The Islamic funds industry is both a potential goldmine and a moving target, to mix metaphors. LAUREN MCAUGHTRY looks at developments across some of the most attractive domiciles for Shariah compliant funds in these troubled times, and evaluates the best and brightest for the coming years.

While the perennial attraction of offshore funds remains viable across the board in both the Islamic and conventional industries, its allure has in recent years been made all the more pertinent by the political instablity across some of the most popular regions for Islamic finance. Market turbulence following the Arab Spring and the recent waves of unrest across North Africa, not to mention the perennially shaky South Asia region covering countries such as Pakistan, have highlighted the need for fund managers as well as investors in these regions to protect their booming Islamic investments through stable fund domiciles.

Industry boom

The Middle East and Asia have for years used offshore centers to organize and structure their investments, and as the profile and coverage of Islamic finance grows it is only natural that investors in these two strongholds demand increasing levels of Shariah compliant expertise from their offshore providers as well as their onshore investments. Particularly popular are offshore Sukuk and Islamic funds, where the beneficial tax, legal, cost and regulatory efficiencies in offshore jurisdictions can offer significant benefits.

Increasingly, leading Islamic fund houses and asset managers are seeing demand for offshore funds as investors seek reliablity. AmInvest, one of the top fund houses in Malaysia and the asset management arm of AMMB Holdings, held around RM34.4 billion (US$10.4 billion) as at the 30th June 2013. Of its 82 funds, 42 are Islamic and its Islamic assets under management (AUM) have seen a 25% growth over the past year, surpassing the industry average of 22%. “Our strategic focus is to provide global Shariah compliant investment solutions to global investors and to grow our global footprint. As at April 2013, 64% of AmInvest’s total Islamic AUM was invested in Islamic offshore funds, primarily in Sukuk,” said Maznah Mahbob, CEO of AmInvest.

However, the traditional advantages that attract investors to many of the traditional offshore centers do not necessarily apply for Islamic finance. Sophistication, expertise, experience and complex structuring ability in the conventional sector do not always translate into Shariah compliant success.

What makes an offshore center?

Originally, an offshore center referred to a variety of (usually island) jurisdictions which offered low taxes, favorable regulatory regimes and low establishment costs. However, while in the previous decades offshore centers were preferred as securitization vehicles and fund domiciles. Now, their remit encompasses a far wider arena: including “repackaging securities, aircraft and shipping finance and insurance” according to a well-known offshore Islamic funds lawyer.

The IMF defines an offshore center as: ”A country or jurisdiction that provides financial services to nonresidents on a scale that is incommensurate with the size and the financing of its domestic economy.” However in the same working paper it also admits that this definition would include areas such as the UK, the US and Singapore, which in fact due to their large populations and financial sophistication and range are usually counted as ‘onshore’. The definition, it is clear, is up for debate.

In terms of Islamic finance, the waters become even more murky, as some leading Islamic finance jurisdictions such as some of the smaller Gulf states in fact come under the same heading. So what do we really mean when we refer to an offshore jurisdiction for Islamic funds?

There are many well-known offshore centeres: including European destinations such as Luxembourg, Ireland and the Channel Islands; along with the better known Caribbean domiciles such as the Cayman islands, British Virgin Islands, and Netherlands Antilles; and newer entrants such as Malta, Mauritius and Cyprus. However, not all of these locations have succeeded in attracting or retaining Shariah compliant funds.

A report by Harvard University on ‘Strategies in the Islamic Funds Industry’ notes that the key elements in selecting a jurisdiction for Islamic funds include:

-

The overall reputation of the jurisdiction.

-

The degree of proven reliability and flexibility of local company, partnership, and other commercial laws.

-

The quality and level of fees of local professionals (lawyers, auditors, and others) who will be associated to form and maintain the fund.

-

The quality of the local infrastructure of the jurisdiction (including availability of reliable telephone and telefax service, e-mail, convenient air travel, and the like).

-

Presence in the jurisdiction of substantial and reliable banks.

-

The extent of local taxes and/or other governmental fees that will be applicable to a fund organized in the jurisdiction.

-

The nature and extent of local regulation of investment funds.

-

The extent to which corporate and other decision-making actions of a fund must physically take place within the offshore jurisdiction.

