Despite the growing enthusiasm for Islamic finance, trade exchanges are still relatively underdeveloped in the member countries of the OIC. The major impediment is related to supply side constraints for developing a diversified economy. As a result, many OIC member countries still rely on exports of commodities and raw materials, hence, trade exchange is prone to swings based on the commodity market. ENG HANI SALEM SONBOL reviews the trade finance space.

Similar to trade exchange, the Islamic finance industry is relatively dependent on commodities, particularly oil, and their prices for resource mobilization. During high oil prices, OIC member countries were able to accumulate funds, which as a result boosted the growth of the Islamic finance industry. The first Islamic banks were established during the oil hike of the 1970s and the industry witnessed immense growth since then; however, the weak commodity market and the instability of some countries present a gloomy outlook for the industry.

Islamic finance with a more conservative business model and risk management framework than its conventional counterpart has a greater potential to mobilize funds and channel them to the countries and companies in them, including SMEs that need the funds to grow and create jobs. OIC member countries enjoy a diverse economy, which provides an opportunity for regional integration and hence supports the existence of SMEs. At the same time, many OIC countries still suffer from underdeveloped infrastructure and production capacity to blossom their SME sector.

Review of 2016

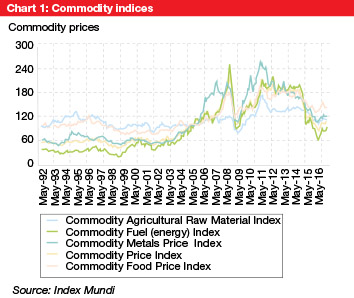

Both the Islamic finance industry and international trade witnessed many challenges in the last 12 months. As indicated in Chart 1, commodity indices dropped dramatically; this sudden drop in the prices resulted in budgetary problems especially in the oil-exporting countries and led to the slowdown of infrastructure projects. For some OIC countries, high leverage companies suffered from the currency revaluation exchange rate that resulted in losses in US dollar loans and losses due to stock revaluation because of decreased stock value.

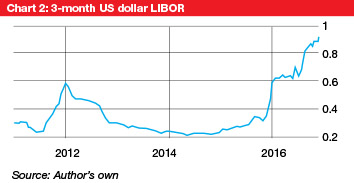

Trade finance gaps were still high particularly for the least developed countries. Low interest rates forced many financial institutions to venture into long-term finance projects to benefit from relatively higher returns. As indicated in Chart 2, the 3-month LIBOR rate was up until recently, with the incentive to venture into short-term trade finance very limited.

The low interest rates also had implications for SME support. The inclination of financial institutions for long-term lending decreased the working capital access of SMEs. This also negatively affected the profitability of Islamic financial institutions particularly those merely involved in short-term trade finance. In the last 12 months, interest rates started to increase and provided a more profitable working environment.

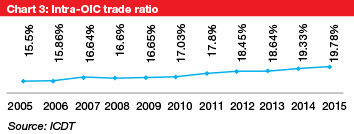

Regardless of these challenges, intra-OIC trade performed well. Net intra-OIC trade was around US$878 billion in 2015, up from US$802 billion in 2014. One main factor is the efforts exerted in OIC member countries to eliminate trade barriers related to regional integration and the WTO Trade Facilitations Agenda: port efficiency, custom modernization, standard and conformity assessment, etc. Academic work shows that the major determinants of the intra-OIC trade ratio are oil prices and the US dollar index due to the dominance of oil in intra-OIC trade and the negative correlation between the US dollar index and oil prices. High oil prices and a strong US dollar boost the ratio. The intra-OIC trade ratio is calculated by dividing the intra-OIC trade value to OIC countries’ trade with the world. As indicated in Chart 3, the ratio has performed well up until the end of 2014. A drop in oil prices starting from the last quarter of 2014 will be reflected on the ratio in upcoming years.

Preview of 2017

The recent economically introverted trend in developed countries is expected to negatively affect international trade. The Federal Reserve is expected to increase the lending rate, hence, a strong US dollar is expected to keep the pressure on commodity prices. This would decrease trade finance volumes and aggravate foreign exchange earning capabilities of commodity-exporting countries. However, increased interest rates would benefit Islamic financial institutions by a higher markup, which can contribute to profitability. On the other hand, the recent sharp movement in commodity prices, interest rates, and the US dollar value would increase credit risk of countries and companies in member countries.

For sustainable growth, the Islamic finance industry should rely less on funds mobilized from oil trade and oil financing. More focus should be on the promotion of Islamic trade finance solutions and the development of strategic commodities which are the two main pillars that will help create a grassroot development impact through providing technical assistance support and organizing sector and market-specific trade promotional activities. Supporting the development of strategic commodities in OIC member countries such as cotton, coffee, cacao and wheat will have a direct impact on alleviating poverty and empowering local communities, which are the other two strategic new millennium development goals.

In addition, focusing on providing integrated trade solution programs will also achieve complementarity among member countries. Programs that focus on developing trade linkages and creating south-south cooperation opportunities can contribute tremendously in the economic development of member countries. Such programs not only promote trade among the regions, but also create trade and investment opportunities for SMEs in member countries.

Conclusion

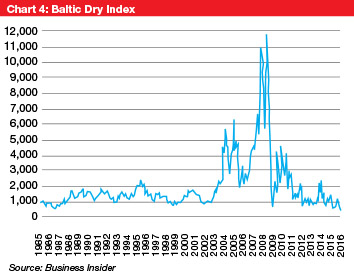

Islamic finance and OIC member countries are not immune from general economic developments in the world. In 2008, many Islamic financial institutions performed well compared to conventional financial institutions due to the Shariah prohibition of controversial financial products such as derivatives. However, Islamic financial institutions are prone to risk associated with the local economies they operate in. Chart 4 shows the Baltic Dry Index, which is below 2008 levels and requires careful reading of global trade and its possible upcoming implications for Islamic financial institutions and the trade finance industry.

Overall, the International Islamic Trade Finance Corporation believes that building strong human and institutional capacities in trade is essential to foster trade and development and will in turn improve the lives of the common people and alleviate poverty.

Eng Hani Salem Sonbol is CEO of ITFC. He can be contacted at [email protected].