Islamic banking and finance, by and large, is a burgeoning industry in Sri Lanka. However, the key barrier to the industry’s growth and development, similar to that of any other industry is a lack of standardization with regard to regulations governing Islamic financial products. Fully-fledged Islamic financial institutions and Islamic business units are facing issues with regard to investing their surplus funds and statutory reserves in non-Shariah compliant financial instruments (interest-bearing treasury bills/bonds) with Central Bank of Sri Lanka, which does not earn any income from the Islamic financial institutions.

A lack of standardization causes increased costs, increased barriers to entry into the market and reduced competitiveness in comparison to comparable products. Indeed, different jurisdictions took different approaches to the problems faced with the lack of standardization. In Pakistan, the State Bank of Pakistan issued a clear directive and rulings that segregated all processes and standardized the Islamic finance business operation. Similarly, Malaysia’s central bank, Bank Negara Malaysia established a national Shariah council with vested power to oversee the industry while segregating its operation.

Review of 2015

The year 2015 brought a new era to the Islamic finance industry of Sri Lanka by focusing aggressively on market development and expanding the horizon of Islamic finance in Sri Lanka, putting the principles into practice without any presentiment. Identifying issues with Islamic finance as an alternative to regular finance such as the need to establish Islamic business values and change the process of meeting Shariah compliance is increasingly important and also a reflection of the increasing wealth and capacity of investors, both Muslim and non-Muslim, to seek and invest in new investment products that serve their needs.

Further political stability and good governance has increased the confidence of local and foreign investors. The Sri Lankan equity market has moved to a new growth phase, with a compound annual growth rate of 15.7% from the 30th September 2009 to the 30th September 2015. The economy is expected to grow in excess of 5% in the next two years. Although a new government came into power this year, the investors were cautious ahead of the government’s policy statement to undertake any new investment projects in Sri Lanka.

Islamic finance industry practitioners are very positive and there have been some new investment products introduced to the market by a few Islamic financial institutions, for example, an Islamic money plus saving product, a unit trust investment to attract small-time investors. This investment is free from withholding tax and a unique feature of this product is that the investor can enter into this investment scheme with small units and he/she can exit from the investment at any time. Another unit trust company is working on an Islamic cash fund to attract the big players.

There has been another interesting initiative this year, with two insurance companies, namely People’s Insurance and LOLC Insurance, opening Takaful windows offering Shariah compliant insurance services to their customers, making the Takaful market more competitive in Sri Lanka. The monopoly status of Takaful operation has now become very challenging to pioneer operator Amana Takaful.

Two more financial service providers have joined the fold of Islamic finance in Sri Lanka: Commercial Leasing Finance and Adam Capital.

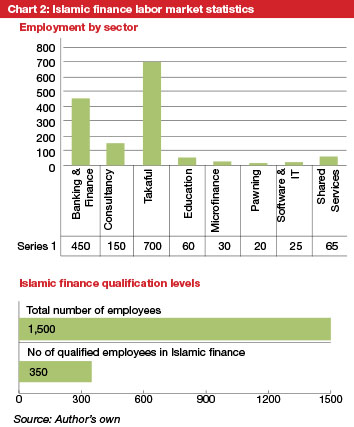

The total number of players in the Islamic finance industry in Sri Lanka currently stands at 44, of which 16 players are in the banking and finance sector, with four in the Takaful sector, nine in the consultancy and advisory sector, four in the education sector, three in the software and IT sector, two in the publishing sector and two in the microfinance sector. There are seven registered market intermediaries who act as investment managers for the Islamic capital market in Sri Lanka.

Preview of 2016

The Islamic finance industry in Sri Lanka is waiting for a government policy statement on new initiatives in 2016. Reports indicate that there may be a positive policy statement toward encouraging capital market operations for Sukuk and other new Islamic banking products. Sukuk are seen as well-suited for infrastructure financing for a developing economy. Sri Lanka is now on the verge of developing the infrastructure facilities. For example, Malaysia has used Sukuk to develop airports, marine ports and roads. Furthermore, Sukuk are listed debt instruments in many countries, such as Malaysia, Singapore, Luxembourg and the UK. A platform to list Sukuk on the Colombo Stock Exchange has been proposed in order to create a platform for secondary market trading and this would pave the way in attracting funds from the Middle East.

A new development was witnessed recently with the formation of the Association for Alternate Financial Institutions (AAFI). The objective of the AAFI is to create a forum for members to voice out and discuss issues pertaining to the Islamic banking industry.

The AAFI is now taking initiatives and lobbying the government to introduce alternative treasury bills/bonds for Islamic finance institutions to park their surplus funds and to generate income to support banking activities and also to assist the government in raising funds for the treasury.

Conclusion

Islamic finance has been moving steadily and with a positive government policy statement on the horizon, the Islamic banking sector is expected to shift to a new epoch. The setting-up of the AAFI will make a difference in the Islamic banking sector in Sri Lanka by having a collective representation of the relevant policymakers and regulatory authorities to facilitate accounting, tax and legal changes.

Imruz Kamil is the head of Islamic finance at Richard Pieris Arpico Finance. He can be contacted at [email protected].