Some bankers and analysts were disappointed that 2013 brought a less robust performance in the Sukuk sector than 2012’s record-setting year. However, the leading markets continued to cement their strong performance, while new players also emerged on the scene to demonstrate the ever-widening global scope of the Islamic capital market.

The UAE re-emerged as a leading center for Sukuk issuance in 2013. With the new UAE Sukuk rules expected in early 2014 and the ratcheting up of Dubai’s plans to become the leading center of the Islamic economy, we should expect Dubai to grow its role as a jurisdiction of choice for Islamic capital market transactions.

As always, Malaysia provided the largest universe of deals to analyze. Keeping their hat in the ring, the number of cross-border deals from Malaysia is also growing as Malaysian financiers supported deals in Indonesia, Saudi Arabia, and Singapore.

Saudi Arabia’s strong domestic Sukuk market enjoyed the first ever clear sovereign support for an Islamic capital markets transaction. Turkey, Pakistan and Indonesia continued to make contributions, whilst Egypt, Nigeria and Oman jumped onto the Islamic capital markets scene with notable deals.

The first hint of tapering threw a scare into the Islamic capital markets in mid-2013. Nonetheless, as the slowing of quantitative easing in the US becomes a fact, most of the Islamic financial market players are adapting. As always, the Islamic syndicated finance market filled gaps that the Sukuk markets were not able to cover. A number of private equity, corporate finance and real estate equity deals also drew attention.

In all, you nominated nearly 400 deals (a 33% increase over 2012) in over 30 categories (a 20% increase over 2012). The 2013 Deal of the Year competition soared past the record set in 2012.

Although 2013 showed more execution of well-tested ideas than innovation and despite local political unrest in several key countries and global markets as well as the dismay over tapering, 2013 remained a good year for the Islamic capital markets.

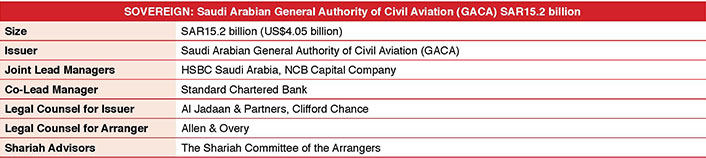

The top nominees for Deal of the Year included Saudi Arabian General Authority of Civil Aviation (GACA), Malaysia Building Society (MBSB), East Delta Electricity Production Company and Emirates Airlines. Each of these deals represented an important landmark in the industry, or a new development of benefit to the market. With GACA as the largest MENA Sukuk issuance ever; East Delta delivering a new product during difficult times; and the MBSB and Emirates deals demonstrating new concepts that may be replicated throughout the markets, no choice was easy.

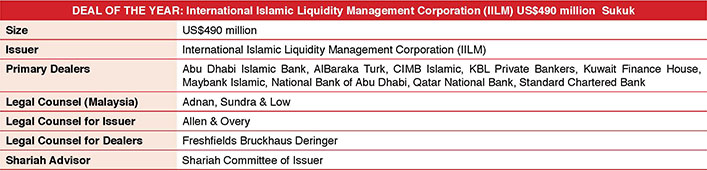

Nearly three years in the making, the International Islamic Liquidity Management Corporation (IILM) issued its first Sukuk in 2013. Designed to support the Basel III-driven needs of Islamic banks to have access to high-grade, easily traded securities, the transaction was well received. Finally stepping into its role to support the Islamic financial services industry, the inaugural Sukuk of the IILM won the Islamic Finance

news Deal of the Year for 2013.

(The IFN DOTY Awards Board)

The Islamic Liquidity Management Corporation (IILM) is an international institution established by central banks, monetary authorities and multilateral organizations in 2010 to create and issue short-term Shariah compliant financial instruments to facilitate effective cross-border Islamic liquidity management. The IILM issued its first Sukuk from a US$2 billion short-term Sukuk program. Rated by S&P, the issuer is a Luxembourg incorporated securitization vehicle. One reason for the difficulty in launching was how to acquire access to government-sponsored assets in sponsor state jurisdictions. The deal also had to reconcile Shariah principles with Luxembourg civil law. Underlying the deal are a number of Sukuk issues which were privately purchased by IILM Holding 2. The Sukuk were issued by sovereign-related entities and were issued in Ijarah and Murabahah format. In order to ensure the Sukuk achieved the rating requirements for the short-term Sukuk program, collateral and credit enhancement features were incorporated into the deal.

-

The Sukuk are tradable US dollar-denominated short-term financial instruments with maturities of up to one year;

-

The Sukuk qualify as money-market instruments backed by sovereign assets; and

-

The Sukuk are tradable globally via a multi-jurisdictional primary-dealer network.

As a result, the IILM’s Sukuk have strong global support as they represent a unique collaboration between several central banks and a multilateral development bank. Apart from meeting the market demand for highly rated short-term Shariah compliant cross-border liquidity instruments, the IILM short-term Sukuk complement the intermediate and long-term Sukuk currently available in the market. The US dollar short-term cross-border Sukuk should address the challenges that Islamic financial institutions face in managing their liquidity more effectively and efficiently.

