What is Murabahah?

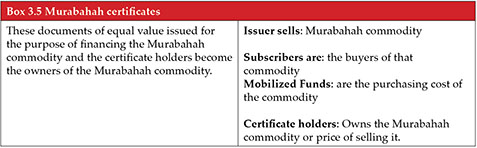

As mentioned above Murabahah is a purchase and then resale transaction which is a way of accessing funds instead of raising them through borrowing. The capital provider purchases the desired commodity from a third party and resells it at a predetermined price to the capital user. The capital user has effectively obtained credit without paying interest by paying the agreed price by installments, by deferral, over time.

What are Sukuk Murabahah?

With Sukuk Murabahah the SPV can use the investors’ capital to purchase an asset and sell it to the obligator on a cost-plus-profit-margin basis. The obligator (the buyer) makes deferred payments to the investors (the sellers). This arrangement is a fixed-income type of Sukuk, and the SPV facilitates the transaction between the Sukuk holders and the obligator.

A company (the originator) needs, say US$100 million. It will issue Murabahah Sukuk for this amount by selling assets to the special purpose vehicle (SPV) for US$100 million. The SPV will finance the company and buy the asset by issuing Murabahah Sukuk equal to the amount needed to purchase the asset ($100 million). The investors will share the proportion of that asset as Sukukholders.

After the SPV buys the asset, it will sell it back to the company at a predetermined amount of money equal to the initial amount and the margin. The payments represent the periodical payments for the investor. At maturity, the investors get the full amount of the Sukuk payment and the return of the principal of the Sukuk Murabahah.

How do you structure Sukuk Murabahah?

With Sukuk Murabahah the SPV can use the investors’ capital to purchase an asset and sell it to the obligator on a cost-plus-profit-margin basis. The obligator (the buyer) makes deferred payments to the investors (the sellers). This setup is a fixed-income type of Sukuk, and the SPV facilitates the transaction between the Sukukholders and the obligator.

The Murabahah contract process begins with the obligator (who needs an asset but cannot pay for it immediately) signing an agreement with the SPV to purchase the asset on a deferred-payment schedule. This agreement describes the cost-plus margin and deferred payments, the key features of a Murabahah contract.

After the contract is signed the Sukuk Murabahah is structured as in Figures 3.4 and 3.5 and follows the steps below:

-

The investors subscribe to the Sukuk and pay the proceeds to the SPV, which acts as their trustee.

-

The SPV issues Sukuk certificates to the investors.

-

The SPV purchases the asset from a supplier.

-

The SPV sells the asset to the obligator as per the contract and per the contract terms. The delivery takes place on the spot.

-

The obligator pays the deferred payments to the SPV in a lump sum or by installments.

-

The SPV distributes the deferred payments to the Sukukholders.

This format was used in 2005, when Bahrain-based Arcapita Bank issued Murabahah Sukuk with a five-year term for US$200 million. The bank used proceeds from these Sukuk to purchase commodities that it then sold.

Key features of the Murabahah structure

-

The consideration (deferred price) must be at an agreed rate and for an agreed period;

-

In order to ensure that the issuer SPV obtains marketable title to the commodities from the commodity supplier in order to facilitate their on-sale to the originator. The issuer SPV may require certain representations and warranties from the commodity supplier that the commodities will be purchased free of any encumbrances or liens;

-

During the period of ownership of the commodities, by the issuer SPV, there is the risk of price fluctuation in the market value of the commodities. This can be mitigated by minimizing the duration of issuer SPV’s ownership and specifying the deferred price payable by originator (as purchaser);

-

If the originator requests physical delivery (as opposed to constructive delivery) there may be a risk that the commodities are damaged whilst in transit. This risk may be mitigated by undertakings from the originator in the Murabahah agreement to accept the commodities on “as is” basis;

Tradability Issues with Sukuk Murabahah

-

A potential problem with Murabahah Sukuk is that these cannot be traded in the secondary market at a negotiated price and hence, are not liquid. Murabahah receivables are in the nature of pure debt and hence the instrument that is evidence of such debt (Shahadat-Al- Dayn) can be transferred only at its face value.

