Islamic finance in Malaysia has been gaining importance in recent decades, concentrating on the area of retail products — the common products, to name a few, are deposit accounts, personal financing and home financing. For most of us, a large proportion of our income would go toward home financing.

In Malaysia, nearly all the Islamic banks adopt the widely used principle of Bai Bithaman Ajil (BBA). Other Islamic modes of home financing in the country are Bai Inah, Istisna and Musharakah Mutanaqisah (MMQ, diminishing partnership).

As the basic features of Islamic financing generally embrace the notion or application of the sales concept, there is a need to explore other innovative Islamic financial concepts such as partnership contracts and leasing. Hence, MMQ was introduced to implement the relationship of partnership in the elements of sharing and ownership.

Comparison of BBA with MMQ

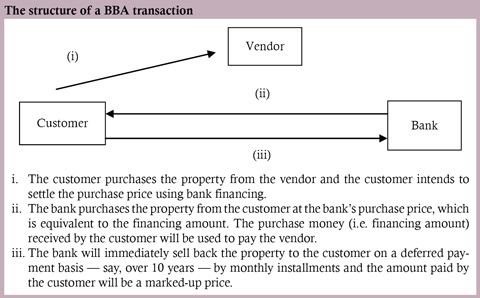

The BBA is basically a deferred payment sale contract whereby the buyer is given the benefit of a deferred payment, and the deferred price of the sale object carries an additional profit. The steps in a BBA transaction are illustrated below.

The underlying transaction of the BBA is said to be based on the Murabahah concept of a cost plus contract, whereby the sale price (with profit) of the commodity is paid in installments over a long period.

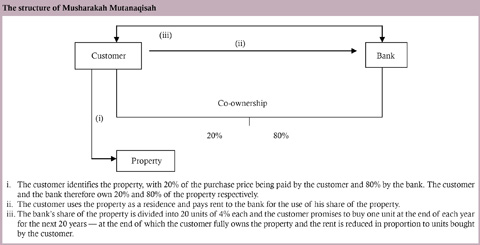

The MMQ contract, on the other hand, is based on the diminishing partnership concept. There are two portions to the contract. First, the customer enters into a partnership (Musharakah) agreement with the bank.

The customer pays, for example, 20% of the initial share to co-own the house while the bank provides the balance of 80%. The customer then gradually redeems the bank’s 80% share at an agreed portion until the house is fully owned by the customer.

Second, the bank leases its 80% to the customer under the concept of Ijarah, i.e. by charging rent. The customer agrees to pay rental to the bank for using its share of the property.

The periodic rental amounts will then be shared between the customer and the bank according to the percentage shareholding at the particular time which keeps changing as the customer redeems the bank’s share. With each payment, the bank’s share in the property will be reduced while the customer’s share increases.

The structure of the Musharakah Mutanaqisah is illustrated on the following page.

Operational structure

The BBA assists the customer in paying the cost of financing during the tenor of the facility (for example, 10 years) at a fixed rate determined by the bank. The bank buys the property from the customer (which is actually the financing amount) and sells it back to the customer, plus its profit margin.

The Shariah would require the bank, as the vendor, to hold ownership of the property and to all liabilities arising. However, the BBA documentation shows that the bank merely acts as a financier rather than a vendor.

This is evident from the acquisition of the property by the bank through the purchase agreement with the customer that does not involve the transfer of the name in the issue document of title to the property.

The buying lasts for a few seconds during the signing and, in practice, the selling back to the customer through the asset sale agreement is almost immediate.

It has been argued that this ignores the Shariah principle of “al-Ghorm bin Ghonm” (no reward without risk), “Ikhtiar” (value addition or effort) and “al-Kahraj bil Daman” (any benefit must be accompanied by liability), thereby subjecting the BBA profit to riba.

At the heart of Islamic finance is the principle of risk sharing. As such, the concept of “al-bay” (trade) is used because the profit from trading incorporates risk-taking, while the contractual profit from loan transactions (riba) is risk-free.