Honorable Mention for Deal of the Year included GACA; Malaysia Building Society; East Delta Electricity Production Company; and Emirates Airlines.

Innovation was not a hallmark of 2013. Two airlines came to market with seat voucher deals (Emirates and Pakistan International Airlines). Barwa’s The First Investor secured Istisnah financing for a major project in the US. and DanaInfra launched the first Malaysian retail Sukuk, albeit using tried and true methods. Telekom Malaysia’s Islamic commercial paper (ICP) program and Islamic medium-term notes (IMTN) program have a total combined limit of up to RM3 billion (US$912.57 millon) in nominal value applying the concept of Sukuk Wakalah. Telekom Malaysia’s seven-year Sukuk is the first to utilize broadband units as an underlying asset. Returns on the Sukuk come from a share of the profit generated by the issuer’s broadband services as represented by a specific number of broadband units which Telekom Malaysia sells to customers on behalf of the Sukukholders.

Airtime, toll vouchers and seat vouchers have already qualified as underliers for Islamic transactions. The application of broadband units are a unique addition to the universe of intangible assets and facilitate Telekom’s speed to market on future issuances by not requiring the company to deal in complex sales and lease back transactions involving land, buildings, or switching stations. This method is a logical extension into the intangible asset base of most telecommunications companies and one may expect to see the method expand globally.

Honorable Mention: CityCentreDC; Emirates Airlines; Pakistan International Airlines; and DanaInfra Nasional

2013 was the year of sovereigns doing over. Structures and methods were almost universally repeated from prior year deals. In a thicket of similar deals, GACA just barely pips the rest. Due in 2023, GACA’s second issuance by GACA was oversubscribed and represented the largest ever issuance in the Kingdom of Saudi Arabia and the GCC. The hybrid Sukuk released funds to finance the redevelopment of the King Abdulaziz Airport, Jeddah and King Khalid International Airport in Riyadh. One wing of the finance was invested in a Murabahah to create certainty of payment and redemption. The second wing was invested in the purchase of benefits owed to GACA, which entitles GACA to charge and collect fees from airlines landing and parking aircraft at airports in the Kingdom. The second wing, essentially a Mudarabah, established the basis for the deal being tradable. This form of hybrid has become widely used in the past three years.

Honorable Mention: Government of Pakistan; Khazanah Nasional; Government of Dubai; Republic of Indonesia; and Republic of Turkey.

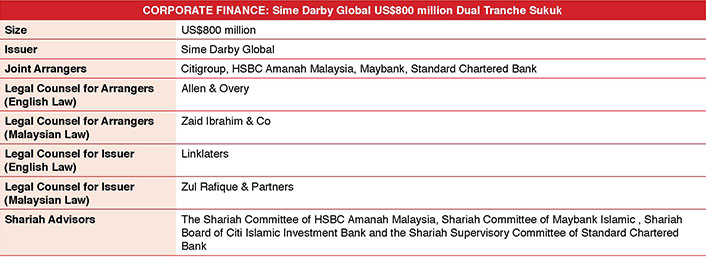

In 2013, there was an active corporate finance market with a number of landmark mergers and acquisitions, syndications, and a number of creative deals. Sime Darby’s Reg S program is Asia’s first internationally rated multi-currency Sukuk program based on an Ijarah structure. The issuer, Sime Darby Global, is an SPV which operates a multi-currency Islamic securities program by acquiring the beneficial ownership of assets from Sime Darby. The asset purchases resulting from each issuance are to be applied by Sime Darby to finance its own or its subsidiaries’ working capital requirements, to finance future investments, capital expenditure, and/or to refinance debt obligations of the parent or any subsidiaries. Each issue of Sukuk has a different group of plantation assets underlying the issue; the assets themselves may reside in various subsidiaries of Sime Darby. Complexities in the deal related to asset jurisdiction, matching back-to-back lease arrangements, and ease of determining the execution of transfer of beneficial ownership.

Honorable Mention: BIMB Holdings; Gulf Marine Services; SP Setia; and Dabbagh acquisition of stake in Petromin.

The problems of the financial crisis are slowly fading away in the GCC. In 2013, there were many high profile restructurings. A’ayan was one of the standouts as it was the first Shariah compliant restructuring under application of the financial stability law in Kuwait (Decree No. 2 of 2009). As a Shariah compliant company, the defaulted structures included Murabahah and other Islamic instruments. The ultimate restructuring involved a number of innovative restructuring techniques including ‘haircut’ arrangements, debt-for-equity and debt-for-asset swaps. Many of these were first applied in the Kuwaiti legal and regulatory context.

Honorable Mention: Arcapita; Dana Gas; Noor Hospitals; and DEWA.

