The strong appeal for Sukuk lies in its value proposition. For issuers, Sukuk offers the opportunity to tap an enlarged investor base with strong demand for Shariah compliant investments, while investors benefit from portfolio-diversification opportunities and investment options in a fast-growing fixed-income asset class. The tipping point centers on costs competitiveness which encompasses issuance costs and the time to market for Sukuk. RUSLENA RAMLI writes.

In Malaysia, to encourage the private sector (or corporate issuers) to play a significant role in the development of the bond market (both Sukuk and conventional bonds) concerted efforts were undertaken by the government and regulators. Several fiscal and financial incentives were introduced, including a tax-neutral framework and tax deductions of issuance expenses on qualified Islamic securities. As a result, Malaysia has become the world’s largest Sukuk market historically contributing more than 50% to total global Sukuk issuance with the corporate sector representing on average of 30% of the total. The balance of issuance comprises approximately 40% of Bank Negara Malaysia (BNM)’s Islamic securities, 20% from the government and 10% from quasi-government issuance.

In analysing the growth of the Malaysian Sukuk market, the barometer of performance is better depicted by zooming in on the issuance trends from the corporate sector instead of the total Sukuk market data. This headline number could include large issuances of BNM’s Islamic securities designed as a market liquidity instrument, which could sometimes obscure the underlying Sukuk market issuance trends.

Review of 2015

Over the past 25 years, RAM Ratings’s rated portfolio of private debt securities (PDS) grew to US$262.4 billion as at September 2015. From the total, US$125 billion or 48% represent Sukuk issuance which includes many pioneer structures that have contributed to the breadth and diversity of Sukuk products in the Malaysian bond market. In 2015, RAM Ratings’s rated portfolio of foreign entities expanded to include Turkey’s largest Islamic bank, Kuveyt Turk Katilim Bankasi’s RM2 billion (US$453.36 million) Sukuk Wakalah program to be issued through its funding conduit, Kira Sertifikalari Varlik Kiralama. To date, RAM Ratings’s portfolio of foreign issuers and/or related credit assessments include 26 foreign entities across 14 countries. While market conditions still dictate the decision to issue and the timing of issuance, the success of attracting cross-border Sukuk issuance was largely driven by Malaysia’s strong regulatory drive as well as having a supportive tax and legal framework.

Following the introduction of Malaysia’s sustainable and responsible investment Sukuk (SRI) guidelines in August 2014, Khazanah National (Khazanah) was the first corporate to take up the government’s call by putting in place a RM1 billion (US$226.68 million) SRI Sukuk program. The first RM100 million (US$22.67 million) seven-year tranche was successfully issued in June 2015 and fully subscribed by a diverse investor group including foundations, corporations, banks, pension funds and asset management companies (based on Khazanah’s press release dated the 4th June 2015, ‘Khazanah issues world’s first ringgit-denominated sustainable and responsible investment Sukuk’). The assigned AAA-rating by RAM Ratings reflects the credit strength of Khazanah as the ultimate obligor to the financing structure. Other notable issuances include infrastructure and utility companies that have raised Sukuk to fund its ongoing infrastructure projects and/or refinance existing borrowings as well as Islamic financial institutions tapping the Sukuk market to meet its capital requirements.

In light of the economic slowdown affecting the Malaysian economy in tandem with the ringgit’s depreciation, RAM Ratings had stress-tested its rated portfolio of companies. The analysis concluded that the stress test had exerted minimal impact on the credit profiles of the companies. Even though foreign-currency debts form a large proportion of the debt profiles (ie about half of the rated corporates), the downside risks were mitigated by the natural hedge in the form of foreign-currency assets and/or earnings while credit quality (ie 90% of RAM Ratings-rated issuers are rated ‘AA’ and above) are supported by moderate leverage and strong liquidity.

Preview of 2016

Following the Malaysian 2016 budget announced in October 2015, the extension of tax deduction on the issuance cost of qualified Islamic securities as well as SRI Sukuk was accorded in line with the government’s aspirations to turn the nation into a global Islamic financial center. This, coupled with current market conditions where demand outstrips supply for Sukuk, has led to the trajectory issuance of corporate Sukuk to remain above the 50% mark of total corporate bond issuance. In promoting innovative structures, the SRI Sukuk issued by Khazanah became a landmark issuance and has propelled Malaysia ahead of the curve in encouraging the development of a new asset class that has a distinctive feature not comparable to conventional bonds. With the stimulus provided for SRI Sukuk in projects such as wind, solar power generation or affordable housing, the government has remained steadfast in encouraging the private sector to play a prominent role in the years ahead.

Conclusion

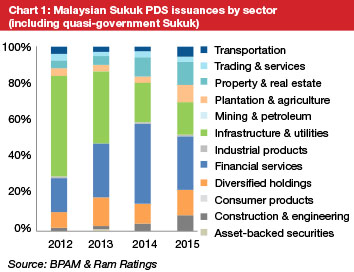

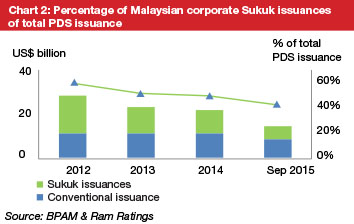

The Malaysian corporate Sukuk market is expected to show resilience with key sectors to remain dominated by infrastructure and utilities as well as financial services. RAM Ratings had, in June 2015, revised its projected gross PDS issuance downward to around US$18-20 billion (based on RAM Ratings’s press release dated the 16th June 2015, ‘RAM Ratings revises projected gross PDS issuance down to RM75-85 billion for 2015’) for 2015 due to mounting uncertainties that had affected market sentiment. As at September 2015, total PDS issuance reached US$14.5 billion, of which corporate Sukuk accounted for 43% or US$6.2 billion. Despite the headwinds, RAM Ratings expects potential infrastructure Sukuk issuance in the fourth quarter of 2015 to shore up total issuance to between US$8 billion and US$10 billion, which is still a respectable level given the challenging market conditions.

Sukuk issuance reaching the financial close will still be dependent on the ever-changing market conditions and sentiment. Nevertheless, the value proposition offered by the local Sukuk market (ie competitive pricing, tax incentives, ability to access the wide investor base, etc) shall continue to prevail in the funding transaction decisions of key market players.

Ruslena Ramli is the head of Islamic finance at RAM Rating Services. She can be contacted at [email protected].