-

Whether there is a local stock exchange (assuming there is a potential for trading the shares or units of the fund in the public markets).

Long-standing tradition

The Cayman Islands is the most recognized offshore financial center for fund establishment, and has capitalized on this to also become popular for Islamic funds. It offers a reliable legal system, top class professional services, a well-regulated anti-money laundering culture, mechanisms to ensure speed of establishment and flexibility in fund structures and products. In addition, since 2007 funds have been allowed to submit financial statements and notifications in Arabic. Last year Ernst & Young estimated that the Cayman Islands had a total of US$4.6 billion Islamic assets under management and around 57 Islamic funds. The Cayman Islands Monetary Authority (CIMA) is the regulatory body for the financial services sector, and all registered funds in the Cayman Islands are governed by the Mutual Funds Law which covers companies, unit trusts and partnerships that issue equity interests. The regulation and licensing for Islamic funds are similar as for conventional funds, and for 20 years (for a company) or 50 years (for a trust) funds in the Cayman Islands are free from any tax on profit, incom, capital gains or appreciation. In addition, the licensing fee for funds in the Cayman Islands is a low US$3,000 per year whil the process of incorporating and registering a fund takes around three to five weeks.

The ease of setting up a fund and the cost of licensing are vital aspects when considering a jurisdiction for an offshore fund. Chris Buchan of Emerging Asset Management and Fawaz Elmalki of leading law firm Conyers Dill & Pearman note in a recent report the advantages of Bermuda as one of the leading offshore jurisdictions for investment funds. The regulatory environment is well developed, based on the 2006 Investment Funds Act, and Bermuda has no legal or regulatory impediments to Islamic investment funds. “The Bermuda government has promoted the development of Islamic finance in Bermuda and there has been steady growth in the development of Shariah compliant private equity funds, infrastructure funds and alternative investment funds… in addition to the traditional real estate funds,” according to Buchan and Fawaz. “Shariah compliant funds can be established in the same manner as conventional investment funds. The Shariah element essentially operates as an extra set of rules layered on top of the existing regulations that are aimed at a specific group of investors.”

Last year the Bermuda Monetary Authority issued a set of Guidance Notes, specifically for open-ended funds such as mutual and hdge funds, which enabled the establishment of Shariah compliant investment funds in Bermuda. The notes cover issues such as the appointment of a Shariah Supervisory Board, disclosure in a fund’s offering document (such as risk factors and conflict of interest disclosure) and elements of a fund’s constitutional documents (such as investment restrictions).

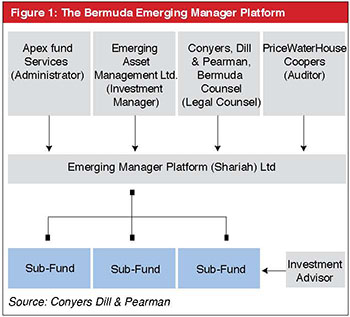

Due to the growing number of Islamic fund managers from the Middle East and Asia looking towards Bermuda, Emerging Asset Management, a local investment manager, together with Conyers Dill & Pearman set up a cost-effective platform named the Emerging Manager Platform (see Figure 1).

This Shariah compliant structure was established in 2012 as an open-ended fund and a segregated accounts company regulated by the Bermuda Monetary Authority.

“A segregated accounts company provides a legal structure for investment funds that allows the assets and liabilities of each segregated account, which can be set up as a separate sub-fund, to be legally segregated or “ring-fenced” from those of the other sub-funds on the platform and from the fund’s general account,” explain Buchan and Elmalki. “Each sub-fund may invest in the same or separate asset classes but it operates independently of the other sub-funds. The manager of each sub-fund is able to establish its own track record. This is important as a successful track record can provide the manager of the sub-fund with the credibility to subsequently launch its own independent fund.

“The Emerging Manager Platform offers all the benefits of a regulated fund and a quick, flexible and cost-effective way for managers with investment objectives and strategies that meet Shariah requirements to launch their funds in a recognised offshore jurisdiction without incurring the high costs and commitment of management time and resources required for the establishment of a stand-alone fund.”

Europe edges in

However despite the continued dominance of traditional Caribbean players, new entrants are edging in to the market as their expertise grows and awareness of Islamic finance in new territories such as Europe increases.