The nominated high quality cross-border deals in 2013 was diverse and exciting. The top nominees opened new markets, found innovative ways to raise capital, and posed a challenge for us to make decisions. Maran Nakilat brought Qatari funds to a new market in Greece. Al Noor Hospitals Group raised equity and listed on the London Stock Exchange (LSE), applying the proceeds to its healthcare business in the UAE. Mobily brought in the largest joint Scandinavian export credit agency (ECA) financing to the MENA region and introduced Finland’s ECA to the Islamic market. Kuwait’s Al Kharafi Group secured its guarantees for the modernization and expansion of the Kuwait International Airport form Dubai Islamic Bank. Atlanticlux Lebensversicherung generated funding for FWU’s Takaful operations. Abu Dhabi Equity Partners opened the Brazil market with a novel trading platform. And Arcapita famously reorganized their debts in New York bankruptcy court.

The International Bank of Azerbaijan stands out as the opening of a new Islamic finance destination for GCC and American banks. The cross-border Islamic syndicated financing transaction was the first Islamic facility raised for an Azerbaijani bank. Among the key obstacles to the deal was the fact that a substantial number of banks in the GCC have no country limits for Azerbaijan. When the deal was being pulled together, the syndicate had to overcome internal differences about how to execute the Tawarruq structure. The bank itself is conventional with an Islamic window, as Islamic finance is still in its infancy in Azerbaijan. On the one hand, the deal contributes to building this market. On the other hand, the size of the market means that opportunities are limited.

Honorable Mention: Maran Nakilat; Al Noor Hospitals Group; Mobily; Al Kharafi Group; Atlanticlux Lebensversicherung; Abu Dhabi Equity Partners; and Arcapita.

The 2013 syndication market was active with a number of mega deals across markets as well as well-targeted smaller syndications in local markets. Although the CityCentreDC deal represents the opening of a new market, the method is the tried and true Istisnah. Astra Sedaya Finance was remarkable as the first Wakalah syndication for Indonesia. The Saudi Aramco Mobile Refinery (Samref) relied on Tawarruq.

The Gulf Marine Services deal is structured to provide a flexible secured facility to the company and to provide for future cash needs, an uncommon feature in Murabahah deals. Gulf Marine Services is a regional leader in the provision of services requiring self elevated support vessels and anchor handling tug supply vessels. Generally, the asset-heavy company serves the oil, gas and renewable energy sectors. In addition to vessels, the company offers offshore accommodation, well maintenance, project management, construction and installation services.

The complex Ijarah transaction allowed Gulf Marine Services to re-profile of existing debt into a multi tranche facility, fund a US$80 million dividend, finance expansion, and meet ongoing working capital requirements. The deal is secured with an assignment of contracts, mortgage over vessels, with a low investment-to-value ratio. The deal has covenants and credit enhancements which include a cash sweep. The Ijarah is structured to facilitate an uncommitted line to future capital expenditures and business expansion.

Honorable Mention: CityCentreDC; Astra Sedaya Finance; and Saudi ARAMCO Mobile Refinery.

Many interesting Sukuk deals were delivered to the market in 2013: DanaInfra with the first retail Sukuk in Malaysia; Malaysia Building Society; Saudi Electricity Company; Osun Sukuk; Bank Asya; Ooredoo; Sadara; and Sime Darby all represent important landmarks in the Sukuk market either on the global or national level. But, the long-awaited International Islamic Liquidity Management Corporation (IILM) Sukuk program offering investment grade tradable Sukuk is the Sukuk deal of the year. IILM delivers instruments which facilitate effective cross-border Islamic liquidity management and qualify as high quality investments for Basel III purposes.

Honorable Mention: DanaInfra Nasional, Malaysia Building Society; Saudi Electricity Company; Osun Sukuk; Bank Asya; Ooredoo; Sadara; and Sime Darby.

Several private equity deals were nominated including Alkhabeer’s Express Publishing & Investment which demonstrates the emergence of generational change in many UAE businesses founded by South Asian entrepreneurs; and RHB Investment Bank’s Weststar Aviation Services which brought Kohlberg Kravis & Roberts (KKR) into the Islamic ambit for a Malaysian deal. Al Noor Hospital’s London Stock Exchange (LSE) listing was also notable. But, BIMB Holding’s is perhaps notable for its strategic achievement.

BIMB Holdings supplemented the Rights and Warrants issues with a 10-year Tawarruq securities issuance of RM1.66 billion (US$505.04 million) (nominal value). The proceeds of the issuances were applied to allow BIMB Holdings to acquire the remaining 49% of issued and paid-up share capital of Bank Islam from Dubai Financial Group (30.47% of the issued and paid-up share capital of Bank Islam for a cash consideration of US$550 million and from Lembaga Tabung Haji (18.53% of the issued and paid-up share capital of Bank Islam) for a cash consideration equivalent to US$334.6 million (payment was in Malaysian ringgit). The remaining funds covered the cost of executing the transactions and provided additional working capital requirements for BIMB Holdings.

The overall structure was designed to optimize the capital structure of BIMB Holdings and achieve the correct combination of equity and debt. The transaction is structured with covenants to ensure transparency and protection of investor’s rights.

