Syndicated Islamic financing and bonds have emerged as distinct asset classes in the recent times. Islamic syndication with its relatively standardized and easier structuring procedures has attracted borrowers and issuers alike, SYED SIDDIQ AHMED writes.

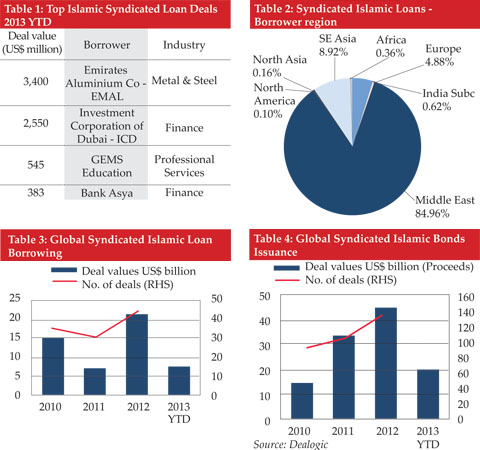

Syndication has traditionally been one of the easier and less complicated modes of funding large capital requirements. Making up 0.62% of the global market, Islamic syndication has shown its significance with increasing number of quasi, corporates and sovereign governments opting to raise financing, especially at a time when Sukuk yields seem undesirable.

Regulations

Regulations for Islamic syndication are not much different from that of its conventional counterpart. As syndication might involve different jurisdictions, and with most deals taking place in the Islamic markets, it may be prudent for bookrunners and issuers to take into account the distinction and applicability of Islamic law of contracts with the governing law of the deal. It may also be important to stress and include the ‘choice of law clause’ that is applicable to the deal.

Market developments

With the UAE leading the market, the Middle East region has accounted for US$7.2 billion worth of syndicated loans in 2013, followed by Europe with US$383 million. Saudi Arabia and Malaysia were the frontrunners in 2012 with US$11.3 billion and US$3.8 billion worth of deals respectively.

In 2013, there were as many as three deals in the transportation sector worth US$650 million, all from UAE borrowers; while Turkey’s Bank Asya borrowed US$383 million for its financing purposes with a leveraged deal. The metal and steel industry saw the highest amount of borrowing with US$3.4 billion by Emirates Aluminum Co Ltd PJSC (EMAL). Based on data by Dealogic, of the top 10 borrowers since 2007, the oil & gas and telecom industries currently lead the way, followed by finance, utility & energy and chemical companies.

Abu Dhabi Investment bank is currently the leading bookrunner for 2013 with US$224 million worth of deals, followed by Standard Chartered and Noor Islamic bank with US$64 million worth of deals each. Saudi Arabia-based Samba Capital ran the largest deal in recent years with a US$3.2 billion Islamic syndicated financing in 2010.

Opportunities

Since there is no public disclosure of deal information, borrowers and issuers might use syndication for institutions which do not want their deal information to be made public. There are also opportunities for international banks with Islamic windows. Relatively simpler structures, approvals and procedures could be seen to encourage institutions to opt for syndication.

Since Qatar, Saudi Arabia and UAE have substantial requirements in infrastructure development, syndication facilities will continue to hold good market in these jurisdictions. Oil & gas, petrochemicals and other development projects would also require deals that might throw opportunities for Islamic syndication.

Challenges

There is a need for innovative Shariah compliant structures in the Islamic syndicated finance industry. Although structures based on Murabahah and Ijarah are gaining popularity, the majority of institutions currently apply organized Tawarruq. This however does not seem to go down very well with Shariah specialists and poses a challenge in terms of approval. Experts also maintain that there is a need for a larger pool of ready investors on a global scale.

Outlook

There has been substantial growth in the Islamic syndication market in 2012. While there have been only eight deals this year worth US$7.6 billion for Islamic syndicated loans, a surge in Sukuk yields could spur institutions to opt for Islamic syndication. With sizable global infrastructure and other growth stakes running high, the Islamic syndication market is expected to gain momentum moving forward.