“This would be a major ‘shot in the arm’ for the Islamic asset management industry, which suffers from lack of scale,” explained Ashar Nazim, a partner at the EY global Islamic banking center in Bahrain, to Islamic Finance

news. “Most of the 700+ Islamic asset managers today have less than US$100 million in assets under management, which is not sustainable. In comparison, the pension fund segment is a major and active player in conventional capital markets.”

State-led revolution

The Islamic asset management industry has long been constrained by a dearth of institutional investment, which has led to a shortage of firms able to hold such large inflows. “The trend is positive but the size of the Islamic fund management industry is miniscule compared to the requirements of the pension industry. This is the primary challenge,” confirmed Ashar.

However, if some of the big country players in Islamic finance launched state-backed Shariah compliant pensions, this would result in a massive wave of institutional funds looking for Islamic investments. Once these state-backed pension funds pushed the market to critical mass, the private pension funds sector would be likely to follow. As Islamic institutions themselves came to recognize the opportunities for Islamic institutional investment on the private side this created they too would then be more likely enter the market, and this could revolutionize the asset management industry.

The road to retirement

Progress is being made, with Islamic pensions becoming a priority in several Muslim-majority countries across the world. “With the maturity of the Sukuk market and Shariah compliant equity indices, as well as technology available to screen conventional indices to carve out Islamic sub-indices, there appears to be sufficient assets available for many of the pension funds to take the first step towards Shariah compliant propositions,” noted Ashar.

In several officially secular countries this is being driven by the private sector rather than government-led. “Several fast-growth emerging markets including Malaysia, Saudi Arabia and UAE are seeing strong demand for retirement plans that are Shariah compliant,” confirmed EY in a recent report.

In Turkey, recent government reforms including a 25% government contribution to private pension premium payments have pushed private pension contributors up to almost 3.8 million from 3.1 million in December last year. According to the Capital Markets Board of Turkey, Islamic pension assets reached US$175 million in September last year (around 1.5% of the industry). Asya Emeklilik, the Islamic pension unit of Bank Asya, now has over 100,000 clients and its fund size is TRY111.6 million (US$55 million). New players are now joining the 17-strong Turkish pension providers, including Katilim Emeklilik ve Haya, an Islamic venture between AlBaraka Turk and Kuveyt Turk announced in March 2013 which received the required approval from the Turkish Treasury in December last year.

Pakistan, in comparisons, launched a state-run Voluntary Pension Scheme (VPS) in 2005 which now holds PKR3.4 billion (US$32.4 million) in Islamic assets – around 60% of total VPS assets. The largest of the seven VPS managers, Meezan Bank, has seen its Islamic assets under management double in the last year and its Islamic pension fund is almost three times the size of its conventional equivalent.

Developments are also occurring in the UAE, where the drive towards creating an Islamic economic center has been much-publicized. Dubai recently proposed a scheme to create a Shariah compliant retirement savings scheme for expatriates, which it hopes would boost the domestic Islamic funds industry.

Industry champion

However, the absence of a robust regulatory framework, the small number of Islamic asset managers and the absence of an ‘industry champion’ has thus far restrained the industry from realizing its full potential.

Despite private sector developments, it must be the state which drives the industry forward to reach an economy of scale. Ashar explained that: “For a nascent industry like this, you need an industry champion to ‘pilot’ the program. The only practical option is for government-linked pension funds to take the lead; possibly with support from multilateral institutions. The private sector’s contribution would be material only in the longer-term.”

Malaysia is at the head of the pack in this regard. The country launched its Private Retirement Scheme last year, in which 13 out of 36 funds are now Islamic. According to Ranjit Singh, the chairman of the Securities Commission, the scheme had 30,500 accountholders as of June 2013 with total assets of around RM97.5 million (US$29.5 million), which it expects to grow to around RM30 billion (US$9.1 billion) in the next decade. Ashar agreed that: “Malaysia is well-positioned to provide leadership to this segment.”

A driving force

The government also is reportedly considering the channeling of RM7 billion (US$2.1 billion) from the state’s Employees’ Provident Fund to Islamic fund managers. EPF already invests around a third of its US$160 billion portfolio in Islamic assets, and in December 2013 the fund reportedly hired consultants including EY and ZICO Law to study the possibility of establishing one of the world’s first state-backed pension funds – which could be the revolutionary kickstarter that the industry needs, providing a model for other countries to follow.

Vive la revolucion!

And the demand may already be there: “There is a clear preference by individuals in these markets to manage their financial affairs in a Shariah compliant manner. This segment represents anywhere between 10- 70% of the overall market, which is sizeable,” explained Ashar. All the sector needs is a new driving force to lead the way.

“Traditionally, the focus has been on switching their banking relationship from conventional to Islamic. Only now are we beginning to see a greater awareness regarding wealth management and retirement planning, which in turn is encouraging public pension funds to consider offering Shariah compliant alternatives.”

Although Ashar warned that “regulatory support will be critical to help sustain the momentum,” it seems as if with Malaysia leading the way and momentum building in Muslim markets across the globe, 2014 could be the year that the Islamic pensions industry finally takes off. And if this happens, the knock-on effects on the Islamic asset management market and institutional investment trends will ripple throughout the industry – driving what could be a very real revolution. — LM