In tandem with the buoyant property market in the Middle East and GCC region, transactions involving Islamic finance instruments in Singapore have seen upward momentum of late. Property-based assets that are Shariah compliant include residential properties, apartments (residential to fully serviced apartments), office lots, industrial or business parks and retail space. However, a hotel which is also a place for entertainment is not acceptable under Shariah laws. Further studies of tenancies often must be undertaken in order to determine their acceptability from the Shariah perspective. Any source of rental income from non-Shariah compliant activities must be less than one-third of the total rental income for the asset.

This article outlines the huge potential for Islamic real estate transactions, beginning by setting out two case studies of recent Islamic real estate transactions in Singapore.

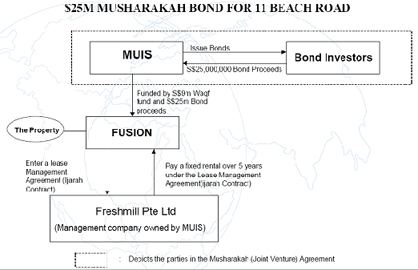

Musharakah bond for 11 Beach Road

The 20 properties concerned in this transaction were generally in a dilapidated condition and in non-prime locations. They were Waqf properties, or held in trust by the Islamic Council, Majlis Ugama Islam Singapura (MUIS). The redevelopment of these properties was not feasible as the potential rental income would have been unattractive.

Given that the Fatwa Committee chaired by the Mufti had allowed the migration of low-yielding Waqf to higher yielding Waqf, MUIS made a decision to divest the 20 Waqf properties based on a 199-year leasehold tenure. In place of this, MUIS bought a six-storey office building on 11 Beach Road at a cost of S$31.5 million (US$20.78 million), equivalent to S$919 (US$606.41 million) per square foot. A single purpose company was formed to purchase and own the new building. An additional S$2.5 million (US$1.64 million) was spent on refurbishment in order to give the building a more upmarket look, as it was in a prime location. This also enabled an increase in the rentable area and the offering of better facilities.

MUIS required financing for the purchase of 11 Beach Road while the sales of the old Waqf properties were in progress. Conventional instruments were explored. Ultimately, a decision was made to use an Islamic financing transaction. This Musharakah bond became the first Islamic bond to be issued in Singapore. Musharakah was acceptable to MUIS and was also in line with guidelines imposed by Monetary Authority of Singapore.

There were two principles for this funding structure: Musharakah (partnership) and Ijarah (leasing). MUIS entered into a Musharakah agreement with the bond investors to purchase 11 Beach Road and to share the profits and risks. MUIS contributed S$9 million (US$5.93 million) while the bond investors’ share was S$25 million (US$16.49 million). The capital contribution and profit-sharing ratios were 26.5% for MUIS and 73.5% to the investors.

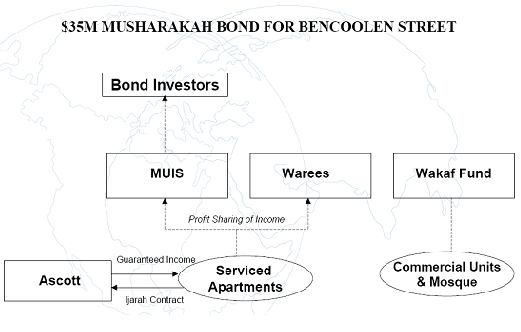

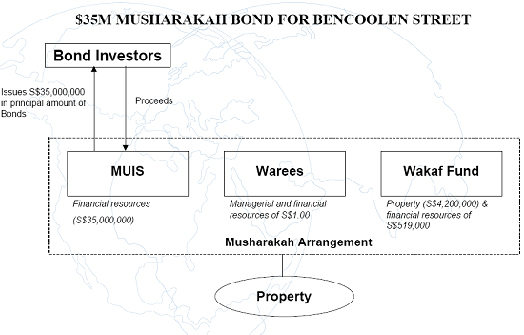

Bencoolen Street – Musharakah bond strucutre

Another property where an Islamic finance structure was involved was an old mosque on Bencoolen Street. The mosque required redevelopment to convert it into a mixed-use complex comprising a modern mosque, a three-storey commercial building and 12 storeys comprising 84 full-facility apartment units.

Here, three parties participated in a Musharakah agreement valued at S$35 million (US$23.09 million). They were MUIS, the Wakaf fund and Warees Investments, a wholly-owned subsidiary of MUIS. The corresponding completed value of the various components to this development determined the share contribution for each party. On completion, the whole complex was valued at S$71.06 million (US$46.89 million). This comprised the mosque and three-storey commercial building owned by Wakaf fund at S$8.44 million (US$5.56 million) (11.9%) and the 12-storey apartment owned by MUIS and managed by Warees at S$62.62 million (US$41.32 million) (88.1%).

The capital contribution by MUIS was S$35 million (US$23.09 million) (88.1%) and by Wakaf fund another S$4.7 million (US$3.1 million) (11.9%) – S$4.2 million (US$2.77 million) for the land value, and equity of S$519,000 (US$342,482). Warees contributed in terms of management resources and nominal cash of S$1.00 (US$0.65).

Warees, on behalf of MUIS, entered into an Ijarah agreement with Ascott to manage the apartments for 10 years with a minimum guaranteed income of S$1.3 million (US$857,813) for the first year and S$1.8 million (US$1.18 million) from the second to the tenth years, with additional profits to be shared. This Ijarah income is paid out to the bond investors at S$1 million (US$659,849) (3.03%) per annum, with the remaining amount distributed between MUIS and Warees at an agreed ratio of 70:30.