This deal was the largest fund raising exercise via Rights Issue with Warrants in the Malaysian financial sector in 2013. The deal was also the largest such transaction for a publically listed company in Malaysia. The key outcome of the deal is the independence of Bank Islam.

Honorable Mention: Al Noor Hospitals Group; Express Publishing & Investment; and Weststar Aviation Services.

Some deals of the year are notable for size, others for sound execution of the basics. Certainly, Saudi Electricity Company, Kimanis Power and Telekom Malaysia all had mega deals in the market. Both Tilal Development Company (Modern Sukuk Company) and Osun Sukuk represented the opening of new markets. Meezan Bank, however, often sticks to the simple and clear application of basic principles to serve their customers.

Meezan structured the operating finance lease to enable Siemens Pakistan to continue enjoying the benefit of the leased assets. Simultaneously, the transaction took the assets off of Siemens Pakistan’s balance sheet in the local reporting of financial statements done in accordance with IFAS, and to keep both assets and related financing off balance sheet under International Accounting Standards followed by the company for its group reporting purposes. As a result, Siemens Pakistan unlocked cash without increasing financial leverage on its balance sheet.

Honorable Mention: Tilal Development Company through Modern Sukuk Company; Telekom Malaysia; Kimanis Power; Osun Sukuk; and Saudi Electricity Company.

As expected the project finance and infrastructure markets are extremely important in the Islamic finance field. CityCentreDC, Kimanis Power, and Deyar Al Balad were all very important and distinct projects. The first represented the largest ever Istisnah construction financing in the US. The second is a major Malaysian Ijarah-based project financing. And Deyar Al Balad is a smaller Saudi public private partnership real estate development in Makkah. The Sadara Basic Services Company Sukuk forms part of a US$20 billion multi-source project financing for the construction of a chemical facility in Saudi Arabia. The project, when constructed, will be one of the world’s largest integrated chemical facilities. It will be the largest ever built in a single phase. Sadara incorporates complex inter-financier issues, ECA issues, and validation of the newly promulgated, but not yet, in force Saudi Arabian Sukuk rules.

Listed on Tadawul, the Saudi Arabian Stock Exchange, Sadara is only the second Sukuk to be approved under new rules. The structure is declining Musharakah with a project Istisnah and Ijarah for pre and post-occupation of the Islamic assets. The profit and principal payable under the Sukuk are funded by the underlying forward lease rentals during construction and actual lease rentals post-construction of the project assets. The Musharakah ensures that the Sukuk are tradable even during the construction period.

The transaction is particularly notable as the sponsors (Saudi Aramco and Dow Chemical) wanted to issue the project Sukuk reasonably early on in the overall financing timeline — in particular, the Sukuk was to be issued prior to the signing of the wider financing, which presented some unique challenges. A regime was required that would allow the Sukuk to be issued, yet also allow certain aspects of the inter-creditor arrangements to continue to be negotiated with the ECAs and the lenders, without having to consult the holders of the Sukuk. The consent regime needed to be robust enough to keep the Sukukholders comfortable, but flexible enough to accommodate the continuing discussions with the conventional lenders and the ECAs. The transaction also saw a number of enhancements to the structure used on the preceding Saudi Arabian project Sukuk for SATORP. Foremost among these was the introduction of a new special purpose entity to act as an ‘authorized agent’ on behalf of Sadara in its various capacities as lessee and procurement contractor.

Honorable Mention: CityCentreDC; Kimanis Power; and Deyar Al Balad.

This was a light year for IPO nominations. UMW Oil & Gas Corporation was a major transaction in Malaysia resulting in a new Islamic stock offering under the Securities Commission’s new criteria. DAMAC was also a significant event in the UAE. Noor Hospitals, however, brings a unique flavor to the IPO segment.

Al Noor Hospitals Group took advantage of its GBP221 million IPO to restructure its Abu Dhabi operations. Proceeds of the IPO funded the acquisition of a specialty center and a group of medical centers for US$50 million; the expansion of existing facilities at Khalifa Hospital and the continued development of new medical centers in Abu Dhabi; and to support the group’s entry into other key emirates.

An eye-catching reality is that Al Noor listed, not in the UAE or MENA region, not in Malaysia, but on the LSE. The shareholding structure involves a Mudarabah arrangement which allows UK investors to acquire an interest in the Issuer’s principal limited liability company, incorporated in the UAE, in a manner that maximizes foreign control in such company while, at the same time, respecting the fundamental UAE laws relating to (a) foreign ownership; and (b) anti-fronting. The Mudarabah structure incorporates complex shareholder arrangements to ensure that close to 100% of the economic benefits in the issuer’s local UAE company indirectly revert to the issuer. The structure was rigorously tested by the UK Listing Authority before it was approved for purposes of the IPO. The structure may be replicable to allow UAE companies to seek international liquidity by listing on a foreign exchange.

Honorable Mention: UMW Oil & Gas Corporation and DAMAC Real Estate Development.

