The mechanics of Sukuk investment are a mysterious and complicated subject for many investors. From the Sukuk structure and the pricing methodology, to its risks and trading strategy, we often leave it to the experts to handle. However with its position as an essential asset class in the mandate of Shariah funds, understanding Sukuk structure is important for all participants. MAYA PUSPA ABDUL RAHMAN, PROF DR MOHD AZMI OMAR, DR SALINA H KASSIM and DR SUTAN EMIR HIDAYAT attempt to unravel the management of a Sukuk portfolio and how investor behavior can be assessed based on the variation of the Sukuk spreads .

Technically, Sukuk that are traded in the secondary market are quoted based on the spreads to a particular risk-free security, such as government investment issues (GII). In the conventional bond market, these spreads are known as credit spreads. The credit spreads are the main focus of investors in corporate bonds. Similarly, the Sukuk spreads indicate the compensation to risk, referred to as the risk premium.

The risk premium is the factor that makes investors willing to invest in Sukuk despite the risks that they may encounter. Even though Sukuk are structured based on the different kinds of contracts, which can be sale-based, leased-based, partnership-based or agency-based, the associated risks to Sukuk is mainly reflected in the spreads, which is comparable with other Sukuk that possess similar rating, duration and outlook for trading purposes.

For example, a fund manager observes that the 10-year ‘AAA’ Idaman Sukuk is trading at a spread of 108bps above the 10-year GII. If another corporate Sukuk with similar credit rating, duration and outlook were trading at a 115bps on a relative value basis, the second Sukuk would be a better buy. Why? This is because with the same risk, the investor could get a higher compensation or premium (115bps vs 108bps) by investing into the second Sukuk. This is one of the strategies carried out by the fund manager in an active Sukuk portfolio management.

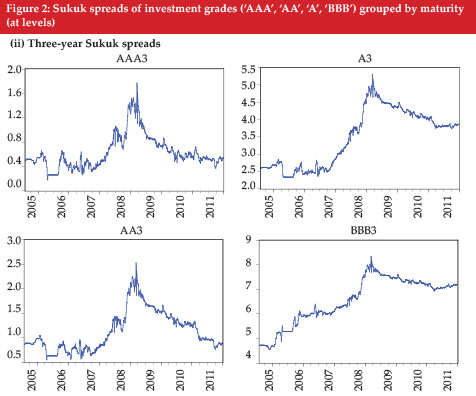

Now, let us assess on the investor behavior by examining the pattern of Sukuk spreads from 2005-11. The higher investment grade bonds (‘AAA’, ‘AA’) for both short-term (three years) and long-term (10 years) Sukuk spreads appeared to have a stable trend until they steeped upward in the middle of 2008, as shown in Figure 1/Figure 2.

As for the lower investment grade (‘A’, ‘BBB’), the Sukuk spreads of both the short and long-term demonstrated an upward trend with the spike of the spreads also observed within 2008-09. As the spreads represent the risk premium to investors for holding corporate Sukuk (against the risk-free government Sukuk), the sharp increase suggests that the risk premium for holding such Sukuk had increased significantly, especially during the financial mayhem in 2007-08. Practically, the trends observed in the charts above may be explained by the shift of investment preference by the Sukuk investors.

As corporations struggled with declining revenue and cash flows during crisis, profits payable to the Sukukholders may also be interrupted. Hence, as investors opt for a much safer instruments like government Sukuk, the higher demand is translated to a lower yield of government Sukuk causing the spreads (against the yield of similar maturity corporate Sukuk) to increase further. For example, on the 1st January 2007, the yield of ‘AAA’ 10-year corporate Sukuk stood at 4.55% whilst GII of similar maturity yields stood at 3.82%, giving spreads of 73bps. Two years later on the same day in January 2009, following the shock of the global financial turmoil which had altered the US financial system and shook the economies of almost every country in the world, the yield of the similar rated Sukuk climbed up to 5.35%, while the GII, being the safe haven instrument, fell to 3.26%, causing the spreads to widen to a massive 209bps. This reflects the higher compensation demanded by the investors for holding a much riskier corporate Sukuk, during economic downturn.

Subsequently, the spike recorded in early January 2009 was also due to the plunge in the yields of Malaysian government bonds generally. In consideration of the sharp deterioration in the global economy following the global financial crisis, Bank Negara Malaysia slashed the overnight prime rate (OPR) by 75bps to 2%, larger than the anticipated decrease of 50bps. As a result, the conventional Malaysian government securities (MGS) dropped by 40bps, led by the three-year MGS (-40bps) and the 10-year MGS (-10bps) on a month-to-month basis (RAM Ratings, 2009). The sudden decrease in the MGS yields also triggered the plunge for the yields of GII, causing the Sukuk spreads to widen further.

The different trends as depicted by the spreads of the non-investment grades (‘BB’) in Figure 3 as compared to the investment grades (Figure 1/Figure2) also reflects the preference of Sukuk investors on different classes of Sukuk. In consideration that investment grades are generally much preferred than the non-investment grades, the spreads for the latter are much higher than the former. For example, the long-term spreads of a ‘BB’ 10-year paper was recorded at 148bps on the 1st August 2005, reflecting the higher risks possessed by the lower-grade Sukuk relative to the investment grade Sukuk (‘AAA’ 10-year: 120bps). A spike in the Sukuk spreads is also visible in early 2009, most probably also due to the worries on the state of the global financial crisis. It is also observed that post-crisis, the non-investment grade Sukuk spreads appeared to chart a different pattern than previously.

As such, it is obvious that the investor behavior is driven by the state of economy. During good economy, investors tend to invest more into corporate Sukuk, pushing its yield downward and tightening the spreads. Conversely, at times of crisis, investors remain sidelined on corporate Sukuk and prefer the safer government Sukuk, causing the yields to move in a different direction hence widening the spreads. In addition, with the high speculative nature of the non-investment grade Sukuk, any changes in the monetary policy driven by the changes in interest rates during the different state of the economy may cause the spreads of the non-investment grades to be deterred significantly relative to the spreads of the investment grades. This is also in line with the empirical evidence of the highly-cited work of Longstaff and Schwartz in 1995 where firms with higher default probabilities (lower grade bonds) are more susceptible to changes in interest rates.

Hence, an understanding of the risk premium reflected by the Sukuk spreads is essential to comprehend how the trading and management of Sukuk portfolio are undertaken. More importantly, the variation of Sukuk spreads, which are derived from the movement of the yields of corporate Sukuk against government Sukuk, is also able to signal trends in investor behavior during different states of the economy.

Maya Puspa Abdul Rahman is a PhD scholar at the Institute of Islamic Banking and Finance, IIUM; Professor Dr Mohd Azmi Omar is the director general, Islamic Research and Training Institute, Islamic Development Bank (IDB); Dr Salina H Kassim is an associate professor at Kulliyah Economics and Management Sciences (KENMS), IIUM and Dr Sutan Emir Hidayat is an assistant professor and academic advisor for Islamic finance at University College of Bahrain (UCB).

They can be contacted at [email protected], [email protected], [email protected] and [email protected] respectively.