Given the success of the Waqf model in Singapore, the strategy now is to replicate this model using Waqf land in other countries. In Malaysia, it will start with a prime Waqf near KLCC, in Kuala Lumpur, and in China prime Waqf and Muslim land has been identified in Shanghai, Beijing, Xi’an and Nanjing. The UK and Europe are also working in partnership with the European Muslim Trust to develop Waqf land there. The Waqf portfolio is an investment structure that can attract Muslim investors worldwide.Application of Islamic finance in REITs

Islamic real estate investment trusts (REITs) involve a fund which is contributed to by investors to own properties, who are then entitled to share the rental or capital gains proportionately. A REIT contract is binding on all investors through a Musharakah or partnership structure.A Wakalah or management contract governs investors and the fund manager. Intrinsic to Islamic REITs must be a Shariah compliant asset class. There is a potential for conflict where a property has a high yield, but a significant proportion of the rental income may not be Shariah compliant. A clear example is if the property is occupied by a conventional bank. The proportion of non-permissible rental income also varies depending on the REIT sponsor or majority investors. The one-third rule may suffice for some, however other investors, for example those from the Middle East, may request a lower tolerance of non-Shariah compliant activities, such as 10% or even zero tolerance.

It is therefore a crucial role of the asset manager to monitor tenancy profiles and business operations for existing tenancies, and especially those up for renewal, as well as the acquisition of new assets into the portfolio mix.

On the issue of leverage, Shariah rulings allow up to one-third of debt using conventional financing, but if leveraging is based on a Shariah structure, it is limitless. All insurance activities are required to be of Takaful schemes. Some Shariah boards may allow conventional insurance in the absence of any Takaful schemes.

In order to attract Islamic funds, the tax structure in the country of listing for REITs and for cross-border investments, as well as the tax structure for properties in the respective countries, must be transparent and provide for Islamic tax via the payment of zakat for charitable purposes.

Promoting Middle East investments into Asia

Feedback from Middle Eastern investors reveals that they are looking for a more diversified portfolio through a pan-Asia fund with an annual yield of 8%, a double-digit internal rate of return (IRR) and a possible exit strategy as REITs. The fund structure can be conventional or Islamic, or even a hybrid through a fund of funds. Sukuk (Islamic bonds) can be promoted for project financing and capital raising. This could also prove to be an avenue to support Singapore’s initiative to promote Islamic banking and wealth management investment opportunities in the Middle East.

The boom in construction activities across the Middle East has been due to demand within and outside the region, partly fuelled by high oil prices. There are exciting mega projects not just in Dubai but now also in other countries such as Bahrain, Kuwait, Qatar, Saudi Arabia, Egypt, Jordan, Lebanon and even Libya. Some of the Middle East funds are also being invested back home due to the high returns and zero tax. The emergence of funds by Middle Eastern institutions for portfolios of assets across the region is indeed appealing to Asian investors.

Many see the real estate sector as a safe haven for investments and the UAE is no exception. Given the backdrop of a growing population – arising from an influx of expatriates – ample liquidity, friendly regulatory environment, as well as its status as a regional investment hub, the UAE has been attracting international companies to establish offices.

Rising infrastructure spending, together with the construction of residential and non-residential properties, underpins the real estate sector, with the country now positioning itself as an attractive tourist destination.

Last year, real gross domestic product (GDP) is estimated to have grown by 8.2% to Dh357.6 billion (US$235.9 billion), with real estate and other related services contributing 7.4% of GDP. The sector witnessed strong activities buoyed by the increasing investment in infrastructure. This is due to the country positioning itself as an attractive tourist destination, in addition to the increase in the residential and non-residential units.

Bahrain is also witnessing strong real estate activities, with the total value of traded land permits estimated to have recorded cumulative average growth above 25% in the last five years.

Wealthy Qatar is another country where the real estate sector is booming. The sector’s contribution to the GDP has been sustained at 5.4% in 2006, compared to the previous year, and growth rate was around 18% in 2006. While this growth appears to be less impressive when compared to 36% in the previous year, the buoyant domestic economy has underpinned real estate demand in Qatar. The vital factors that have positively influenced this expansion are high population growth, superior per capita GDP and abundant resources.

Middle Eastern investors are looking into Asia to complement existing investments in the US and Europe. The requirement is for products with good returns. The trend is in property investment for matured markets through indirect investment vehicles such as property funds and REITs. There is also growing demand among Middle Eastern investors for Shariah compliant funds and a similar trend is picking up in Malaysia and Brunei.

Conclusion

There is an increasing trend for Islamic finance beyond just the global Muslim population. More conventional banks and industry players can be witnessed leaping onto the bandwagon, with the UK having formed the Islamic Bank of Britain as a full retail bank. Initiatives in Shariah home financing through Murabahah (mark-up sale) have been granted a waiver of the double stamp duty in Singapore. There is also growing demand for Shariah property funds and REITs, especially into Asia. Middle Eastern investors have a keen interest to diversify into Asia, but there is still a lack of good assets for investment.

One suggestion is for Asian governments to open up office buildings owned by statutory boards and government-linked corporations (GLCs) to attract more foreign investments through property funds and REITs. Pan-Asia Islamic REITs are able to tap the growing Muslim funds for both institutional and retail investors across the board – local, regional and Middle Eastern investors. The performance of Islamic REITs, however, may be constrained by certain Shariah principles, and asset classes can be mitigated through better structures and strong asset management. Over the next few years, REITs will evolve across Asia and grow significantly, but this must be in tandem with conducive regulatory and tax frameworks.

[email protected]

.