2013 saw many mega Mudarabah deals including Dana Gas; GEMS Education; Dubai Islamic Bank; and Arcapita Investment Holdings restructuring. Abu Dhabi Islamic Bank — Egypt (ADIB Egypt) was not the largest, but it was executed in difficult circumstances and applied a novel structure to purpose for which conventional banks are often quick to act with fine pricing.

The ADIB Egypt structure relates to the issuance of letters of credit and their prospective refinance through restricted a Mudarabah finance facility. The deal was executed for sight and usuance letters of credit up to US$110 million in favor of East Delta Electricity Production Company for the importation of spare parts for the production facility stations. The facility covers a five-year base stock supply. The Mudarabah facilities were priced at profit sharing ratio reflecting a pre-agreed margin above the mid-corridor rate as announced by the Central Bank of Egypt. The Mudarabah facility has a term of four years and funds in Egyptian pounds up to 85% of goods under the letter of credit documents. The deal is guaranteed by the Egyptian Electricity Holding Company.

The transaction is the first corporate finance Mudarabah of its type deal in Egypt, and the first Shariah compliant syndication for a major Egyptian public energy sector entity. In addition to its Islamic finance benefits, the financing supported a strategic sector at a time where power outages were frequently affecting the industrial and commercial sectors and the daily life of every Egyptian. The financing prospectively helps the obligor to provide electricity in seven strategic governorates.

Honorable Mention: Dana Gas; GEMS Education; Dubai Islamic Bank; and Arcapita Investment Holdings.

Normally, our Murabahah class does not encompass Tawarruq as we wish for the category to reflect the true movement of goods between parties. This year, many of the true trade finance deals incorporated Tawarruq. The Mobily US$645 million deal with northern Europe ECAs highlights the importance of cross-border trade with non-Muslim countries. This transaction follows SEK’s prior deal for Saudi Telecom’s Indonesian subsidiary. The Mobily deal was disbursed in two tranches backed by the Swedish and Finnish export agencies. The first of US$320.85 million was a Murabahah facility with the support of Sweden’s Exportkreditnämnden for the purchase of eligible goods and services from Ericsson AB. The second was a US$325 million Murabahah facility with the support of Finnvera, for the purchase of eligible goods and services from Nokia Siemens Tietoliikenne Oy. Each deal provides long-term low cost fixed rate financing to Mobily on terms which cannot be found in commercial banking market. The proceeds help fund Mobily’s capex development plan. Although Mobily could have been contemplated as a true trade Murabahah, the counterparties preferred the flexibilities that Tawarruq would provide including the facilitating of multiple tranches.

For Finnvera the deal represented a number of firsts: its first Islamic deal, its largest deal ever in Saudi Arabia and its largest ever deal in the Middle East.

Honorable Mention: Trading Corporation of Pakistan; Turk-Eximbank; Abu Dhabi Equity Partners; and Bahra Advanced Cable Manufacturing Co.

The Musharakah category was also hotly contested with the competition spilling into the perpetual category. Each of Malaysia Airports Holdings Berhad, UMW Holdings, Pandu Logistics, and Sadara Chemical Company had an offering with strong merits.

SP Setia is a public-listed company and a prominent property developer. The company is constantly increasing its land bank as well as developing townships. Given the nature of the real estate business, SP Setia requires long-term funding. As a public company, SP Setia has to consider the issues relating to dilution if it issued new shares.

Given the lack of favor that real estate is currently suffering, and the Basel III impact on long-term project financing, SP Setia’s Sukuk Musharakah program addresses the key issues facing the company and helps it to stand out in a large crowd.

This Sukuk Musharakah is a perpetual Sukuk, combining Musharakah and Musawwamah, to be issued by a Malaysian public-listed company in the property sector. The issuance has no fixed tenure or maturity date, but it does incorporate a step up feature after the fifth year. The Sukuk Musharakah was structured to be classified as equity in the financial statements of the issuer while having common features of a fixed income instrument such as a periodic distribution to investors thanks to the Musawwamah element.

The net proceeds arising from the issuance of the deal will be utilized towards the deal expenses, purchase of lands, buildings and property; and development and construction costs and working capital of existing and future projects; as well as the issuer’s working capital. The issuance allows SP Setia to tap a large pool of funds without increasing its debt to equity ratio. As a result, the company preserves financing capacity in the broader market.

The securities are not convertible to any class of the Issuer’s ordinary shares avoiding dilution of the existing shareholders of the Issuer.

Honorable Mention: Malaysia Airports Holdings Berhad; UMW Holdings; Pandu Logistics; and Sadara.

Perpetuals became the flavor of the year in 2013 with the form moving into the corporate, education, and real estate sectors. Al Marai Company as the largest integrated dairy company in the MENA region issued, as did GEMS Education, one of the largest education firms in the GCC. But, property is the most challenging business segment in which to attract funding. Given the success of publically listed real estate developer SP Setia to launch its RM700 million program allows them to top the very well-noted competition.