In 2012 two leading Islamic asset managers, both from Saudi Arabia, established funds in Europe. NCB Capital launched its Shariah compliant UCITS platform in Ireland, while SEDCO Capital established an Islamic funds platform in Luxembourg which is currently managing assets of US$1 billion which it hopes to increase to US$1.6 billion by the end of the year. Launched in March 2013, the Sedco Shariah compliant platform is a Luxembourg Sicav marketed to the high net worth segment with a choice of seven investment funds and hopes of increasing to 15 by the end of the year.

The firms are following an increasing number of Islamic asset managers with successful track records that are venturing out from their domestic markets and looking for products in well-established jurisdictions that provide them with the required global reach to maintain the success of their funds. This is a key element of offshore funds that is attractive to Islamic investors, and Europe is becoming increasingly important in this sector as offshore centers enable investors to access regions and markets that are not available through usual onshore channels as they have failed yet to pass specific Islamic finance legislation.

However some prominent European domiciles including Luxembourg and Ireland have been extremel successful in attracting Islamic funds. In Ireland the tax authorities have issued guidance notes regarding the treatment of Islamic funds, while in December 2012 Luxembourg, the leading fund domicile in Europe and one of the leading domiciles for Islamic funds globally, saw the launch of the Association of the Luxembourg Fund Industry (ALFI) which issued a collection of best practices for the establishment and servicing Islamic funds.

As Islamic asset managers seek to expand internationally, established products such as the Undertaking for Collective Investments in Transferable Securities (UCITS) in Europe could help them to reach new markets which have a long-standing reputation of being well regulated and providing a high level of investor protection.

Last year over 24 Islamic funds were domiciled in Ireland with an estimated AUM of almost half a billion US dollars. Funds are classified into UCITS and non-UCITS, with UCITS funds governed under EU legislation while non-UCITS funds are regulated under local Irish fund regulations and are thus able to target retail as well as institutional investors Funds domiciled in Ireland offer highly attractive features such as tax avoidance for non-resident invstors, while the annual license fee is a low US$1,900 per fund including up to five sub-funds. Another key attraction is a highly expedited timeline of just 24 hours.

In comparison Luxembourg is another highly competitive tax-efficient jurisdiction and fund vehicles here are also exempt from taxation. An annual license fee is around EUR2,650 (US$3,542) for a single fund under the 2002 Investment Funds Law. Under the SIF Law of 2007 this falls to EUR1,500 (US$2,005) with a timeline of around six weeks.

New players

Despite the competition, the Islamic finance industry is expanding at such a rate that new jurisdictions are rapidly emerging to attempt to attract new funds. The Maltese government has expressed a specific interest in promoting the launch of Islamic funds, and recently issued a Guidance Note offering support for the establishment of Shariah compliant funds. Islamic funds fall under the remit of Collective Investment Schemes in Malta, and are thus tax-exempt, while the annual fee for professional investor funds and retail investor funds is EUR1,500 and slightly more expensive at EUR1,630 (US$2,179) respectively. However, the jurisdiction has a timeline issue which is inhibiting fund establishment. While professional investor funds take just three to seven days to set up, retail funds can take between two and four months.

Mauritius is another domicile that has attempted to attract offshore Islamic funds, but is struggling to compete with more established jurisdicitons. Some funds are subject to around 3% tax, while annual license fees can reach EUR10,000 (US$13,367) and the registration process can take up to six weeks.

China as a new hub

In fact, the biggest source of potential for Islamic finance remains China, which is opening up as a market since the introduction of Sukuk legislation in Hong Kong this summer which it is hoped will crack open the mainland market. Malaysia, which remains the central hub for Islamic finance in Asia and (arguably) worldwide, stands to gain massively from increased trade with China, as renminbi trades will lower costs of business and attract further Chinese business.

As Asia grows in dominance, new jursidictions will also spring up as investor priorities change. No matter how competitive the attractions, eventually Middle East and Asian investors will follow the money and look to offshore centers that offer access to the biggest and best in new and up-and-coming funds. With the renminbi advancing 30% against the US dollar over the last five years, China looks to be not only the most attractive example for offshore funds, but with an appreciating and stable currency and with low volatilty meaning lower hedging costs, it could be the new castle in the sky for the Islamic funds industry.