Sukuk continues to be a viable alternative for both Islamic and non-Islamic investors seeking to diversify their investment portfolios. With attractive relative returns to traditional fixed income assets, the volatility of this asset class has historically been less correlated with the global fixed income market. Sukuk issuers typically are from the fast-growing and most financially sound economies in the GCC and Southeast Asia, countries that are often underrepresented in many traditional bond indexes and funds. AHMAD NAJIB NAZLAN summarizes what happened in the past year and what we can look forward to in 2017 with regards to institutional investments.

Review of 2016

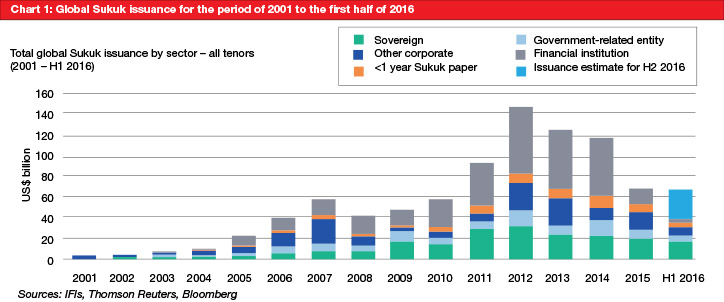

Global Sukuk issuance has been moderating since 2015 and we expect this trend to remain subdued this year and in 2017, with reference to rating agencies Moody’s Investors Service and S&P (see Chart 1). New Sukuk issuance volumes remained subdued for the first half of 2016 at US$40 billion. This has been driven by more challenging economic conditions in emerging markets and the GCC’s move to tap conventional liquidity from international investors, as quantitative easing has been driving yields to zero or even negative rates in various markets.

The year saw low global growth, as markets sought leads to possible growths in the backdrop of weakening BRIC countries with Brazil, China and Russia facing recession. GDP growth has been revised downwards continuously in 2016, which was an uninterrupted trend from 2015 (see Chart 2). The slowdown in economic growth in China has led to overcapacity in many industries including cement, steel, coal and shipbuilding. Commodity prices were also down due to weak economic growth. Europe, Japan and China continued to implement monetary easing policies to bolster growth.

In our views, the environment of lower interest rates and high asset prices may see low asset returns in the medium term; developed world equities and fixed income do not offer value, rather relative value can be found in emerging market equities and fixed income over the medium term. 2016 was also punctuated by sharp corrections and equally sharp rallies as macroeconomic data and corporate earnings disappoint. Volatile markets are often a function of low visibility and weak economic growth.

Preview of 2017

The following are what to expect in 2017:

- Developed markets and Asian economic growth are expected to be subdued but stable to moderately better. Asian exports are still declining, albeit at a slower pace.

- Monetary easing in developed markets may have reached limits, eg in the US, Europe and Japan. Meanwhile, market players are expecting 1-2 rate hikes in the US in 2017.

- Policymakers in developed markets and many parts of Asia are increasing fiscal spending to complement monetary easing and support growth. Fiscal stimulus and infrastructure spending will likely pose an upside risk to earnings outlook and government bond supply.

- Binary outcomes could possibly lead to increased volatility, eg the US presidential election and the US Fed hikes. 2017 will see Malaysian elections, the UK to invoke Article 50 in the first quarter of 2017, French elections in April and German elections in September.

- The recent decline in the US bond market coupled with negative yields in Europe could be good news for the Sukuk market, which could see funds flowing in as investors shift their gaze away from developed markets and into this asset class.

- Sharp movement is expected in certain fixed income markets due to the recent increased market volatility, eg Malaysian government securities may provide attractive entry points for investors.

Conclusion

Market volatility has increased in recent years. From a portfolio allocation standpoint, heightened volatility across asset classes usually coincides with macro turning points. All would agree that a certain level of volatility will continue in 2017 and beyond. Sukuk are increasingly featuring as an effective diversification tool in a volatile market, while showing evidence of low correlation with developed and emerging market US dollar-denominated asset classes.

Ahmad Najib Nazlan is CEO of Maybank Islamic Asset Management. He can be contacted at [email protected].