Islamic venture capital and private equity funds have shown tremendous growth in the last few years and are said to be among the fastest-growing areas within the Shariah banking industry.

In Malaysia, venture capital and private equity are principally structured on the basis of issuance of preference shares. Section 5 of the Malaysian Companies Act, 1965 defines preference share as:

“… a share by whatever name called, which does not entitle the holder thereof to the right to vote at general meeting or to any right to participate beyond a specified amount in any distribution whether by way of dividend, or on redemption, in a winding up, or otherwise;”

One of the common features of preference share is its cumulative feature, whereby when a company fails to pay a dividend, the cumulative preference shareholders are entitled to receive this missed dividend payment when a dividend is next declared. The holders are also entitled to the current dividend if sufficient cash is available. These payments take priority over the claims of ordinary shareholders.

The above feature of preference share has become an interesting point of discussion in structuring Musharakah venture capital and private equity as to whether the same complies with the requirements of Shariah.

The Shariah Advisory Council of the Securities Commission Malaysia has ruled that non-cumulative preference shares are permissible based on tanazul, where the right to profit of the ordinary shareholder is willingly given to a preference shareholder. Tanazul is broadly defined as cessation of the right to claim.

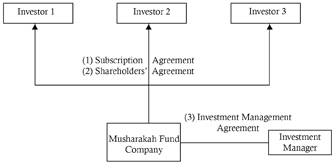

Tanazul is also known as isqat haq, which means to drop claims to a right. In the transaction structure below, the above principle of Tanazul can be applied.

The Shariah adviser shall endorse the structure and all legal documentation before they are executed. He shall also endorse the guidelines and operating manual.

Generally, the key features of the arrangement shall contain the following terms and conditions:

(1) Subscription agreement

This is the primary agreement to reflect, inter alia, the following salient features:

(a) Conditions precedent

Increase of paid-up capital, registration of the Musharakah fund company with the relevant authority, and amendments to the memorandum and articles of association of the Musharakah fund company are among the important conditions precedent to be fulfilled.(b) Rights attaching to ordinary shares

(i) The investors as holders of the ordinary shares, to the extent that profit is available for distribution and subject to dividend in respect of the RPS (redeemable preference shares) has been paid, shall be entitled to receive out of the profits of the Musharakah fund company resolved to be distributed.

(ii) The investors as holders of the ordinary shares shall be entitled to one vote in respect of each ordinary share held.

(c) Features of RPS

(i) The RPS shall have its par value and premium.

(ii) The tenor of the RPS is for the period of the fund life and is redeemable at the option of the Musharakah fund company.

(iii) The holder of RPS shall not be entitled to receive notice of, and to attend all general meetings of the Musharakah fund company and to speak before such meetings and shall not be entitled to vote at such meetings.

(iv) The holders of RPS shall be entitled to receive information such as accounts, investment update, progress and performance of the Musharakah fund’s and/or such other information from time to time.

(v) The RPS shall be issued free from all charges, liens or other encumbrances whatsoever and in the event of liquidation of the Musharakah fund company, the RPS shall rank in priority to the ordinary shares in the Musharakah fund company in relation to preferential dividend and repayment of capital together with arrears, if any, provided that there shall be no further right to participate in the surplus assets or profits of the Musharakah fund company.

(d) Tanazul

The investors, being the holders of the ordinary shares by way of Tanazul, agree to waive their rights in respect of preferential treatment conferred upon the holders of RPS under paragraph (c)(v) above.(e) Redemption of RPS

Except on the liquidation of the Musharakah fund company, redemption of the RPS shall only be made by the Musharakah fund company proportionate to the number of RPS held by each investor, by issuing a redemption notice to the investors.

(2) Shareholders’ agreement

This is the agreement executed to reflect, inter alia, the following salient features:

(a) Musharakah fund

This clause, inter alia, mentions the endorsement of the Shariah adviser, the investment objective and the fund size.(b) Board of directors

The role of the board, its composition, appointment of the chairman, quorum, voting and decision making are among the clauses reflected herein.(c) Investment committee

This clause sets out, inter alia, the role of the committee, its composition, quorum and decision making.(d)Shariah adviser and Shariah governance

(i) The Shariah adviser shall be responsible for the following:

(a) advising the Musharakah fund company on matters relating to Shariah compliance issues in relation to the Musharakah fund; and

(b) monitoring and ensuring that the investments and the activities of the Musharakah fund comply with Shariah principles.

(ii) The list of businesses which are inconsistent with Shariah principles are set out in this clause.

(3) Investment management agreement

This agreement reflects, inter alia, the following salient features:

(a) Appointment of investment manager and authority pursuant to Wakalah concept

(i) The Musharakah fund company agrees to appoint the investment manager and the investment manager hereby agrees to accept its appointment, by way of Wakalah, as the exclusive manager to provide the prescribed services.

(ii) Wakalah is a contract that gives a person the power to nominate someone to act on his behalf, as long as he is alive, based on the agreed terms and conditions.

(b) Services to be rendered by investment manager

The Musharakah fund company confers on the investment manager the right to arrange, implement, operate, administer and manage the Musharakah fund for and on behalf of the Musharakah fund company throughout the duration of the agreement.(c) Management fee

As consideration for the due performance by the investment manager of the services under the Shariah concept of Wakalah, the Musharakah fund company agrees to pay an agreed management fee per annum.

In conclusion, the Shariah concept of Musharakah has evolved phenomenally from the first Musharakah bonds issued by Sarawak Shell Berhad in 1990 for RM560 million (US$173 million) to the recent venture capital and private equity funds structured under such concept.

Ahmad Lutfi Abdull Mutalip is partner/head of financial services at Azmi & Associates. He can be contacted at +603 2118 5002 or via email at

[email protected]

. Visit

www.azmilaw.com