Furthermore, Shariah law prohibits Muslims from dealing in interest – both the paying and receipt thereof. For investors that want to adhere to Shariah, the universe of available investments therefore reduces substantially as a consequence and in particular sectors like banking, beverages, media and entertainment become no-go areas for investment.

Furthermore, for companies with Shariah compliant business activities, debt and cash balance levels need to be closely managed to avoid the payment or receipt of excessive amounts of interest. As a result of the perceived onerous rules and limitations placed on Shariah investors, the conventionally-held view is that Shariah investing will result in lower returns compared to conventional investing.

At Kagiso Asset Management, we do not share this conventional view. We launched a Shariah compliant equity unit trust in July 2009 because we are of the view that, even with the perceived limitations placed on us, we would be able to outperform our traditional competitors in the unit trust industry.

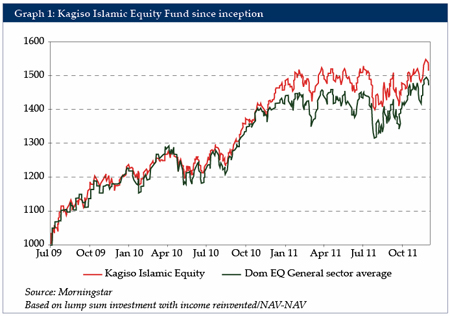

We benchmark our performance relative to the mean performance of our peers with a view to outperforming this benchmark and being amongst the top 20% of funds on a consistent basis. As can be seen from Graph 1, our Kagiso Islamic Equity Fund has outperformed the mean fund since its inception in mid-July 2009.

Longer-dated returns

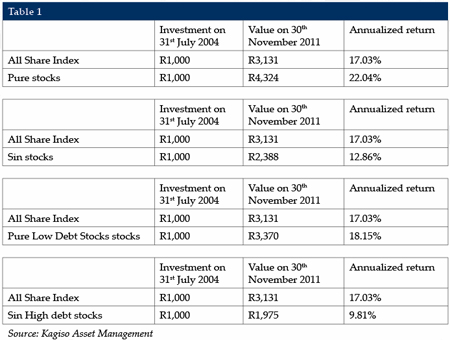

As part of our pre-launch research for the Kagiso Islamic Equity Fund, we looked at historic returns on the Johannesburg Stock Exchange (JSE) All Share Index and specifically, the returns from a Shariah compliant or ‘pure’ portfolio of listed stocks relative to the JSE All Share Index and a portfolio of non-permissible or ‘sin’ stocks.

Due to changes in the JSE’s equity classification system, we could only calculate returns from July 2004: nevertheless we had five years of data to our launch month of July 2009. We recently updated the research to incorporate the latest data to the end of November 2011, a total of 88 months.

Measuring performance

We calculated the performance of the two portfolios and the JSE All Share Index using pricing data supplied by the JSE to INet-Bridge, excluding dividends. The inclusion of dividends would have favoured the pure portfolio, as the companies in the portfolio tended to have higher dividend pay-out ratios and stronger balance sheets compared to the sin portfolio. Significantly, the measuring period included the 2008 recession, as well as the preceding bull market period. The results of the back-testing can be summarised as per Table 1.

As indicated in the table, the JSE All Share Index returned 17% over the 88-month period, translating into a portfolio value of ZAR3,131 (US$385.1) at the end of November 2011, following a ZAR1,000 investment on the 31st July 2004.

Conclusion

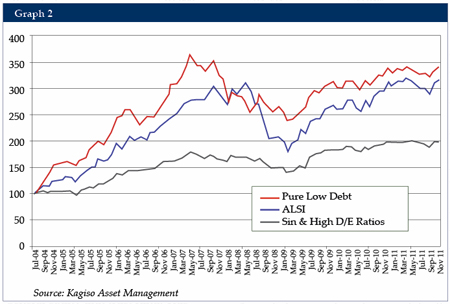

The outperformance of the pure portfolio was expected during the recession given the stable balance sheets of the underlying companies. However, the preceding bull market as well as the subsequent rapid recovery would have favored geared stocks disproportionately. Nevertheless, a pure Shariah compliant portfolio would not only have outperformed the broader market but also earned a substantial real return over the last seven years.

Abdulazeez Davids is the head of research and portfolio manager at Kagiso Asset Management. He currently manages the Kagiso Islamic Equity Fund as well as segregated equity portfolios for institutional clients. He can be contacted at

[email protected]

.