A case for diversification

If you were an Islamic investor in GCC equities over the past five years, you would have lost over 45% of your investment. If you had invested in Europe over the same period, you would have lost a little over 3%. A more promising market would have been the US: had you invested there over the same period, your investment would have gained 13%. On an annual basis, this equates to a loss of 9.05% in the GCC, a loss of 0.67% in Europe and a gain of 2.6% in the US every year for the past five years. Figure 1 highlights the performance of these markets.

One can only imagine how frustrating it has been for GCC investors; no matter how well their economies performed and no matter how well the investment outlook was for the region, stock market investors lost a lot of money.

If you are an Islamic investor, you can at least be thankful that you were not invested in global financial institutions. The Dow Jones Global Financials Index lost over 55% of its value over the past five years. Looking at this picture, money market instruments and other short-term low-risk products avoiding equities all together would have been a safer bet. However, this was not the case for all markets and all regions.

Looking at the Dow Jones Islamic Market Index returns in Figure 1, you will see that investing in emerging markets over the last five years would have yielded a return of 23%, or 4.6% annually. Investing in Asia Pacific (excluding Japan) would have yielded a return of 31%, or 6.2% annually. Better yet, investing in Malaysian blue-chips would have given you a total return of 67% or 13.4% on an annual basis.

There is a lot of momentum pushing up Asian equities, which is the opposite of what’s happening in the GCC markets. The stock markets in the region are much smaller than Asian exchanges and they have a lot less liquidity. In some GCC markets, daily trading volumes are less than US$20 million, which makes it difficult to get the attention of institutional money managers. At the same time, to regain investors’ confidence, these markets need to improve liquidity and attract more investors. Figure 2 shows a comparison of stock market capitalization for select Middle East and Southeast Asian markets.

As a result of the dilemma that GCC markets face, there have been little if any new developments in these markets. Trading volumes continue to be well below their peaks of 2007 and 2008, and initial public offerings (IPOs), which are a gauge of a market’s health, have been slow to return. GCC investors, who tend to favor Islamic investing, are being forced to look outside their region for better returns.

Asia currently presents better opportunities for equity investors and is attracting a lot of interest from Islamic investors. Fund managers, family offices and high net worth investors are all looking for ways to gain exposure to Asian markets. New Islamic funds sponsored by money managers in the Middle East have been set up this year to invest in Asia. Islamic fund managers, who have traditionally focused on the developed markets of Europe and the US, as well as their home markets, are now focusing on setting up funds to invest in Asia. This trend is expected to continue as long as the momentum keeps moving in Asia’s favor.

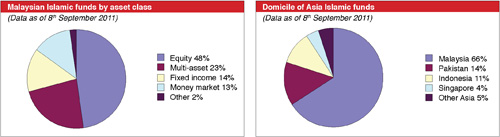

According to Morningstar, a fund research firm, one third of the 693 registered Islamic funds worldwide are domiciled in Asia (or 227 funds). Of these 227 funds, two-thirds are domiciled in Malaysia, as you can see in Figure 3. Although there are fewer new Islamic fund launches announced globally this year compared to previous years, the bulk of new fund launches outside of Asia have emerging markets or Asian investment strategies. GCC investors were not the only ones hurt during the market downturn. Money managers in the region also lost money and clients. These money managers are looking to regain their footing in the market, and a number of Asian markets present attractive opportunities. Take a closer look at Asian Islamic funds however, and it becomes clear that many are designed to cater to Asian investors in their respective countries. Far fewer of these funds were designed for the purpose of attracting international investors, with some notable exceptions.

Islamic investors are not demanding and are not looking for complex investment vehicles. There are four main asset classes where they like to invest: equities, fixed income, short-term cash products and real estate. The latter is out of favor at the moment but it still remains a primary asset class for Islamic investors. Equity products are the easiest to develop and what Islamic investors demand are a solid track record and expertise in a given region or asset class.

Islamic investors outside of Asia have traditionally favored investments in developed markets and, as a result, have established long-lasting relationships with the leading money managers in Europe and the US. Asia is new to these investors and they have yet to develop similar relationships with money managers. This presents an opportunity for Asian money managers with established track records to gain a foothold in the market.

Islamic investors globally are looking at Asia. The challenge they face is finding the right way to access this region. More importantly, they need to find the right Asian partner.