A capital market is typically a place where capital is traded between those having surplus capital and those requiring funds for their investment needs. Modern capital markets, particularly in a capitalist, monetized economy have, over a century or so, developed a very efficient system in order to facilitate the following demands:

-

Those with surplus capital would have the opportunity to select the best forms of investments not only in terms of yields or returns but also in terms of a good mix of short, medium and long-term investments to spread their risks;

-

Those who have the opportunities and expertise to innovate and manage investment concerns but lack the funds to finance their activities can get access to surplus funds from others;

-

There are also those who need to vary their investment mix from time to time and wish to do so with ease and rapidity at very little cost;

-

There are obvious needs to develop a mechanism that will ensure the generation of investment and financing activities which are operational, cost-effective and generally fair to all parties concerned;

The growing awareness of, and demand for, investing in accordance to Islamic principles on a global scale has created a flourishing Islamic capital market, a trend enhanced by the increasing wealth in the hands of Muslims worldwide who are actively involved in corporate and business activities.

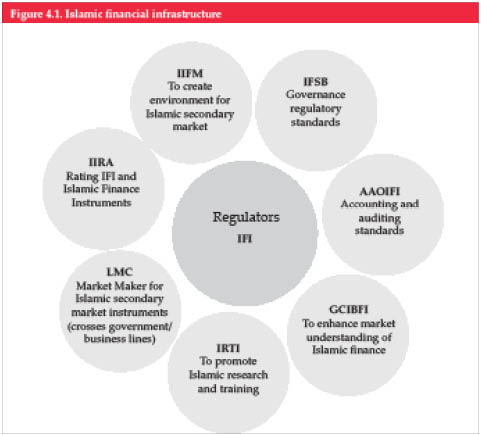

Indeed, the pace of development in the Islamic financial market has gathered momentum with the formation and growth of various international Islamic organizations to provide the appropriate infrastructure, see Figure 4.1.

These organizations include:

-

The Accounting and Auditing Organisation for Islamic Financial Institutions (AAOIFI), based in Bahrain.

-

The Islamic Financial Services Board (IFSB), based in Malaysia.

-

The International Islamic Financial Market (IIFM), based in Bahrain.

Today, the Islamic capital market operates in parallel to the conventional capital market and provides investors with an investment philosophy based on religion. It is rapidly gaining worldwide acceptance. It should be stressed that the fact that the Islamic capital market does not prohibit participation from non-Muslims creates unlimited upside to the depth and breadth of this market.

What are Islamic capital markets?

The differences between Western conventional finance and Islamic finance can be as stark as the two cultures. The respective cultures have, quite naturally, developed investment strategies reflective of their different regions.

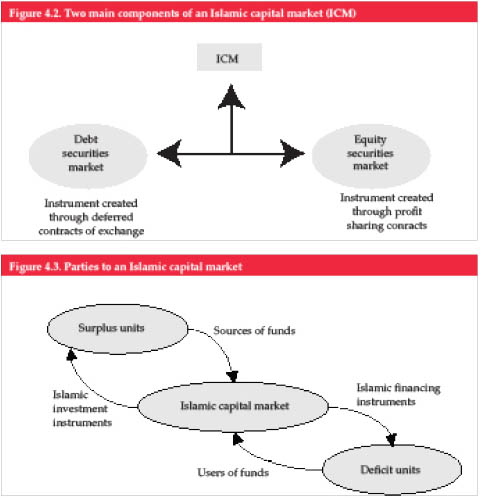

While Western investments often take on high risk and are structured to generate maximum returns, Islamic investments are based on Shariah law, which forbids the payment and receipt of interest and requires risks and profits to be shared amongst investors. Figure 4.2 illustrates the two main components of an Islamic capital market.

The role of capital markets in promoting an efficient financial system cannot be over-emphasized. Given that a developed financial system can make positive contributions to economic development, the existence of vibrant capital markets becomes a necessity for any economy. As discussed in Chapter 3, capital markets facilitate long-term financing for businesses and entrepreneurs by attracting savings from a large pool of investors. These markets provide long-term capital to entrepreneurs through a series of short-term securities with investors who may enter and exit the market at will.

An efficient capital market is expected to perform the following functions:

-

To provide a resource mobilization mechanism leading to an efficient allocation of financial resources in the economy;

-

To provide liquidity in the market at the cheapest price, i.e. the lowest transaction cost or low bid-ask spread on the securities being traded in the market;

-

To ensure transparency in the pricing of securities by determining the risk premia, reflecting the riskiness of the security;

-

To provide opportunities for constructing well-diversified portfolios and to reduce the level of risk through diversification across geographic regions and across time.

