Are Islamic indices an integral component of the Islamic finance industry? ALKA BANERJEE provides a detailed explanation and comparison.

Islamic finance has grown in stature and importance over the last three decades. It is somewhat interesting that coincidently, the importance of indexing, or passive investing, has also grown exponentially during the same time period. While indices have been around for a long time, their commercial use has exploded in the last twenty years.

At its core, an index seeks to measure the returns of a clearly defined market space – for example, geographically or by sector or style. The use of an index has further evolved as a tool to facilitate investments, via ETFs, mutual funds, OTC products, and derivatives. Naturally, as Islamic finance has grown, the necessity and existence of Islamic indices has become more important.

Long-only equity market investments have been perennial favorites of Shariah compliant investors. Hence, equity market Islamic indices were the first requirement of the day. If Islamic investments are all about equitable risk sharing, then the best mechanism for risk sharing is the stock market. A key aspect of Islamic investors that should be noted is the similarity between their requirements and that of conventional investors.

The process of Shariah screening is in itself, quite simple. Stocks that pertain to ‘haram’ activities like pork, alcohol, gambling, financials (except Islamic financial institutions), advertising and media (newspapers are allowed and sub-industries are analyzed individually), pornography, tobacco, the trading of gold and silver (as cash on a deferred basis) and cloning are removed from the universe.

In Table 1, the three headline Shariah indices currently provided by S&P Indices: the S&P Pan Arab Shariah, the S&P 500 Shariah and the S&P Global BMI Shariah, are compared to the underlying indices. Some common facts emerge: the typical coverage of Shariah compliant stocks ranges from a minimum of 40% to over 55% – both in terms of market capitalization and in terms of number of stocks captured. There is a clear bias towards large cap stocks for Shariah compliance, illustrating that large cap stocks tend to have less debt on their books (which is no surprise). Sector weights are largely similar in their overall allocations to underlying indices, except for the financials sector which, naturally, gets mostly removed from non-Pan Arab regions. While sectors may be over- or underweight in the Shariah compliant versions compared to the underlying indices, no major sector bias develops as a result of being in compliance with Shariah law.

Now to the major question: How do S&P Shariah indices perform when compared to the underlying conventional indices? On a three-year basis, the Shariah indices are the clear winners. The financial meltdown of 2008-2009 impacted the financial sector the most, and Islamic investors managed to avoid most of the pain associated with the fallout.

This has naturally led to significant outperformance of the Shariah indices in all the markets studied in this article – Pan Arab, US and Global. The Pan Arab Shariah Index outperformed the conventional Pan Arab indices by more than 7% over the last three years. The S&P 500 Shariah outperformed the underlying index by more than 4% and the Global BMI Shariah benchmark beat its underlying conventional index by more than 3% during the last three years.

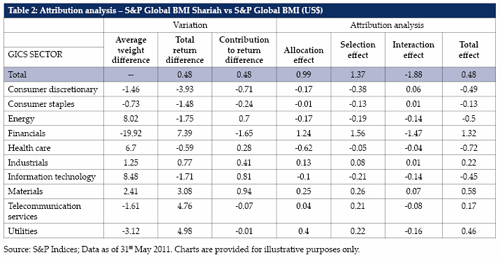

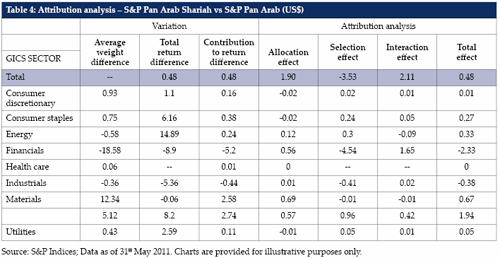

Closer analysis continues to support the theory of sector play at work. Attribution analysis (as illustrated in Tables 2 – 4) on the same three indices for the 2010 year show that for the S&P BMI Global Shariah Index, the sectors with the highest positive weight differential were information technology (8.48% overweight), energy (8.02% overweight), and healthcare (6.7% overweight) – all of which contributed more towards positive returns for the index.

The maximum contribution to returns came from the materials sector which is 2.41% overweight in the Shariah index, and has had stellar returns for the year (+28.25%). While not shown in the attached tables, while the Shariah index suffered with the financials uptick following the market crisis, it was more than compensated by the strength of the materials, energy, information technology and healthcare sectors which were all overweight in the Shariah index.

A similar story emerges from the S&P 500 Shariah. Information technology, materials, energy and healthcare were the most overweighted sectors in the S&P 500 Shariah. The outperformance of 1.68% of this index, in 2010 – over its conventional counterpart – came from the positive returns produced by these sectors, overshadowing the strength of the financials sector, where the index was severely deficient.

Islamic indexing has extended its frontiers into the world of Sukuk (i.e. bonds), with several Sukuk indices jumping into the fray. However, adoption and usage has been hobbled by the lack of secondary markets, or liquidity for Sukuks, in general. Another important area is commodities. With almost all of the Middle East heavily dependent on oil, a commodity index which is Shariah compliant would seem a natural. However, most standard commodity indices are based on the futures price of their constituents, and spot pricing is not considered a liquid option.

Recently, some attempts have been made to create a limited number of Shariah compliant physical commodity indices, using ‘Salaam’ contracts — how successful these indices will be remains to be seen.

Recently, the boundaries of passive investing have been pushed further out, with more and more of the so-called ‘active’ strategies finding a home under the banner of indexing. The idea is that if a strategy can be quantified and solidified under a series of fixed rules, which apply themselves on a regular frequency, then that concept could qualify to be called an index.

Strategy indices have gained a lot of traction, in recent years, with simpler concepts ranging from thematics — where theme-based sector-investing is measured — to far more complex concepts such as Risk Control Indices, where the index allows the investor to move money to cash, when an equity portfolio crosses an acceptable limit of volatility.

While many of these ideas can apply themselves naturally, and seamlessly, to the Shariah space, several others cannot, due to the lack of acceptable instruments which can be utilized. A well-developed financial system is essential for the overall economic growth of a region and its people.

Alka Banerjee is the vice-president of global equities and strategy indicies at Standard & Poor’s. She can be contacted at

[email protected]

.