Xav Feng discusses the intricacies of rating a fund using Lipper’s methodology, explaining that it deals with much more than merely performance.

In a world where information is readily available at our fingertips, we can easily read about people’s experiences. In the world of gastronomy we can read opinions from food critics and refer to the famous Michelin star system for a rating of a dining experience at a particular restaurant.

Mutual funds have existed for a long time as investment vehicles for the man in the street as well as for the investor seeking to capitalize on global investment themes.

There are thousands upon thousands of funds out there, many of them with similar investment objectives, and many of them that fill niche investment areas. While investors may be interested in investing in emerging market equities, for example, it is still often a daunting task to decide which particular fund is the most suitable. This is why a comprehensive fund rating system is so important.

Performance is not everything

When looking at a particular mutual fund product for the first time, the would-be investor might look at tables and graphs depicting the performance of the fund. However, as in all marketing materials, the good periods of performance are often played up, while periods when the fund did not perform as well may be downplayed (or omitted). Secondly, while past performance is not indicative of future performance, it is still true that a track record is extremely important, and investors want to be confident that a money manager has delivered in the past.

Investors who rate performance above all else tend to be the extremely aggressive sort – often choosing the fastest vehicle to get to their destination. For investors with a longer time horizon or who tend to buy into mutual funds at set intervals through regular investment plans, the historically best performing funds may not be the funds of choice.

Rather, these investors may want to look at how well the funds have preserved capital through market downturns or how consistently the funds have managed to outperform relative to their peers.

Investment jargon can be complicated

Fund managers and fund management companies often generate on an internal basis an array of financial ratios to compare their fund against the competition. There are Sharpe ratios, information ratios, and Jensen’s alpha; among other portfolio management ratios they examine internally.

Such information may be readily available to the retail investor in certain capital markets through the publication of monthly factsheets, or the information may be updated on the fund management company’s website – a good thing if the investor is sophisticated and savvy enough to understand what the information means.

However, for many individual investors these ratios are unintelligible; it’s too difficult to obtain and to understand these technical analyses.

Lipper Leader ratings system

As a professional fund data provider and fund research company, Lipper knows what most individual investors really need. Lipper created the Lipper Leader ratings system to help look at funds from different angles to meet investors’ needs. Most people invest in order to build wealth, and it is with this in mind that they look at the most popular metric: consistent return, which identifies funds that provide year-to-year consistency and risk-adjusted returns relative to all other funds in the same peer group.

The metrics that Lipper identifies as important to an investor are explained briefly below:

Total return: By rating funds purely for total return (which includes income from dividends and interest as well as capital appreciation), this particular Lipper Leaders rating identifies funds that have performed the best historically, without taking into account the risk the fund managers have taken. Investors who are aggressive and who are less concerned about downside risk often look at funds rated high for this particular metric.

Total return is defined as the return after (net of) expenses and includes reinvested dividends. Total return is commonly used to evaluate performance. Fund managers use it in conjunction with fundamental or quantitative analysis when choosing stocks, and individuals who engage in momentum investing frequently use total return as their primary screen.

Preservation: As people near retirement age or as their willingness to take risk decreases, the preservation metric is often used to identify funds that have demonstrated an ability to preserve capital over time across different market conditions, compared to other funds in the same peer group.

Investors who use the ratings system to identify such funds are often better able to minimize downside risk and preserve capital. Lipper scores for preservation reflect funds’ historical loss avoidance relative to other funds in the same asset class. The preservation model uses the sum of negative monthly returns over three, five, and ten-year performance periods.

Consistent return: One of the most popular metrics, consistent return combines the investment strategies of both return and risk tolerance, making it an extremely investor-centric rating, instead of just rating a fund based on its strategy or asset type. The consistent return metric simultaneously combines the fund’s performance and historical risk; it awards a rating based on these two factors relative to all other funds in the asset class.

Typically; the greater the risk, the greater the reward. The consistent return metric seeks to identify funds that have delivered the best returns with the lowest amount of risk taken. Lipper scores for consistent return reflect funds’ historical risk-adjusted returns relative to peers, measured in local currency. The consistent return measure is a richer risk-adjusted mutual fund return performance measure than others currently available in the marketplace.

It takes into account both short and long-term risk-adjusted performance relative to fund classification. The measure is based on the effective return computation. Effective return is a risk-adjusted return measure that looks back over a variety of holding periods (days, weeks, months, and/or years).

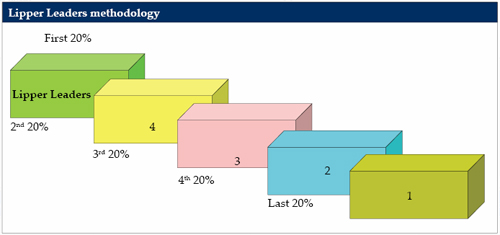

Lipper Leaders methodology

Only the funds that stand out in each type of metric are awarded Lipper Leader status. It is through careful comparison of each fund relative to others in the respective categories that the top 20% of funds in each category are awarded the Lipper Leader status for any particular metric. The highest 20% of funds in each peer group are named Lipper Leaders (5), the next 20% receive a score of 4, the middle 20% are scored 3, the next 20% are scored 2, and the lowest 20% are scored 1.

The scores are subject to change every month and are calculated for the following periods: three-year, five-year, ten-year, and overall. The overall calculation is based on an equal-weighted average of percentile ranks for each measure over the three, five, and ten-year periods (if applicable), and the scores help to provide context and perspective for investors who want to make their own investing decisions.

Using ratings objectively

Comparing the diverse number of funds in the market is not as simple as one would think; there are many similar funds that still use different strategies. Many investors make the cardinal mistake of comparing funds that are as dissimilar as apples and oranges.

Ratings systems help to provide a certain amount of context to help investors, but one cannot look at a ratings system only on the surface in order to make investment decisions. Certain types of mutual funds are inherently more volatile than others. A very volatile equity fund such as an emerging market equities fund that may have a very high rating under the preservation metric might still be more volatile than, say, a fund that invests in the equity of utility companies – historically more stable.

Conclusion

The Lipper Leaders fund rating system uses investor-centric criteria to identify the top funds in each category. Good funds will invariably get good ratings for these different criteria. Unlike depending on the taste of a film critic to make a decision about which movie to watch, the system allows the ultimate investing decision to lie with the investor.

Xav Feng is the head of Lipper Asia Pacific Research. He can be contacted at

[email protected]

.