Honorable Mention: GEMS Education; Al Marai Company; and Dubai Islamic Bank.

As always, real estate is a deeply desired investment for Muslim investors. This year’s nominations included a number of interesting deals. Deyar Al Balad was proposed a Makkan public private partnership for real estate development. The SAR4.3 billion (US$1.14 billion) Arabian Centers Company was the largest financing for a private sector company in Saudi Arabia. DLA Piper nominated Alkhabeer’s Park 10 US acquisition, which applied the well-tried master sub-lease structure for real estate acquisition. CityCentreDC, however, is a landmark. It is the largest ever domestic US Islamic real estate financing for GCC investors.It is one thing to build on Key Bank’s 2002 authorization to use Istisnah and another to craft suitable tax-friendly documentation. The process took nearly 18 months after selection of JPMorgan Chase to lead the financing syndicate which including many leading US banks. The project itself is a major urban redevelopment project in the US capital. Composed of multiple office and residential buildings, the project is a short walk from the Capitol Building, sporting arenas, and the convention center.

Honorable Mention: Deyar Al Balad; Arabian Centers Company; and Park 10.

Tawarruq, often termed commodity Murabahah, is the process of generating cash or financing from a series of sales transactions, typically involving four counter-parties. Albaraka Turk Participation Bank used the structure to issue non-tradable Sukuk as part of its regulatory capital structure. BIMB Holdings incorporated Tawarruq into its shareholder buyout. Malaysia’s Cagamas and Perbadanan Tabung Pendidikan Tinggi Nasional also achieved successful large-scale Tawarruq transactions. Maran Nakilat jumps ahead of the crew for its various characteristics. The transaction finances two LNG which are contracted to for Ras Gas and British Gas through its own vessels. Maran Nakilat is the first ever Islamic vessel financing transaction for a Greek company (co-owned by Qatar’s Nakilat). The five-year deal has an extension option for a further five years which also allows for re-sizing of the facility. One reason that Tawarruq is often preferred for shipping finance is that it facilitates the use of shipping mortgages which are well understood in the global market, and it allows financing without ownership risk. In the hydrocarbon sector, ownership risk often extends to carrying the liability for pollution.

Honorable Mention: Albaraka Turk Participation Bank; BIMB Holdings; Cagamas; and Perbadanan Tabung Pendidikan Tinggi Nasional.

Although a number of clever structures were nominated for the Structured Finance Deal of the Year, the MBSB deal is the first covered Sukuk transaction in the Islamic housing finance sector. Tamweel PJSC and others have issued asset-backed securities. But, with the growing Basel III challenges, many Islamic banks operate in jurisdictions in which securitization is not easy, not possible. Leave it to the Malaysians to pioneer a model for which is replicable and may be adjusted to other markets. A key distinction in this deal is that unlike many covered deals in the MENA region, the investors are legally able to access the ‘cover’ to satisfy their claims. Most earlier deals in the MENA region are asset-light and the Sukukholders cannot make claims on the underliers.

MBSB is a key provider of personal financing facilities for civil servants in Malaysia. The institution is seen as very secure as almost all repayments (99%) collected through salary-deduction schemes. Funding in this deal is provided through Tawarruq creating a direct claim against MBSB. The pool of receivables transferred to the guarantor SPV give a second avenue to cover the financial claims of the Sukukholders from a dedicated pool of identified Islamic personal financing receivables which are ring fenced in the bankruptcy remote SPV.

Honorable Mention: International Islamic Liquidity Management Corporation; Univers Acier; Telekom Malaysia; and KDU University College.

Honorable Mention: Trading Corporation of Pakistan; Turk-Eximbank; Abu Dhabi Equity Partners; and Bahra Advanced Cable Manufacturing Co.

Although there were many large and well publicized Wakalah deals, the Astra Sedaya Finance transaction was an intriguing cross-border deal allowing 3.5-year tenors (inclusive of six months of availability period). The deal, availed in US dollars, was the first syndicated Wakalah financing in Indonesia. Supporting the auto finance business of Astra Internasional, the deal provides a means for participation in the underlying installment sales and leasing contracts of Astra Sedaya Finance.

Honorable Mention: Abu Dhabi Equity Partners; Al-Mourjan For Electricity Production Company (Rabigh 2 IPP); Emirates Airlines; Ooredoo; and PIA.

Fulfillment of the African promise is slow. In 2013, only a few African nominees emerged. ITFC structured a revolving trade facility for Morocco’s Univers Acier, freeing cash during the trade cycle for the Moroccan steel maker. The winner of the Mudarabah Deal of the Year, East Delta Electricity Production Company pulled together an innovative syndication during difficult times. But, in Nigeria, Lotus Capital pulled together the first sub-sovereign issuance applying the new Nigerian ‘non-interest’ capital markets framework. This is also the first sub-Saharan sub-state sovereign deal. Based on the strength of the product and the opening of the market, Osun Sukuk is the African Deal of the Year.

