MD TOUHIDUL ALAM KHAN discusses why Islamic banking is gaining momentum in Bangladesh.

Islamic banking in Bangladesh will celebrate its golden jubilee in 2033, on the eve of 50 years of banking. The present shape of Islamic banking in the country is being modernized in terms of this changing scenario, in tandem with the forecast for the world economy in 2033. Realizing the importance of this, the central bank, Bangladesh Bank, recently introduced new guidelines for Islamic banking.

The central bank stated that as Islamic banking has become a part of mainstream banking in Bangladesh, it is necessary to introduce the guidelines to bring greater transparency and accountability. With this circular, Islamic banks now have a legal framework recognized by Bangladesh Bank and the government. Islami Bank Bangladesh, the first Islamic bank in the country, has gained the premier position among the private banks in terms of deposits, investment, export and import, and remittance collection in the country.

Islamic financial institutions in Bangladesh

Islami Bank Bangladesh started its Islamic banking operations in 1983. Now, there are seven Islamic banks out of the 47 banks in the system and 15 banks with Islamic operations.

In addition to the 47 banking institutions there are 29 non-financial institutions (NFIs) in the country. Two of these, Islamic Finance and Investment Limited and Hajj Finance Company, operate on Islamic principles.

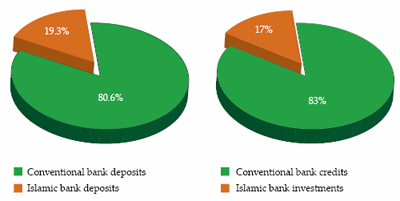

The total figure of deposits under Shariah financing is BDT669.54 billion (US$8.95 billion) out of total bank deposits of BDT3.46 trillion (US$46.28 billion) and the Islamic investment position is BDT646.47 billion (US$8.64 billion) out of total bank credit of BDT3.79 trillion (US$50.78 billion) as at the 31st December 2010. Islamic banking constituted 19% of deposits and 17% of advances of the country’s total banking system in 2010.

First Shariah-based syndication financing in Bangladesh

A total of three syndication deals have been concluded in the country. In 2006, Prime Bank Bangladesh acted as the lead arranger of the first Shariah-based syndication deal for a pharmaceutical project in which three Islamic banks participated.

Three years later, Prime Bank arranged funds through another syndication deal for a ceramic tiles manufacturing project where six Islamic banks participated. Islami Bank Bangladesh also participated in this deal.

Why is Islamic banking gaining momentum in Bangladesh?

The country’s Islamic finance boom can be attributed to a number of factors. Bangladesh is the world’s third largest Muslim-majority country, with Muslims making up more than 80% of the nation’s population of 148 million. As the religion prohibits earning or paying interest, Islamic banking makes it possible to operate interest-free business, contributing to its growth momentum in Bangladesh.

The growth rate of Islamic banking in the country is 15%-20%, while for conventional banks it is 10%-15%. Islamic finance is one of the fastest growing sectors in the financial industry in Bangladesh.

The industry, at present, has been growing at 20% per annum. The growth follows a guideline for Islamic banking released by the central bank in November 2009 which allowed the introduction of either new fully fledged Islamic banks or the conversion of conventional banks into Islamic. The new regulations also restricted further banks with dual operations.

Despite the restriction, the industry is growing and industry watchers feel that if the rate of growth continues, Islamic banking in Bangladesh will become the mainstream system within the year 2025.

In a recent seminar Dr Atiur Rahman, the governor of Bangladesh Bank, said: “The strengths of Islamic banking served well to protect Islamic banking during the global financial crisis while many conventional banks and financial institutions collapsed, including some with global stature and renown. The profit and loss sharing nature of liabilities of Islamic banks is a good safeguard against solvency risk, while prohibition of financial speculation serves well in keeping their books free of speculative assets and derivatives that proved toxic and worthless in the crisis.

“These strengths of Islamic banking are now attracting conventional banks in increasing numbers, including large global ones, into Islamic modes of financial services.” It was also concluded from the seminar that by 2025, the market share of Islamic banking will rise to 55% and it will become the country’s mainstream banking system.

Kawsar Ahamad, the executive officer of Prime Bank, who also looks after the investment portfolio of all of the bank’s Islamic branches, opined that one of the challenges faced by Islamic banking in Bangladesh is that: “In a mixed economic and financial system such as that in the country, where both the conventional and Islamic banking systems prevail, sometimes bank-to-bank transactions and international transactions may not be done in compliance to the full Shariah system.”

Another challenge facing the growth of Islamic banking is inadequate Shariah compliant working capital mode of finance. Hence proper attention from the government and all other regulatory bodies, especially the central bank, is required to boost Shariah compliant banking.

The absence of a Shariah compliant money market system is also a hindrance for the growth of Islamic banking in the economy. Besides this, Ahamad feels deeply that a profit-based model is the prime need instead of an interest-based model in pricing and designing Islamic financial products.

Md Touhidul Alam Khan is the executive vice-president, corporate banking division of Prime Bank and associate fellow member of Institute of Islamic Banking and Insurance, UK. He can be contacted at

[email protected]

.