According to the International Monetary Fund, Saudi Arabia’s GDP per capita in 2010 was US$16,257. Although it is much wealthier than Indonesia and Pakistan, it is much less wealthy on a per capita basis compared to its GCC neighbors. Kuwait’s GDP per capita in 2010 was US$37,009, the UAE was US$57,884 and Qatar was US$74,901. So wealth cannot be the only reason for the success of Saudi Arabia’s Islamic fund industry.

From our research, we have come to the conclusion that the relative success of the Islamic fund market in Saudi Arabia can be credited to four main factors:

1) The early launch of funds;

2) Strong government support;

3) A high percentage of high net worth individuals; and

4) Extensive branch distribution networks.

1) Early launch of funds

Funds as investment vehicles are still new in much of the emerging and frontier markets. In the Islamic market, Saudi Arabia was one of the first countries to introduce funds. The first Islamic funds in the form of short-term Murabahah (or money market instruments) and equity funds appeared in Saudi Arabia around 1992. It wasn’t until the later part of the 1990s when funds spread to other neighboring countries.

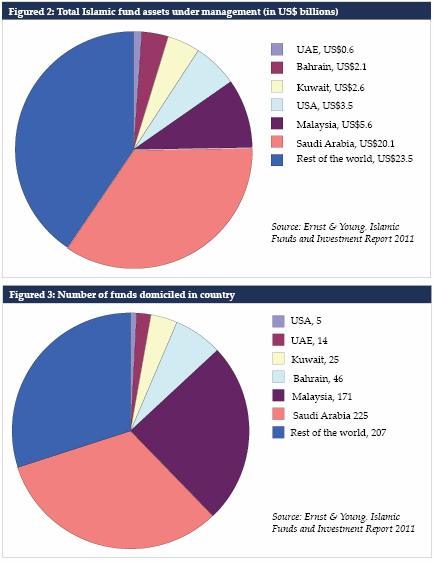

Investors seem by now to have accepted funds as an investment vehicle. Over the two decades following their introduction, total fund assets domiciled in Saudi Arabia have reached US$20 billion. In addition, many of the Islamic funds domiciled in offshore centers such as Luxembourg and Ireland were also set up by Saudi institutions or western institutions targeting Saudi and other GCC investors. The number of funds has grown from an estimated 40 in 1996 to an estimated 693 in 2011. Saudi Arabia accounts for over one third of all assets in Islamic funds worldwide. Assets of Islamic funds in the UAE in contrast account for only 1% of the market. Bahrain, which has long been the banking center of the GCC, makes up less than 4% of all assets in the market.

Early entry to the market is therefore clearly only part of the answer as to why Saudi Arabia dominates; as otherwise Bahrain would have a larger share of the market as it was also one of the first to enter the fund space.

2) Government support

Flush with petro-dollars from the 1970s, the Saudi government realized early on that it needed to develop the wealth of its citizens and offer them local investment opportunities. As a result of limited investment opportunities at home, the Saudi government and its citizens were forced to look outside the country to park their new wealth. Much of this wealth ended up in Europe and the US and the term ‘petrodollar’ was used to explain this phenomenon.

In the 1970s, the Saudi government spent a considerable amount of wealth developing the country’s infrastructure: building roads, airports, ports, hospitals and schools. It also promoted the development of industries, such as petrochemicals, manufacturing and even farming. This helped build a diversified economic base.

With the government focused on building up its economic base, it fell short of developing financial institutions. It wasn’t until the late 1970s that the push to develop the banking sector took off. Saudi Arabia has had foreign entities active in its financial sector since 1926, when it allowed the Netherlands Trading Society to set up a branch in the country in order to help finance the haj pilgrims coming from the Dutch East Indies (now Indonesia). For the most part, the financial sector was closed off to foreign institutions. However, with the country developing rapidly, the government allowed foreign institutions to participate in developing the Saudi banking and finance sector by forming joint venture banks. Foreign banks could form a minority joint venture with Saudi investors. This was a success, as foreign banks got the chance to participate in the lucrative Saudi financial sector and Saudi Arabia got foreign expertise in developing its financial system. Some of the key joint venture banks set up during this time were the Saudi Hollandi Bank (ABN AMRO) in 1969; the Saudi Fransi Bank (Credit Agricole S.A.) in 1977; the Saudi British Bank (HSBC) in 1978; and the Saudi American Bank (Citibank) in 1980.

These banks grew rapidly as they helped finance the Saudi government’s vast projects. They also pushed ahead to develop the retail banking sector, and today Saudi Arabia boasts one of the most sophisticated retail banking sectors in the Middle East. The government also pushed for the establishment of the Saudi Arabian Monetary Agency (SAMA) in 1984 to regulate the informal stock exchange, now known as Tadawul. The Saudi exchange is the largest stock market in the Middle East with a market capitalization of over $325 billion.

3) High percentage of high net worth individuals

According to the Credit Suisse Global Wealth Report 2011, Saudi Arabia has over 44,000 millionaires, and this is expected to grow by 45% over the next five years to 64,000. The UAE holds the number two slot in the Middle East with 40,000 millionaires, followed by Kuwait with 31,000. The higher concentration of wealth in the country can also be attributed to the growth of the fund market.

4) Bank distribution networks

There are only 11 banks currently operating in the country and a large area to cover. This helps explain why some of these banks have hundreds of branches. Al-Rajhi Bank, which was formed in 1978 as a currency exchange and trading company, is considered to be the first Islamic bank in Saudi Arabia. It has over 466 branches and was the first to launch an Islamic fund in 1992. Like many other banks in the country, its vast distribution networks have been a leading factor in the increasing popularity of Islamic funds. Not only does Saudi Arabia have the largest number of funds, the funds are larger in terms of assets under management than funds domiciled in other countries. This is a clear sign that Saudi banks are able to attract assets to their funds.

Not everything is so positive

For all the success of the Saudi fund market, there are still some issues that are holding it back from reaching its full potential. Legal and regulatory issues aside, there are two key issues affecting the market: 1) Investor psychology, and 2) Restrictions on foreign investors.

For centuries the Middle East has had a strong trading culture, which has continued through modern times. However, due to the petro-wealth of the governments in the GCC, expensive welfares states have developed. Though there are many positive aspects of this, there are also negative side-effects, one of which is the lack of a savings culture. There is little incentive to save or invest for the long-term if you know that the government has a comfortable retirement plan waiting for you down the road. Thus, speculation and trading are in and savings are out.

On the other hand, foreign investors are not allowed to invest directly in publicly traded companies. This is why we have had to construct two versions of our indexes for the Middle East: one version for local investors and another version for foreign investors – the Dow Jones Islamic Market GCC Index with and without Saudi Arabia. Saudi Arabia is not the only country that restricts foreign investors in the GCC. Kuwait and the UAE both have some restrictions. It is only in the last two years that the restriction has been modified in Saudi Arabia to allow foreigners to participate via fund vehicles. The success so far has been limited.

Final words

Saudi Arabia became the largest Islamic fund market because it allowed the establishment of funds early on. It also had strong government support backing up its financial services industry coupled with a large number of high net worth individuals. However, a key factor to this success has been the vast distribution networks of banks in the country. This not only allowed its banks to offer a wide range of investment products, it also insured that these products would be supported by a strong asset base.

Tariq Al-Rifai is the director of Islamic Market Indexes at Dow Jones Indexes and he can be contacted at

[email protected]

.