The 14.75% fixed return Sukuk Ijarah due in 2020 supports the construction of 23 high schools, two middle schools and two elementary schools across Osun State. The Sukuk are guaranteed by the government of Osun State. The deal won widespread support from the full Nigerian financial market community with almost all domestic investment banks acting as co-underwriters and almost all banks, conventional and non-interest buying the Sukuk. As the first sub-sovereign Sukuk in sub-Saharan Africa the deal went well despite the challenging regulatory and legal framework environment. The Sukuk were oversubscribed notwithstanding their novelty. Lotus Capital rightly takes pride that the deal was completed successfully and efficiently with Nigerian talent doing the heavy lifting and no international underwriters or structuring agents.

Honorable Mention: East Delta Electricity Production Company (Egypt) and Univers Acier (Morocco).

In a year of ongoing European malaise and anemic UK growth, the deals of the year flow was light for the UK and Europe in general. BLME continued their niche real estate business with new competition. LTH deserves merit for facilitating Tabung Haji’s leveraging of UK real estate.

Up until now the theme has been real estate and Tawarruq. As a result, the FWU-sponsored Sukuk Wakalah Salam III stood out as innovative. The investment-grade sponsor delivered the Sukuk through its subsidiary Atlanticlux, Luxembourg.

The first of three tranches was US$20 million and closed in October 2013. Two more tranches are planned. The Sukuk appoint the issuer to invest in the re-Takaful business and its permissible activities. This frees cash for the sponsor to pay commissions to its agents. The deal is highly collateralized by the sponsor’s underlying Shariah compliant cash flows.

The US$100 million Murabahah facility from AK BARS Bank represents an exciting new step in the continuing development of the Islamic finance industry in Russia. The geographic diversity of investors demonstrates the high level of global interest in this nascent market; and the significant oversubscription establishes AK BARS Bank as a leading proponent of Shariah compliant finance in the CIS region.

Honorable Mention: Somerset Place, LTH and AK Bars

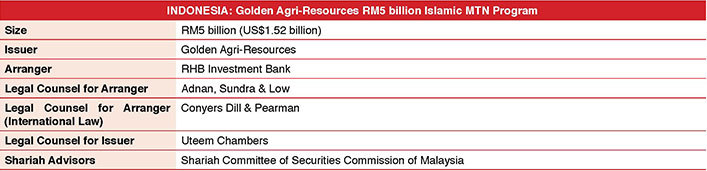

Indonesia had a limited number of nominations for 2013. Golden Agri was the largest Malaysian ringgit-denominated issue by a foreign issuer in the Malaysian debt market. Golden Agri is the world’s second-largest palm oil plantation company and the largest in Indonesia. The Sukuk program gives Golden Agri access to US dollar funding at competitive pricing through cross-currency swaps in a volatile environment.

Honorable Mention: Astra Sedaya and Pandu Logistics

Kuwait is only now fully emerging from the financial crisis. Many investment companies are refocusing their businesses, which is the essence of Noor Investment Bank’s exit from its investment in Pakistan’s Meezan Bank. Others like A’ayan Leasing and Investment Company have restructured. Al Kharafi won the project from the Directorate General of Civil Aviation for the Kuwait International Airport Expansion project (Phase II). In this project, Al Kharafi will be working on the administration building, car park and fire station. Dubai Islamic Bank, fronted by a Kuwaiti bank, is providing performance cover for Al Kharafi during the nine-month project period. The guarantees are covered by ‘escrowing’ of payments from the Directorate General of Civil Aviation Al Kharafi with a local bank in Kuwait; Notice of Assignment to transfer project proceeds to Dubai Islamic Bank (Amanat/collection account) from the project account with the Kuwaiti bank only in case of any outstanding claims under letter of guarantees and/or due payments under letter of credit and acceptances or any due payments under funded exposure; and acknowledgement, consent and undertaking on the Notice of Assignment from the Kuwaiti bank. Documenting and validating the security package was complicated.

Honorable Mention: Noor Investment Bank sale of shares in Meezan and A’ayan Leasing and Investment Company.

The Malaysian Sukuk market is the most vibrant and active Sukuk market. As a result, selecting Malaysia’s deal of the year is never easy. With deals like BIMB Holdings, Malaysia Building Society, S P Setia, and Malaysia Airports Holdings, the competition was crowded at the top. As always, Malaysia breaks new ground, despite the achievements of the other deals, DanaInfra’s first ever exchange traded Sukuk successfully created a new asset class for retail investors. By reaching beyond institutional investors, high net worth individuals, and financial institutions, DanaInfra’s retail Sukuk promises to bring greater liquidity to the Islamic capital markets by tapping the deeper pool of national savings. In light of this achievement, DanaInfra is the Malaysian Deal of the Year.

Honorable Mention: BIMB Holdings; Malaysia Building Society; S P Setia; and Malaysia Airports Holdings.

