“Those who live on usury will not rise up before Allah except like those who are driven to madness by the touch of Shaitan. That is because they claim: ‘Trading is no different than usury, but Allah has made trading lawful and usury unlawful. He who has received the admonition from his Rabb and has mended his way may keep his previous gains; Allah will be his judge. Those who turn back (repeat this crime), they shall be the inmates of hellfire wherein they will live for ever (Al-Baqarah,275).” On that note, RALEENA THASSIM JUNKEER analyzes whether Sri Lankan Muslims’ faith influences their economic behavior.

Unlike prior to 2011, today Islamic banking and financing facilities are conveniently available for Muslims in Sri Lanka. Would this improvement in the financial services industry result in the active transfer of funds from the conventional financial system to the Islamic financial system because Muslims’ faith influences their economic behaviour? An RIU survey conducted in the last quarter of 2014 shows a significant percentage of Muslims tend to compromise their religious beliefs when making financial decisions.

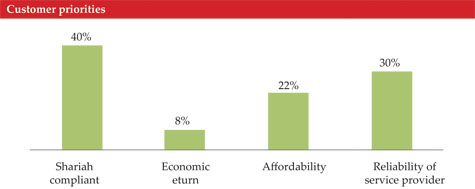

Surprisingly, only 40% of the respondents considered Shariah compliance as a top priority when selecting a financial service provider. These respondents expressed strong faith in Islam and believed Islam should be practiced in all aspects of life. The majority (86%) of them had a clear understanding about Islamic finance. This segment of the customers is loyal to the industry and actively contributes to its growth. On the contrary, Shariah compliance was not a top priority to the remaining 60% of the respondents. This trend is distressing due to two reasons. Firstly, it questions the sincerity of Muslims to Allah and secondly, it questions the strength of the most prominent unique selling proposition of its niche market. Thus, a company highly capitalizing on ‘Shariah compliance’ to position its products and services may not be able to reap the expected results.

Reliability is also an important determinant of Muslims’ choice of a financial service provider. Some 30% of the respondents preferred a conventional financial service provider over an Islamic financial service provider if the latter is proven to be more reliable although they were aware of prohibition of interest in Islam and had a good perception about Islamic finance. The faith of these customers has very little influence on their economic decisions. They give priority to the security and efficient management of their funds. As building credibility requires a long time, the transfer of funds of this type of customers from a conventional to the Islamic system will take place at a rather sedate pace.

Even though the percentage is insignificant, 8% of the respondents selected their financial service provider based on economic returns. The positive indication of this trend is that the majority of the respondents are willing to pay a little more or willing to accept a little less for a reliable and Shariah compliant Islamic financial institution. The study also indicates that industry players are required to divert their attention to address the misconceptions about Islamic finance among Muslims. Sixty percent of those who based their financial decisions on economic value believed Islamic finance is no different from conventional finance. Clearing their misconception may encourage them to switch from a conventional to the Islamic financial system. The other 20% of the respondents understood the concept of Shariah compliant financing and yet, preferred to select their financial service provider based on cost and returns as their faith had no influence on their economic behavior.

It is noteworthy that 22% of the respondents compromised Shariah compliance for affordability. Nearly 70% of them exhibited a strong faith in Islam and Islamic finance but are forced to seek conventional financial solutions due to their financial constraints. This segment of customers believes Islam permits such compromises in order to fulfill necessities. However, they will readily shift from a conventional system to the Islamic system if the rates of Islamic financial service providers are affordable. Competitively pricing its products and services is challenging to the industry players because Shariah compliant institutions incur additional costs and cannot benefit much from economies of scale like its counterparts. However, if the Islamic financial service providers can ease the financial constraints of this segment of customers, they will become loyal customers of the industry.

In a nutshell the faith had a substantial influence on the economic behavior of 40% of the respondents. However, the remaining 60%’s economic behavior was driven based on assurance, affordability and economic benefits. Therefore, firstly the Islamic financial institutions should actively be involved in educating Muslim communities and creating awareness about the graveness of the Islamic rulings they conveniently compromise, to create the correct mind-set of its target market. Secondly, the industry players should try to make its products more appealing in terms of what customers value rather than heavily depending on the ‘Halal’ status to promote its products to customers. The correct mind-set and appropriately packaged products will accelerate the growth of the Islamic finance industry of Sri Lanka.

Raleena Thassim Junkeer is a consultant at Research Intelligence Unit. She can be contacted at [email protected] .