When we talk about Islamic finance in Turkey (also commonly referred to as interest-free finance), participation banks come to mind. It is because participation banking focuses on interest-free financial products and services mainly based for production and asset financing, and also because these are the organizations that offer interest-free finance products in banking and other areas of finance. As a matter of fact, an interest-free banking license is given only to participation banks under current regulations AVSAR RADI SUNGURLU writes.

When we look at the participation banking sector which was founded in 1985, it can be seen that it has a market share of 5.2% in the total banking system as at the end of 2015 in terms of the total asset size. Despite the potential in Turkey, the sector has always been criticized for not showing a serious development in this market share for many years.

These sizes, of course, represent deposit banking, ie fund collection and disbursement. Given the other areas of finance, however the development of interest-free financing is unfortunately far behind. For example, in the field of investment banking and capital markets, the activity of participation banking has remained very limited.

However, interest-free finance and participation banking are in essence based on partnership, partnership financing and profit-loss sharing. This is the understanding that forms the basis of capital markets. In spite of this, participation banking in Turkey operates not based on partnerships such as Musharakah or Mudarabah, but works with a funding system that is predominantly based on ‘buy in advance/sell in terms’, ie Murabahah. There are similarities for interest-free capital market products in world applications. However, when we look at investment products and services, the market share of interest-free finance practice in Turkey falls well below 1%.

As a matter of fact, the situation of participation banking in general has been discussed in recent years and the government has taken the initiative to develop interest-free financing in Turkey to a certain extent as part of the Istanbul Finance Center Project. This is also why public participation banks are on the agenda. Ziraat Participation Bank and Vakif Participation Bank have started operations and Halk Participation Bank is planning to be active soon. The aim here is to bring dynamism to the sector with more competitive and fast-acting public players and thus increase the share of the sector. Of course, in order to be able to do this, it is necessary for new public players to concentrate on the growth of the sector with new products and services rather than on competition with existing ones, and to work on bringing foreign funds to Turkey with domestic project financing. Otherwise, this will not do much more than to break up the existing market. When it comes to new products and services, partnership-based financing and investment products are the most important for participation banks and in general for the interest-free financing industry in Turkey.

One of the projects that has recently aimed at a faster development of interest-free finance in Turkey is the creation of the Interest-Free Finance Coordination Board which consists of the Ministry of Development; the Ministry of Finance and Treasury Undersecretaries; the presidents of the central bank, the Banking Regulation and Supervision Agency, the Capital Markets Board and the Participation Banks Association; and the general-director of Borsa Istanbul under the chairmanship of the Ministry of Treasury. The aim of the establishment is to develop and raise awareness of the interest-free finance system.

When we look at these developments, we can see that the public is spending a lot of effort in the development of interest-free financing, and from time to time we witness the authorities’ effort to trigger this development. In recent months, meetings between World Bank officials and representatives of institutional investors were part of this process. The World Bank cooperates with the government of Turkey in the development of alternative financing methods such as project bonds and Sukuk, asset-backed securities for the deepening of capital markets and the financing of long-term infrastructure investments. Within the scope of this cooperation, they are also seeking information on the supply, demand, legislation, infrastructure and tax dimensions and will provide recommendations to government authorities based on international experience, and will be meeting with interested parties. The interviews with institutional investors are aimed at assessing the demand for different Sukuk structures to be issued, in particular for the financing of public, municipal and private infrastructure projects by institutional investors.

The public infrastructure projects are indeed an important opportunity for capital markets. Given the current state of the sector in recent times, such as the stagnation in public offerings and the problem of trust in private issuances, capital market products based on public projects are alternatives to the perception of investors. Moreover, these projects cannot be financed only within the banking system due to their size. For example, the third airport project was funded by domestic bank credit, but immediately followed by refinancing from a foreign bank consortium. Of course, due to their size, these and similar projects may not also be funded solely by the capital markets at this time, but some portion of them may be served by the Sukuk issuances as well. Actually, the fact that the World Bank officials are examining alternative financing models gives the impression that the public is at least also looking for such alternatives.

These financial instruments are also important in terms of participation banking and interest-free finance. Participation banks are limited in the asset portfolios if they want to issue Sukuk. We can see that the Sukuk issued by the participation banks recently have started to be 51% based on management (leasing receivables) and 49% on Murabahah, a condition which is not sustainable. Because Murabahah-based Sukuk is a controversial issue, they are used in limited quantities of issuances that are rolled out in certain periods. However, Sukuk based on infrastructure projects are suited to the nature of interest-free financing due to their partnership nature, as well as enabling larger and longer-term issuances.

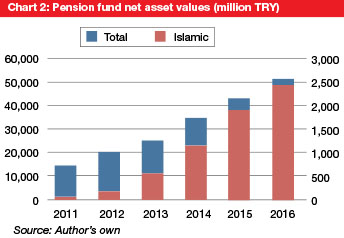

On the other hand, if we look at the issue in terms of institutional investors, there are different implications here. Turkish legislation has exclusively authorized participation banks for interest-free finance in banking. However, this is not the case on the investment side and the conventional players can manage and sell the interest-free investment funds or pension funds. Also, the fastest-growing area in the interest-free market is the area of pension investment funds. These pension investment funds need appropriate financial products that they can invest in. Therefore, there is a serious growth potential here. However, one of the most critical issues hindering progress is the establishment of interest-free finance standards in the sector to avoid problems related to Islamic compliance in the future.

Avsar Radi Sungurlu is the general manager at Bizim Portfoy Yonetimi. He can be contacted at [email protected].