-

The practice, however, has been found to be totally unacceptable in the Middle East and other parts of the globe. It has been rightly asserted that the sale of debt at a negotiated price (price that is different from the face value of debt) or at a discount opens the gates to riba-based transactions. Only if investors hold on to the instruments until maturity would the yield on the instrument constitute a legitimate profit and not be riba.

When can Sukuk Murabahah be traded?

-

This is because the Shariah analysis turns on whether there is some ongoing ownership stake between the Investor and the Sukuk asset following a transfer of the Sukuk certificate (which is permitted) or whether the transfer shifts ownership and creates a debt obligation on a third party (not permitted). As such, Sukuk, certificates issued prior to a Murabahah commodity sale would represent ownership in those commodities rather than the right to the receivables generated by their sale;

-

Sukuk certificates derived from an underlying Murabahah structure may still be negotiable if the Murabahah receivables form a small proportion (exact percentages may vary depending on the transaction and the analysis of each Shariah scholar) of a larger portfolio of Sukuk assets .These assets would comprise mostly other negotiable instruments such as Sukuk Ijarah, Sukuk Musharakah and/or Sukuk Mudarabah and are usually packaged into a hybrid Sukuk.

As mentioned despite being debt instruments, the Sukuk Murabahah could be negotiable if they are the smaller part of a package or a portfolio, the larger part of which is constituted of negotiable instruments such as Sukuk Mudarabah, Musharakah, or Ijarah.

Sukuk Murabahah have, however, become popular in Malaysian market due to a more liberal interpretation of Fiqh by Malaysian jurists permitting the sale of debt (Bai-al-Dayn) at a negotiable price. This makes Sukuk Murabahah Shariah compliant within Malaysia. This is discussed on box story.

It should be noted that although some of these instruments have been generally accepted as being in compliance with Islamic principles in order that they can be traded in the secondary market, the negotiability of certain others is still a point of debate. This is due to controversy surrounding their legal acceptability or compliance with the Shariah. The effect is that some of these bonds can be traded in the secondary market while the trade of others is limited to the primary market because Shariah acceptability means that they can only be exchanged at face value.

It is important to understand that differing regions of the world follow different schools of jurisprudence (madhabs) with the effect that the acceptability of Sukuk from some madhabs are not acceptable to others. In fact the Malaysian schools have very different rulings from the GCC madhabs.

Brian Kettell was, until recently, an advisor to the CEO at ICD, part of the Islamic Development Bank (IDB) Group based in Jeddah, Saudi Arabia. He had many Shariah-related responsibilities and was actively involved in the ICD Sukuk structuring team.

He worked for several years as an advisor for the Central Bank of Bahrain where he worked on structuring the first two Sukuk ever issued.

Subsequently, Kettell taught workshops on Islamic banking and finance at a range of financial institutions including the World Bank, African Development Bank, National Commercial Bank (Saudi Arabia), Global Investment House (Kuwait), Noor Islamic Bank (UAE), the UK Treasury, the Central Bank of Iran, the Central Bank of Syria, the Securities Investment Institute and the Institute for Financial Services .

Kettell is the most published book author on the subject in the world. He is the author of :

• Sukuk: A new Global Investment Asset Class (Oxford Press)

• Sukuk : A Guide to the Shariah Structures (Oxford Press)

• Case Studies on Sukuk (Oxford Press)

• Islamic Capital Markets (Oxford Press)

• Islamic Finance in a Nutshell (John Wiley)

• Frequently Asked Questions on Islamic Finance (John Wiley)

• Introduction to Islamic Banking and Finance (John Wiley)

• Case Studies on Islamic Banking and Finance (John Wiley)

• A Workbook on Islamic Banking and Finance (John Wiley)

• Islamic Sukuk : A Definitive Guide to Islamic Structured Finance

• Opportunities in Islamic Finance (ed):CPI Financial

• Islamic Banking and Finance in the Kingdom of Bahrain (BMA)

Contact details

www.gulfSukuktraingcourses.com

[email protected]

mobile : +971 (0) 566399300