Many sovereign deals in 2013 were repeats of the same structures used by the same issuers. Little new ground was broken. Meezan Bank, Standard Chartered Bank Pakistan and Dubai Islamic Bank Pakistan provided advisory services to the Government of Pakistan (GoP) to enable it to raise funds in a Shariah compliant manner. The resultant Sukuk Ijarah issuances help to allow the establishment of a domestic benchmark. The transaction, which uses Pakistan’s M1 motorway as underlying asset, also serves the needs of the Islamic banking industry by enabling them to effectively manage their liquidity with a high quality liquid instruments. The Sukuk are issued through State Bank of Pakistan auctions.

Ooredoo is the security that many hope will generate more enthusiasm for state-linked and corporate Sukuk in the Qatari market. The Reg S deal is listed on the Irish Stock Exchange and was very well received, being oversubscribed four times. The Sukuk program utilizes airtime as the underlying asset. This inaugural issuance was through Ooredoo Tamweel, a Cayman Islands SPV wholly-owned by Ooredoo (the trustee), of US$1.25 billion trust certificates due 2018. The program utilizes a Manafae structure, conferring on the certificateholders the right to receive income arising from the sale by Ooredoo to the trustee of minutes of airtime on Ooredoo’s mobile telecommunications network and the distribution thereof by Ooredoo to its customers. The use of the telecom airtime minutes instead of property assets, for example, to underpin the Sukuk, provides Ooredoo the opportunity to use a much larger pool of available assets and thus issue on a regular basis in future. The development of the Sukuk structure also required the cooperation and interaction with the Qatari telecommunications regulator because sale of airtime is a regulated activity in Qatar. The deal was Ooredoo’s first time issuing in the Islamic capital market. Previously, Ooredee had been a frequent conventional issuer.

Honorable Mention: Qatar Islamic Bank and Maran Nakilat Co.

Saudi Arabia is increasingly a sprint to compete with Malaysia in volume and variety in Islamic capital market transactions. In 2013, the volumes of syndicated deals and Islamic securities deals were also robust. Mobily’s Tawarruq facilities from the Finnish ECA, Finnvera, and the Swedish ECA, Exportkreditnämnden, GACA, Kemya, and Al Marai all provide strong claims for being the Saudi Arabian deal of the year. But, Sadara grabs the lead by refining the SATORP structure and applying the anticipated new Sukuk rules. With the help of the Sadara Basic Services Company Sukuk, more structure is delivered to the Saudi Arabian market, and a template for asset-rich corporates and real estate companies is defined. Sadara also must do so while managing complex inter-financier issues and export credit agency requirements for the overall project. The tradable Sukuk are listed on Tadawul.

Honorable Mention: GACA; Kemya; Mobily; and Al Marai Company

The Turkish market performed well again in 2013. The participation banks improved their regulatory capital, and the republic returned to the market with a successful offering. A key part of the Turkish success story over the past 10 years has been trade finance. The ITFC has been playing an important role in the expansion of Islamic trade finance tools. The ITFC has successfully delivered its two-step Murabahah products throughout the Islamic Development Bank (IDB)’s footprint. The tool has generally been used for import finance. With the Turk-Eximbank, the ITFC applied the concept for export finance. Under the export structure, the ITFC purchases the goods from exporters upon presentation of proof of exports, via export declaration forms. The ITFC then sells the goods on to Turk-Eximbank which has assignment of the ITFC’s receivables from exporters.

Honorable Mention: Albaraka Türk Katılım Bankası; and Bank Asya.

The markets ended 2012 feeling that something extraordinary was happening in Dubai. Business indicators showed more than recovery. Yet, concerns remained about the emirate itself: would it be able to reposition itself into an ever better position? For the government of Dubai, other issues were at stake including the establishment of its yield curve and a benchmark of investor confidence. The deal was executed swiftly, delivering attractive pricing on the unrated 10-year Reg S Sukuk. This buoyed and continues to support growing confidence in the emirate. The transaction was over subscribed by 12 times, a clearly supportive voice from the market, and a very good way to start the campaign to establish Dubai as a capital of the Islamic economy.

Honorable Mention: Al Noor Hospitals; Dubai Islamic Bank; Gulf Marine Services; GEMS Eductaion; and Emirates Airlines.

For a number of years, Bank of London and The Middle East (BLME) held up the Union Jack flag. They return with the Somerset Place deal which is the first redevelopment of an entire Georgian Grade I listed property. On the continent, FWU also led the charge with the second-ever European Sukuk in 2012. In 2013, FWU delivered more innovation to the market with market with a premium linked Sukuk product. On the one hand, the innovation will require more market investigation of the concepts applied. On the other hand, the Tabung Haji as sponsor of LTH Property Holdings used a tried and true method to overcome challenges relating to tax and jurisdiction.

In order to leverage two central London properties, LTH Property Holdings applied Tawarruq to fund clients’ investment in two central London properties. The facility involves multiple jurisdictions including Malaysia, Jersey (Channel Islands) and the UK.

Honorable Mention: Somerset Place and Atlanticlux Lebensversicherung.