Iran is a country in which all financial instruments should comply with Shariah rules and regulations. For this, it is not lawful in the capital market to trade any conventional financial instruments nor to establish any financial institution where its performance contradicts Islamic rules and regulations.

In 2015, the Iranian financial market faced new economic and political situations. Talks between Iran and powerful economies in the globe for Iran nuclear programs and a reduction of inflation through some deflationary monetary policies resulted in some changes in financing tools and the Islamic equities market.

Review of 2015

What Iranian investors witnessed in 2015 may be categorized in Table 1.

|

Table 1 |

|

|

Islamic equity market |

As indicated before, nuclear talks between Iran and six other powerful economies (ie the US, Russia, China, England, Germany and France) finished with a decision to lift many sanctions against the Iranian financial system. This affected listed companies which were mainly active in the trade business. |

|

Islamic derivatives market |

The Islamic gold coin futures market in Iran, as a result of US dollar to Iranian rial fluctuations and also global gold price changes, was facing many alternations. There was no important change in the underlying assets in Islamic futures contracts in Iran in 2015 but some new arrivals has been planned that would be described in the preview of 2016. |

|

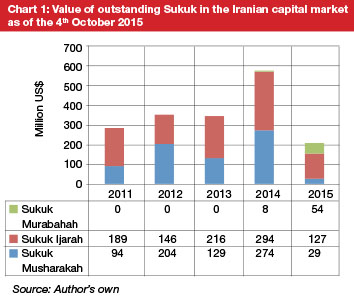

Sukuk market |

Sukuk Ijarah, Musharakah, Murabahah, Salam and Istisnah are the five types of Sukuk as issued in the Iranian capital market in 2015. The market value is shown in Chart 1. One important modification in the Sukuk market in 2015 was the new procedure for subscription which was based on investor valuation in IPOs. Previously, Sukuk in Iran was issued at a nominal value, but according to the modification, investors may pay different amounts than the nominal value. |

|

Table 2 |

|

|

Islamic equity market |

The macroeconomic condition of the country is going to be in more vibrant situations. The state is planning for more protection of investors as well as listed companies. Lifting of sanctions will also broaden Iranian financing opportunities as the current low P/E ratio seems to make the market attractive to many foreign investors. Hopefully, there would be better conditions for the development of the Islamic equity market in Iran. The Islamic gold coin futures market in Iran, as a result of US dollar to Iranian rial fluctuations and also global gold price changes, was facing many alternations. There was no important change in the underlying assets in Islamic futures contracts in Iran in 2015 but some new arrivals has been planned that would be described in the preview of 2016. |

|

Islamic derivatives market |

For derivatives, the market is planning to welcome currency futures in a Shariah compliant model. This would bring more opportunities for development in the Iranian Islamic futures market. Currently, gold coins are the main underlying assets in Islamic futures contracts. The SEO has announced its plans for the establishment of a ‘currency exchange’. While in 2015 currencies were traded traditionally by exchanges, the new scheme may structure the market in a better format. Islamic currency futures contracts are going to be launched and traded in the new exchange. |

|

Sukuk market |

For Sukuk, the SEO is planning for the development of the market in both value and volume in 2016. While the Shariah Board of SEO resolved that “Ijarah, Murabahah and Musharakah types of Sukuk may be initially issued at market price”, the SEO implemented this technique to make Iranian Sukuk more attractive to investors as they may gain more in profits. Additionally, in 2016 the SEO is going to use Sukuk Istisnah more widely as a financing tool for many contractors. While currently there are not many Sukuk Istisnah issuances in the Iranian capital market, the SEO is planning to have more in the coming year. |

|

Source: Author’s own |

|

Preview of 2016

The Securities and Exchange Organization (SEO) as the supervisory and regulatory body of the Iranian capital market is planning for developments as well as to strengthen current situations as in Table 2.

Conclusion

In the Iranian financial system, all market instruments should follow Shariah, but above all, it is the regulatory body of the market that regulates and supervises the issues within the system; in the other words, there should be a strong Shariah governance framework for supervising Islamic issues. The Iranian capital market is going to find more diversity in Islamic financial instruments and derivatives. Moreover, the lifting of sanctions may witness more investment demands in the Iranian wholly Shariah compatible market.

Majid Pireh is an Islamic finance senior expert at Iran’s Securities and Exchange Organization. He can be contacted at [email protected].