Capital markets consist of primary and secondary markets. Whereas primary markets are important for raising new capital and depend on the supply of funds, secondary markets make a significant contribution by facilitating the trading of existing securities. In some ways, secondary markets play an equally critical role by ensuring liquidity and fair pricing in the market and by giving valuable signals about the security. In other words, secondary markets not only provide liquidity and low transaction costs, they also determine the prices of the securities and their associated risk on a continuous basis, incorporating relevant new information as it arrives.

Just as capital markets play a critical role in the conventional financial system, their role in the Islamic financial system is also equally important. Whereas conventional capital markets have an established and long-running track record, Islamic capital markets are at an early stage of their development.

Conventional capital markets have two main streams: the securities markets for debt trading and the stock markets for equity trading. Raising capital through conventional debt is not possible in the Islamic system due to the prohibition of interest. Although borrowing and lending on the basis of debt is a common practice in modern conventional markets, Muslims cannot participate in conventional debt markets.

It should be stressed that the concept of stock markets is most certainly in consonance with the Shariah principles of profit-and-loss sharing. However not every business listed on the stock market is fully compliant with the Shariah. These issues pose challenges for the development of Islamic capital markets.

An Islamic capital market refers to the market where the activities are carried out in ways that do not conflict with the conscience of Muslims and the religion of Islam. In other words, the Islamic capital market represents an assertion of religious law in capital market transactions where the market should be free from the involvement of prohibited activities by Islam, as well as free from elements such as usury (Riba), gambling (Maisir) and ambiguity (Gharar). Figure 4.3 illustrates the parties to an Islamic capital market.

Functions of an Islamic capital market

An Islamic capital market should ideally perform all the above listed functions of conventional capital markets but with the added Islamic concerns of justice and equitable distribution of benefits. The Quran and the Hadith have given clear guidance on moral rules and obligations, prohibition of interest, and the prohibition of obtaining others’ property by wrongful means. Based on these and other guidelines, an Islamic capital market should function without interest and also without some of the other issues which, in the eyes of Muslims, adversely affect conventional markets viz Gharar etc.

Another aspect of Islam is that it prescribes the compulsory financial obligation of Zakat. The Quran prescribed that the purpose of Zakat is to ensure that the wealth does not circulate only among your rich folk’ (Al-Hashar 59:7). In this sense, if the capital market is not growing to allow for the overall increase in wealth and economic growth or if the growth results in the concentration of wealth to few groups of individuals, this indicates, in the eyes of Muslims, that there exists some weaknesses in the system and corrective measures need to be implemented by the appropriate authorities. This is also an area where capital markets fit within Islam.

As mentioned in Chapter 3 in the conventional financial system, an ideal effective and efficient regulatory structure is said to promote financial markets that are:

-

Liquid and efficient, where there exists a free flow of capital and where it is allocated efficiently given the underlying risks and expected returns;

-

Transparent and fair where information must be reliable and relevant and must flow in a timely and fair-handed manner to all market participants; and

-

Ethical and sound where market participants should act with integrity and in accordance with principles of unimpeachable conduct as they make capital transactions and other related activities.

The success of regulators is seen in terms of the extent to which they can build investor confidence in the integrity and fairness of transactions in capital market and the extent to which they are able to develop the markets in the direction of better transparency, greater competition and hence greater efficiency.

Objectives of an Islamic capital market

In principle, the objectives of an Islamic capital market are based on the Shariah which in essence should be treated as the necessary framework vehicle to transfer funds from surplus to deficit units. This is to ensure the equitable allocation of capital to sectors which would yield the best returns to the owners of capital and hence contribute towards the overall growth and expansion of the economy. The objective of the Islamic capital market is also to ensure that a means of attracting surplus funds for worthwhile investments exists in accordance with the owners’ preferences in terms of the extent of risk involvement, rate of return as well as the period of investment preferred. Without a capital market, the fund owners would not find sufficient opportunities to invest for the short-term. Most investments have gestation lags and are long-term in character. Emergency needs may arise from time to time which cannot be easily met.

Subsequently, Kettell taught workshops on Islamic banking and finance at a range of financial institutions including the World Bank, African Development Bank, National Commercial Bank (Saudi Arabia), Global Investment House (Kuwait), Noor Islamic Bank (UAE), the UK Treasury, the Central Bank of Iran and the Central Bank of Syria

Kettel is the most published book author on the subject in the world. He is the author of 11 books on Islamic banking and finance

Contact details

www.gulfSukuktraingcourses.com

[email protected]

mobile : +971 (0) 566399300

Islamic Capital Markets

Author: Brian Kettell

ISBN 9780955835117

Price US$125, including post and package