Many have observed that there is no risk-taking in the BBA financing and, hence, does not merit the concept of al-bay.

In a BBA financing, the customer is saddled with the burden of paying off the property even before it is completed as he has engaged in a “debt contract” with the bank at the outset, thereby leaving the welfare of the people unprotected.

The MMQ, on the other hand, ultimately culminates in ownership of the property by the customer. The bank participates as a financial partner, whether in full or in part, and an agreement is signed between the customer (partner) and the bank that stipulates each party’s share of the profits.

The bank will then lease its share of the property to the customer under Ijarah. The share will be divided into a number of equal units and the customer promises to buy the individual units periodically until all are taken up (the principle of “al-bay” under the MMQ contract).

The bank will then agree that the Ijarah rental is reduced in proportion to the units purchased.

The periodic payment by the customer in this model constitutes two parts:

a) a rental payment for the portion owned by the bank; and

b) a buyout of part of that ownership.

In contrast to the leasing model, where the ownership of the financed item remains with the lessor for the entire lease period, ownership under the MMQ contract is shared between the customer and the bank. Over a period of time, the portion of the property owned by the customer increases until he owns the entire property and no longer needs to pay rent. At this point, the contract is terminated.

The MMQ, nevertheless, has its share of operational problems.

An example is that the rental rate would be based on the market rental value, which is very much determined by location, and in time, the rental value can therefore change; in normal cases, this would increase.

It would be difficult to keep track of the rising rentals and prove cumbersome to the bank and the customer, who would have to pay a higher rental as the years pass.

Another issue is whether the above transactions can be combined into one agreement as the Shariah principle has made it clear that a combined agreement and made conditional to each other is not permissible.

There has been a proposal that the co-purchase and Ijarah can be combined into one document and the purchase of the bank’s share over time must be in a separate agreement.

However, it has been resolved that it is permissible for the contracting parties to combine the two contracts of Musharakah and Ijarah into one document as long as both were concluded separately and do not overlap.

Differences between BBA and MMQ contracts

-

The MMQ contract is seen as a joint ownership structure whereas the BBA is a debt-type financing.

-

As a financing structure, the MMQ is more flexible than the BBA as the customer can own the property earlier by redeeming faster the principal sum of the bank without the need to compute rebates, as is the case with the BBA.

-

Many may be of the opinion that the BBA is similar to a conventional loan.

-

The MMQ is accepted internationally as Shariah compliant whereas the BBA is recognized predominantly in the east, e.g. in Malaysia and so on.

-

Under the BBA, the selling price of the property by the bank does not reflect market value since the mark-up for the deferred payment is quite substantial.In the MMQ model, the value of the property always reflects market price and rental is determined by market rental values.

-

By default, partners in the Musharakah arrangement are free to leave a partnership anytime. Thus, the bank has to note this and incorporate the compensation clause applicable when a customer leaves the partnership.

-

By default, the lessee in an Ijarah arrangement will cease to pay rent once he stops deriving benefit from the use of the property.

-

By default, any decision relating to the disposal of the acquired property must be approved by both Musharakah partners.

-

The return of the BBA is based on a fixed selling price. However, under the MMQ, the bank need not be tied to a fixed profit rate throughout the financing tenor. This is because the rental rate can be revised periodically to reflect the current market situation.

-

The bank can manage the liquidity risks better as rental payments can be adjusted at the end of each subcontract period. This is not possible under the current fixed-rate BBA as the profit rate is constant throughout the tenor of the financing.

In comparison, under the BBA concept, the customer would most likely end up paying about four times the original cost. This may burden the lower-income group in particular.

The MMQ can be seen as more just as there is no interest charge or “advanced” profit involved. It is based on the concept of rental payments and redeeming the bank’s shares in the property.

Noreeta Mohd Nor is a senior associate at Azmi & Associates. She can be contacted at +603 2118 5031 or via email at

[email protected]

. Visit

www.azmilaw.com