In this issue we focus on the recent activity in the agriculture sector.

Diminishing economic growth rates mixed with a disappointing earnings season and revised profit outlooks put pressure on financial markets in October. On the credit side we have seen some strength in the US housing sector, as well as better than expected consumer sentiment data. All in all, it seems as though the latest quantitative easing programs are suffering a diminishing marginal utility.

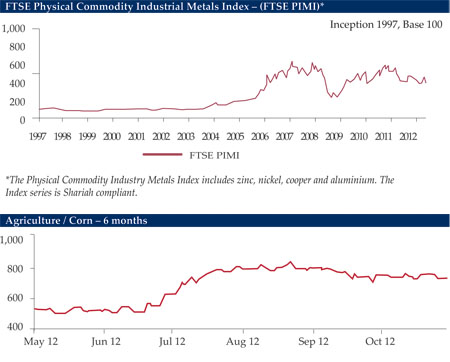

Base and precious metals were particularly hard hit with nickel, zinc and lead losing more than 10%. The sector is confronted with declining growth rates in emerging markets, diminishing global demand and to a certain degree with overcapacity and high stock levels. Aluminium stocks in Shanghai have risen to 940,000 mt, the highest level since September 2010. According to Aurubis, the largest copper producer in Europe, the intended launch of copper ETFs by J.P. Morgan and Blackrock (still to be approved by US regulators) may cause the two institutions to buy 180,000 t of copper for physical deposit.

Apart from that we have seen a weak energy sector with WTI- and Brent-prices falling by 7% and 3% to US$85.5 and US$108.5 per barrel respectively – thereby pushing the spread between the two contracts again to record highs of US$24/barrel. The prevailing price levels indicate lower geopolitical risk premiums and sufficient stock levels in the short and medium-term.

After the sharp price increases during the summer months in the course of the worst US drought in 50 years, grains are going through a period of price consolidation with slight negative tendencies as the late harvest turned out to be better than initially expected. Eighty percent of the US corn and soya harvests are already brought in and due to the lack of storage facilities farmers sell their crop directly from the fields – thereby putting pressure on futures markets. However, with price increases of 30% on average this year, the agricultural complex remains top ranked for 2012.

Merit Commodity Partners. For more information or a daily update, contact

[email protected]

or

[email protected]