“As a former CEO of an Islamic bank and now the vice-chairman of a university dedicated to Islamic finance, I was concerned that many Muslims and people of other faiths just did not have a grounding in the fundamentals of Islamic finance. Indeed, the first edition also proved very popular with practitioners who found it to be a useful primer and reminder.” – Daud Vicary Abdullah, co-author of Islamic Finance.

The second edition of ‘Islamic Finance: Why it makes sense for you,’ by Daud Vicary and Keon Chee was published this year by Marshall Cavendish. The following excerpt is taken from Chapter 10 ‘Other Islamic Financing Methods.’

We have covered the three methods on which most of Islamic financing in Southeast Asia are based: BBA and Murabahah (cost-plus financing methods) and Ijarah (leasing). What we will look at in this chapter are brief descriptions of other Islamic financing methods, which can be broadly divided into two categories — those that are equity-based and those that are debt-based (see Table 10.1).

Equity-based financing methods

There are two main kinds of profit-loss sharing, or equity-based, financing contracts:

-

Mudarabah; and

They are far less popular than debt-based financing methods because, as we will see, they are more challenging to implement. Nevertheless, while equity-based methods are less popular, they are ideal for community building and risk-sharing. Consider the plight of the entrepreneur who has a promising idea for a new venture but does not have sufficient capital. If he were to go for debt-based financing, the bank would very likely make him pay a higher profit mark-up. That is because his venture will be perceived as having a fairly high chance of failing within a year. High financing charges increase the danger of failure.

Profit-sharing (Mudarabah)

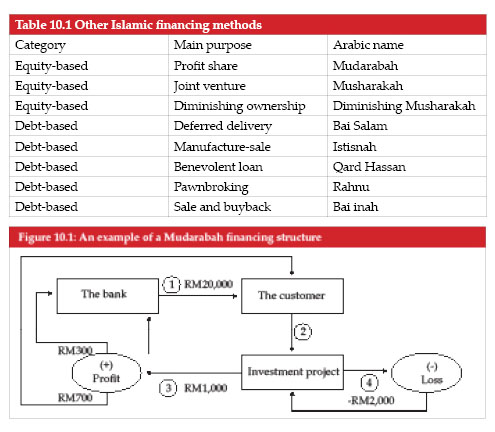

Profit-sharing or Mudarabah was discussed in Chapter 7 on Islamic deposits where the customer is the capital provider to the bank. The concept is exactly the same in this chapter, except that in a financing situation, the bank (not the customer) is the capital provider. The customer plays the role of entrepreneur who seeks funds to operate a business.

If profits are generated, the profits are distributed according to a pre-agreed profit-sharing ratio (PSR). Losses, on the other hand, are entirely absorbed by the bank. A simple Mudarabah financing structure is presented in Figure 10.1.

Let us suppose Jalilah has a business idea to recycle old computer parts for cash. The bank reviews her business plan and agrees to fund the project.

-

Jalilah obtains financing of RM20,000 (US$6,136) from the bank. The PSR is 30–70 (30% to the bank and 70% to Jalilah).

-

Jalilah sets up the business and manages its operations.

-

Suppose there is a net profit of RM1,000 (US$306), then 30% or RM300 (US$92) is the bank’s share and 70% or RM700 (US$214) is Jalilah’s share.

-

In the event of a loss of, say RM2,000 (US$613), the bank (capital provider) is solely responsible for the loss.

Joint-venturing (Musharakah)

A joint venture is a business enterprise undertaken by two or more entities (persons or companies) to share the expenses and profits of a particular business project. It is a form of partnership that is limited to a particular purpose.

Among the main benefits of joint ventures is that partners save money and reduce their risks through capital and resource sharing.

Musharakah refers to an Islamic joint-venture partnership in which the bank and its customer agree to combine financial resources to undertake and manage a business venture, according to the terms of an agreement.

Profits are shared according to a PSR while losses are shared in proportion to the amount of capital each contributed.

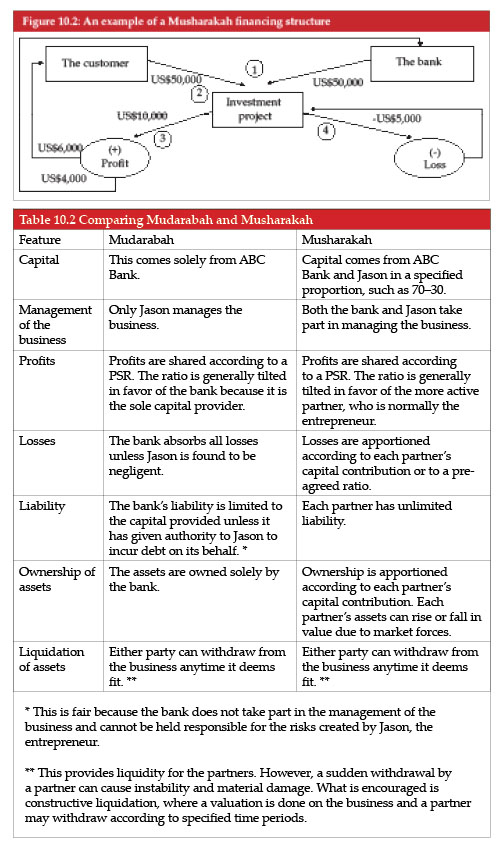

Figure 10.2 shows a basic Musharakah structure where the customer Jamil and the bank put in equal capital of US$50,000 each into a project. According to terms of the agreement, profits will be apportioned 60–40 in favor of Jamil as he will be the main party managing the project.

Losses, on the other hand, will be shared equally. Banks mostly leave the responsibility of management to the customer-partner, and retain the right of supervision and follow-up. Or they might even become active partners in a whole range of activities to ensure that the objectives of the company are met.

-

The bank and Jamil agree to each contribute US$50,000 to a joint-venture project.

-

Jamil is the main party to manage the project.

-

Suppose profits amount to US$10,000, these will be shared US$6,000 or 60% to Jamil and US$4,000 or 40% to the bank.

-

If there is a loss of, say US$5,000, the loss is shared 50–50, that is, US$2,500 each. The loss directly brings down the value of the project’s assets.

Comparing Mudarabah and Musharakah

Equity-based financing using Mudarabah and Musharakah involves the sharing of risk and returns. These two methods of financing are often compared in terms of their differences (see Table 10.2). To simplify the comparison, let us suppose that ABC Bank is the capital provider and Jason is the entrepreneur in a financing situation.

Diminishing Musharakah

A financing transaction based on diminishing Musharakah is straightforward. At the start of the transaction, the bank owns most of the asset. As instalments are made by the customer, the customer’s share increases while the bank’s share declines or diminishes. The ownership of the bank ends when all payments are made and the customer completely owns the asset.

© Marshall Cavendish Asia (International)

For more information, please visit

www.marshallcavendish.com/genref