For over two decades, the Kingdom of Bahrain led a strong base in the financial services and other non-oil sector services. And increasingly, young and well-educated people are engaged in boosting the pace of economic development in the country.

By all measures, the year 2015 was not as good as many industry analysts have anticipated. The GCC region has been faced with the challenges of budget deficits due to the sharp fall of oil prices. However, some of the major social infrastructure projects may go ahead with financing and constructions. Others may have to wait until global economy recovery materializes and oil and energy prices get back to better rates that generate enough income to finance projects in the GCC.

Evidently, growth in non-oil sectors of the GCC showed relative economic stability and helped consumer confidence. According to the Economic Development Board in Bahrain, the forecasted growth for the Kingdom’s non-oil sectors for 2015 was estimated at 4.6% and real GDP growth during the year at 3.6%. That is less than 1% (0.9%), also less than the previous year. Table 1 shows the changes of GDP growth between the year 2014 and forecasted growth for 2016.

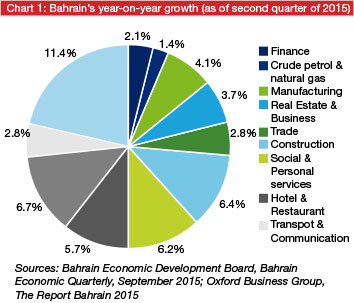

Bahrain’s transportation and communication sectors have been experiencing the greatest amount of year-on-year growth at 6.7% in the second quarter of 2015, followed by construction at 6.4%, and social and personal services at 6.2% (see Chart 1).

|

Table 1: GDP growth in 2014 and forecasted growth for 2016 |

|||

|

|

2014 |

2015 forecasted |

2016 forecasted |

|

Real GDP growth % |

4.5 |

3.6 |

3.2 |

|

Nominal GDP growth % |

2.9 |

-3.2 |

8.6 |

|

GDP (BD Billion) |

10.82 |

11.17 |

11.60 |

|

Consumer price index % |

2.8 |

3 |

3 |

|

Sources: Bahrain Economic Development Board, Bahrain Economic Quarterly, September 2015; Oxford Business Group, The Report Bahrain 2015 |

|||

Oxford Business Group reports that the country’s finance sector is one of its main economic drivers, with financial services constituting 25% of the country’s GDP. The energy sector continues to account for the majority of the government’s revenue; however, the proportion of GDP that it constitutes has recently been decreasing.

The regulatory environment

The Central Bank of Bahrain (CBB) continued to provide strong support to the financial industry which provides a significant percentage to the country’s GDP and economy as a whole. One of the recent initiatives in the Islamic finance space is that the CBB is currently working on providing a framework for Shariah governance of institutions offering Islamic financial services.

The proposed centralized Shariah Committee will organize and agree on practices that all institutions offering Islamic financial services in Bahrain should follow (as opposed to each institution having its own Shariah board to govern only their own products and services). This approach to harmonize practices of issues relating to Fatwas and Shariah operational practices is embraced in several countries around the world including, Malaysia, Pakistan and Sudan. By doing so, the CBB like other regulators aims to reduce the level of inconsistency in product offerings and Fatwas in the industry. As rightly reported by the CBB, the lack of uniformity in the past of service provisions has the potential to harm consumer confidence in the industry and may have customers questioning the belief as to whether these institutions are truly Shariah compliant. The CBB’s key objective is to have a comprehensive national approach to Shariah governance.

Other regulatory developments include the introduction of a new Islamic finance liquidity instrument which was based on the International Islamic Financial Market (IIFM)’s Wakalah Master Agreement. The instrument allows institutions offering Islamic financial services with excess liquidity to transfer these funds to the CBB and to have CBB invest the cash on their behalf.

Similarly, the Bahrain Bourse launched a new index in September, the Bahrain Islamic Index. The index shows the changes in the values of Shariah compliant securities and will list 17 different stocks.

In April 2015, the AAOIFI organized an outreach meeting with the International Accounting Standards Board to discuss strengthening their collaboration, specifically to support the financial reporting requirements the regulatory bodies require from institutions offering Islamic financial services.

The IIFM and the International Capital Market Association hosted a workshop in London which aimed to promote the IIFM’s release of their Master Collateralized Murabahah Agreement. The new standard provides new guidelines to institutions offering Islamic financial services to access liquidity that is collateralized using Sukuk and other Islamic securities.

The market practice front

Tamkeen, a Bahraini financial supporter of SMEs, has continued to partner with Islamic banks in Bahrain in order to ensure all its lending transactions are Shariah compliant. A key development was evident when Khaleeji Commercial Bank added BHD10 million (US$26.29 million) to Tamkeen’s portfolio to support the growth of SMEs. A similar initiative was taken by Ithmaar Bank which provided BHD10 million to Tamkeen’s joint portfolio to support this important niche market in the country.

Outlook for 2016

Looking to the future, the CBB remains consistent with its encouragement of the consolidation of Islamic banks in order to improve their strength in the industry as well as their ability to compete on a higher level. Consolidation coupled with the shift away from heavy investment in real estate will result in more resilient institutions that can cope in the face of economic downturns. There is great change and growth occurring in the worldwide Islamic finance industry and with the help of the CBB and this year’s developments, Bahrain appears to be moving in the right direction in order to further capitalize on the market.

However, it is important that the strong government policies and effective regulatory implementation, and the sound and friendly business infrastructure environment that the country enjoys should continue. Moreover, a focus on financial services and social and civic and human capital needs would drive further stability and growth in the Kingdom.

Dr Hatim El Tahir is the director of Islamic finance group, Islamic Finance Knowledge Center Leader, Deloitte & Touche – Bahrain. He can be contacted at [email protected].