Offshore centers have long been popular with conventional fund managers due to their favorable environment for conducting business; low tax regimes; flexible regulations and strong legal standards; as well as high numbers of trained specialists.

The centers have also gone to great lengths to treat conventional and Islamic financial products similarly in terms of regulatory treatment.

The conducive environment for Islamic finance has now led to many other offshore centers following suit: including Bermuda, Mauritius, Dubai and Singapore.

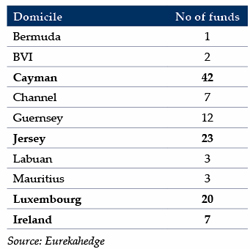

A quick check with Eurekahedge reveals that over 10% of the 876 Islamic funds globally are now registered in these offshore centers. As seen in the table above, the Cayman Islands are the most popular domicile for Islamic fund managers with 42 funds, while trailing behind in second place is Jersey with 23.

However, the global financial crisis in 2008 caused many investors to become more risk averse and hence raised the bar for greater transparency. Although the main attraction of offshore centers are their tax incentives, conventional players feel that some of these offshore domiciles face a lack of adequate regulation and quality administration. There has since been a movement towards the re-domiciling of conventional funds onshore; particularly for alternative products moving to onshore regulated jurisdictions such as Dublin and Luxembourg.

Conventional fund managers are now launching funds that comply with the widely known Undertakings for Collective Investment in Transferable Securities (UCITS) model. What was initially designed for European regulation to facilitate sales across the European Union has opened out globally to include a range of countries in Latin America and Asia. The advantage of the UCITS model is its clear and straightforward regulatory framework. It also provides a harmonized framework for fund managers relating to investor protection, transparency and disclosure requirements.

UCITS IV, adopted on the 22nd June 2009, introduces a more defined and prescriptive governance and risk management regime that compels fund managers to identify, monitor and manage both investment exposure risks arising from the instruments and strategies used in addition to the operational risks of those instruments and strategies. With such measures in place, investors benefit from high levels of investor protection and transparency.

Currently there are seven Islamic funds registered in Ireland and 20 funds domiciled in Luxembourg by a majority of European asset and fund management companies. In its bid to gain international recognition from investors, CIMB-Principal Islamic launched its funds platform establishment in Ireland in January, making it Malaysia’s first asset manager to establish an Islamic funds platform in that country. South Africa’s Oasis Group and Saudi Arabia’s

Altawfeek Financial Group have similarly launched funds in Ireland and Luxembourg respectively.

With the growing demand for transparency from investors and the need for international recognition from fund managers, the probability of Islamic funds being re-domiciled to onshore centers such as Ireland and Luxembourg is increasing. Unless offshore centers are able to formulate a similar quality of services and protection to investors, they stand to lose out.